AlgoLab Workflow for Swing Trading Strategies on the GBP/JPY H4 Timeframe

All information including workflow settings and example strategies shared on the website is intended solely for the purpose of studying topics related to the usage of StrategyQuant software and is in no way intended as a specific investment or trading recommendation.

Neither the website operator nor the individual authors are registered brokers or investment advisers or brokers.

If specific financial products, commodities, shares, forex or options are mentioned on the website, it is always and only for the informational purposes.

The website operator is not responsible for the specific decisions of individual users.

This workflow generates swing strategies for the GBP/JPY pair on the H4 timeframe and includes simple robustness tests, such as Monte Carlo simulations, slippage, a 2-out-of-sample data test, and two different markets. With this custom project, you can easily start building strategies based on breakout and swing logic.

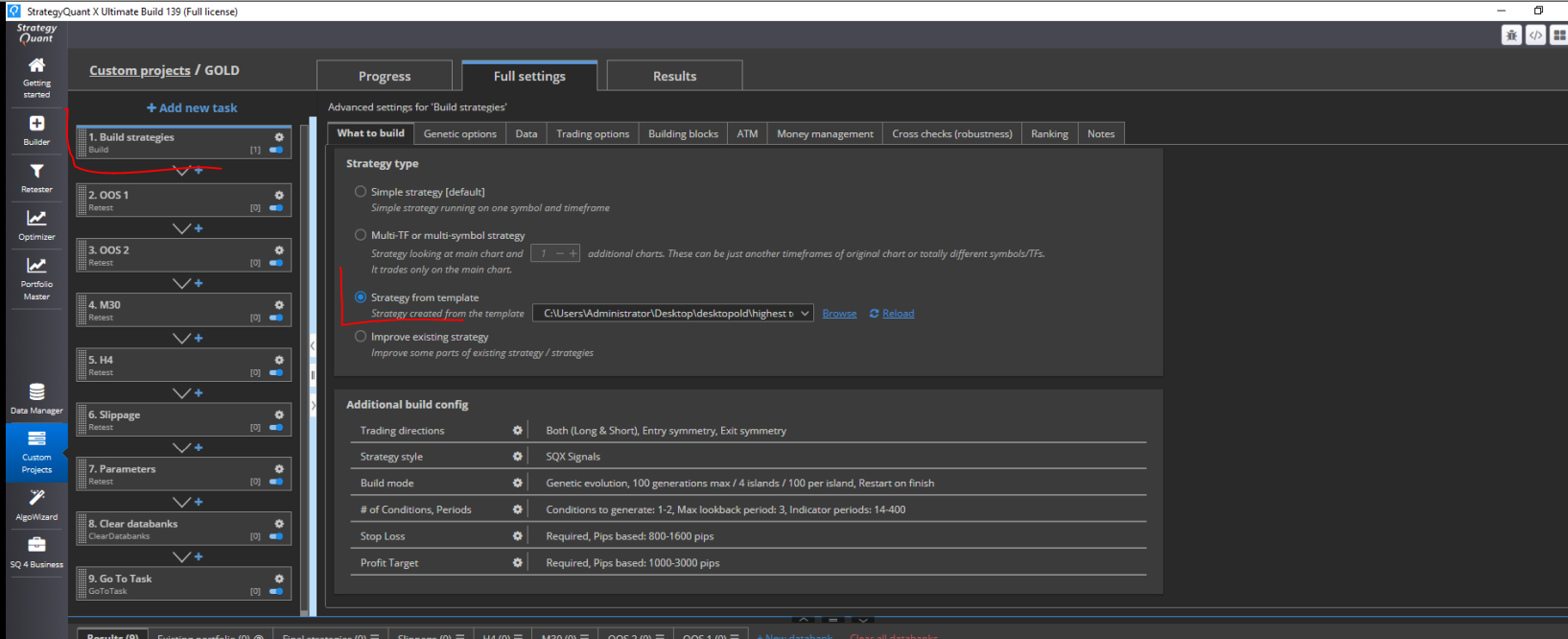

You need to also download the template and set the correct path in the builder. See attached screenshot:

Hello.I have a problem with all the shared files I download from this site. They are zip files and inside there are HTML. How can I solve it? Thank you

If you use the right click and “save file as” does that work?

Thanks for your answer. I don’t have that option, I can only “save link as”, and I can only do it in zip format and inside there is an HTML file. When I download strategies instead of a custom project, I have the same problem. How should I proceed? Do I need to set the configurations or filters in the builder?

Same problem and it doesn’t work for me either…

I tried with Save as, but HTML is the only option. I’ve tried with Chrome and Edge, and still the same.

Solved

Here (don’t open the file), right button > Save link as > select all files > add CFX extension. Ready!