AlgoLab Workflow for GBPJPY H1 (Updated 2024)

All information including workflow settings and example strategies shared on the website is intended solely for the purpose of studying topics related to the usage of StrategyQuant software and is in no way intended as a specific investment or trading recommendation.

Neither the website operator nor the individual authors are registered brokers or investment advisers or brokers.

If specific financial products, commodities, shares, forex or options are mentioned on the website, it is always and only for the informational purposes.

The website operator is not responsible for the specific decisions of individual users.

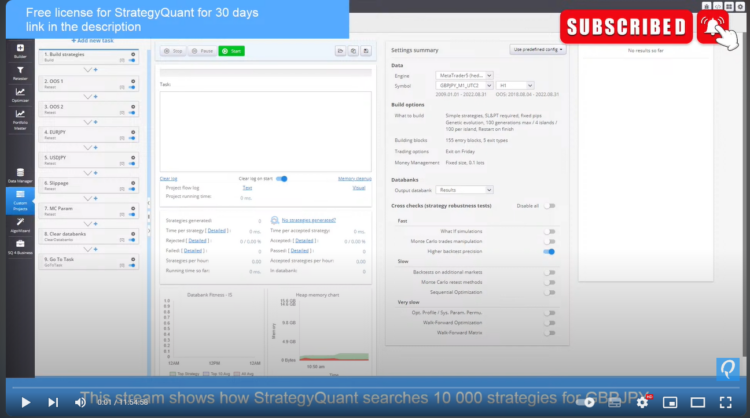

This workflow generates swing strategies for GBPJPY and uses some simple robustness testing like Monte Carlo simulations, slippage 2 Out Of Sample data test, 2 different markets: With this custom project you can start easily building strategies based on breakout and swing logic.

Live stream:

Live stream link here: https://youtube.com/live/q8dhqzFD0LU

Could you kindly clarify whether this is only applicable to GBP/JPY pairs? I would also be grateful to understand whether it could be useful for other markets as well

You can adjust it to the other markets, it could also work, but on the JPY works the best. I did not tested on other markets this workflow, you can try it and let us know in the comments.

Hi, the file is downloaded in xlm format, why can’t I download it in cfx? Thanks

The file is available in cfx format, please download the again and do not unzip the file.