We are glad to announce that a new StrategyQuant version – Build 130 is out. Also, we would like to thank you all who helped us with testing and making it bug free. This version introduces several new major features with a big potential to improve your trading results.

Few of the features with most impact:

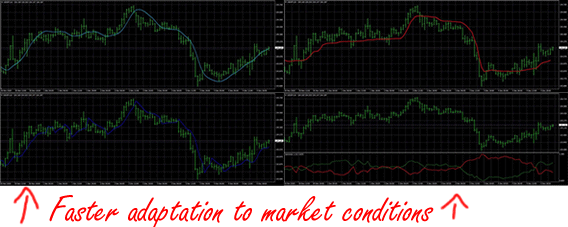

New zero-lag indicators and signals based on them

for creating more accurate trading robots. You can find detailed description of new indicators here.

Advanced Trade Management (ATM)

allowing multiple exits (scale out), and enabling multiple exits also for already existing strategies.

Documentation: Settings – ATM

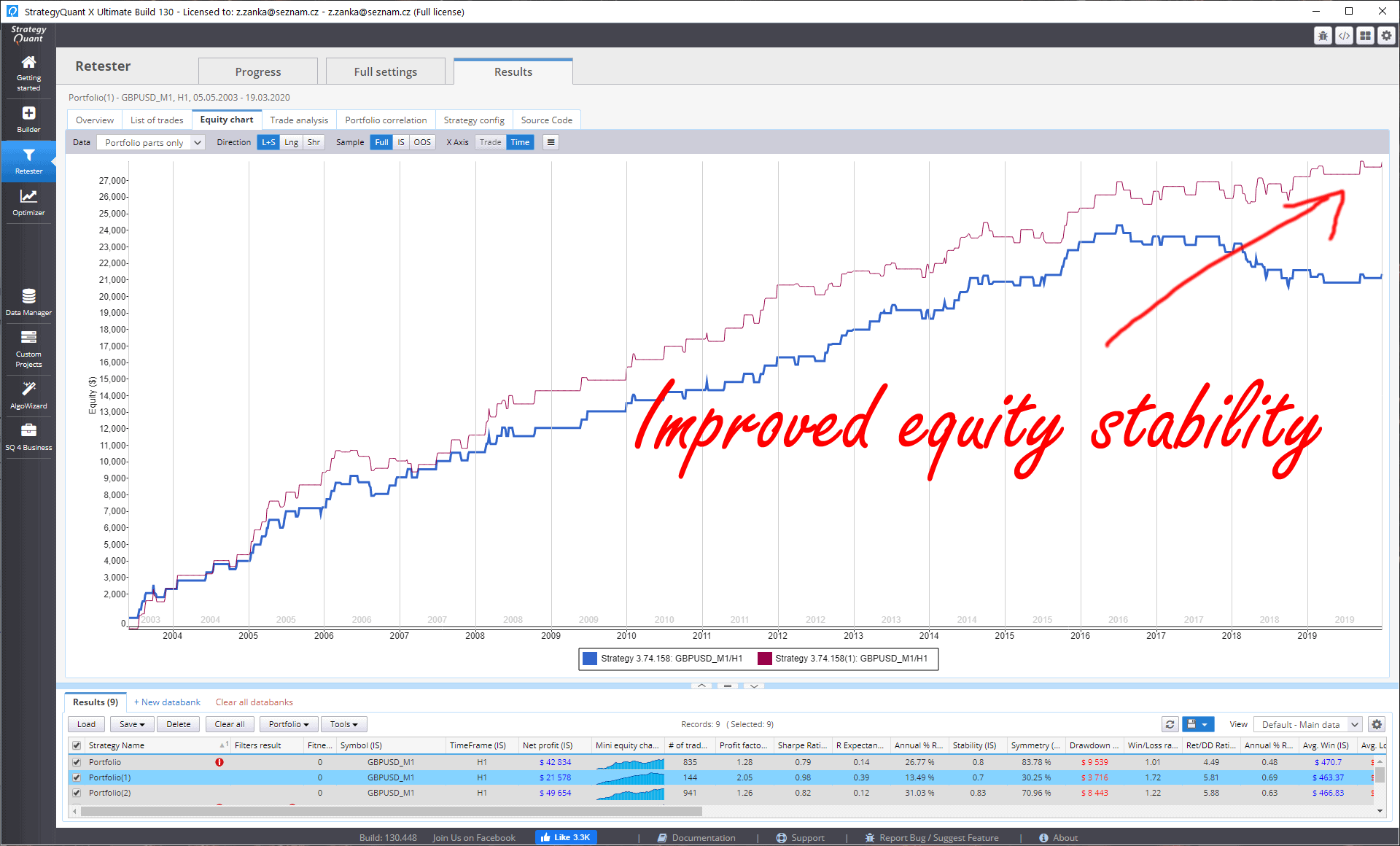

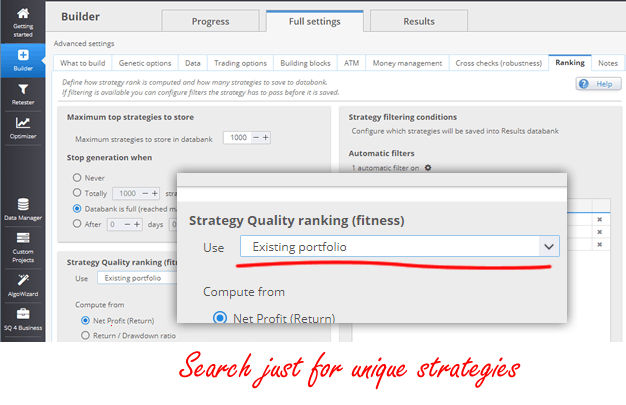

Fit to portfolio

filter in Builder – allows looking for strategies that have low correlation with your portfolio of already existing strategies.

Documentation: Fit strategy to existing portfolio

SQ for Business – MQL Market support

native support for publishing your strategies to MQL Market and earning another source of income. Only for the ULTIMATE version.

If you already have StrategyQuant Professional and you would like to use Business module then you can now upgrade your license for the better Christmas price here.

JForex engine

added support for JForex engine. Still experimental.

Other smaller features:

- Mass-modify symbols in custom project

allows you to quickly replace symbols / timeframes in all tasks of the custom project

- Compare backtest config

compare backtest configuration between two strategies and quickly find out what’s different.

Documentation: Comparing and using the same backtest settings

- PDF report from backtest

save your backtest report into PDF

- Mass-improve build type implemented in Builder

- Possibility to change type (Minimize/Maximize/Approximate) in weighted fitness configuration

- Use custom JARs in Snippets – import custom Java JAR libraries to be used in snippets.

Documentation: Using custom JAR libraries

Check our Roadmap page for a complete list.