</> Codebase

StrategyQuant X platform codebase – a place to share coded customizations and extensions – among all users.

Indicators / Signals

Relative Vigor Index – RVI

Relative Vigor Index - RVI

oscillator

Relative Vigor Index - RVI

rvi

Columns > Databank / Filter

Walk Forward Optimisation Metrics

Snippets designed for better evaluation of WFO process. Idea behind this you can find in this series: Algorithmic Backtesting & Optimization for Alphas I will add blog post

wfo

optimisation

Columns

Entry Order Types

Databank snippets described here: https://strategyquant.com/blog/how-to-categorize-your-strategies-by-entry-type-quickly-and-efficiently/ How to import custom indicators to SQX: https://strategyquant.com/doc/programming-for-sq/import-export-custom-indicators-and-other-snippets/

stop

limit

Entry Order Types

orders

type

order types

market

Columns

Databank Ratios 01032022

AnnualPercReturnAvgDDPerRatio AvgWinPerc AvgWinPercAvgDDPerRatio NetProfitAvgDDRatio PercARAvgDDRatio

ratio

databank

columns

AnnualPercReturnAvgDDPerRatio

AvgWinPerc

What If scenarios (SQ)

What If: Evaluating the trading performance of strategies

Both snippets are described in this blog post: https://strategyquant.com/blog/evaluating-the-trading-performance-of-strategies/

trading

strategies

on/off

stop tradkng

Trading options

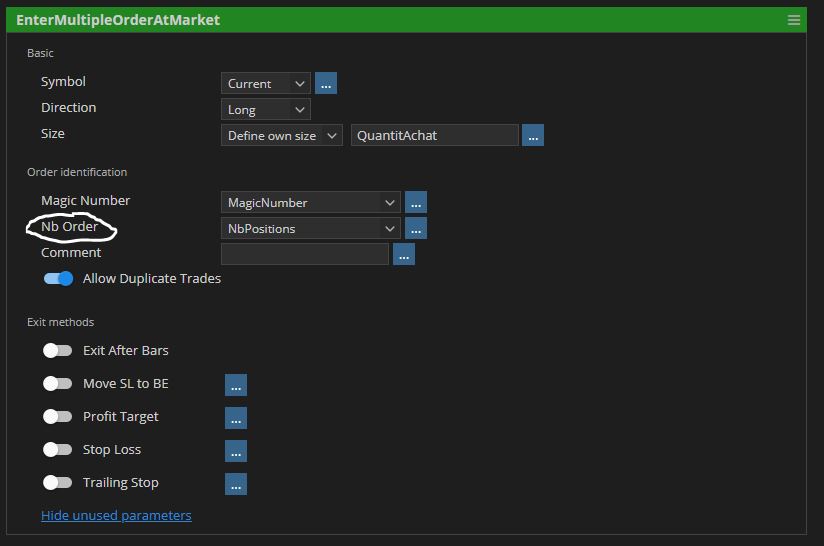

Multiple Market Order

Here is a Multiple Orders at Market snippets. It will send multiple orders at once with a different magic number.

AlgoWizard

Market Order

Multiple Market Order

Columns > Databank / Filter

Sortino Ratio

The Sortino ratio is a variation of the Sharpe ratio that differentiates harmful volatility from total overall volatility by using the asset's standard deviation of negative portfolio returns—downside deviation—instead of the total standard deviation of portfolio returns. The Sortino ratio takes an asset or portfolio's return and subtracts the risk-free rate, and then divides that amount by the asset's downside deviation. The ratio was named after Frank A. Sortino. Source: https://www.investopedia.com/ CREDIT: Acerbi

sortino ratio

risk

ratio

Indicators / Signals

Double Smoothed Stochastic Bressert

Double Smoothed Stochastics – DSS Bressert is an oscillator introduced by William Blau and Walter Bressert shortly after each other in two slightly different versions. The calculation of DSS Bressert values is similar to the stochastic indicator. The difference is the use of double exponential smoothing. The advantages over the classic stochastic oscillators are the fast response to price changes in a still very smooth pattern. In addition, the extreme zones at the other end of the scale are reached quite frequently, even in strong trends, resulting in many trend conforming signals. Double Smoothed Stochastics – DSS The Bressert values are the same as the stochastics – values above 80 indicate an overbought condition of the market, values below 20 indicate an oversold condition of the market.

oscillator

dss

inidcator

stochastic

clonex

Live coding sessions

Together with our worldwide community of traders, there is a growing group of programmers who are extending StrategyQuant with custom snippets and indicators. We would like to support your effort,