Could you introduce yourself, what is your daily job etc.

Hello, my name is EDAU87. I’m excited to have this opportunity to introduce myself and share a bit about my background and work.

I have a law degree and currently work in the Aerospace & Defense sector in the United States. While I’ve been trading since 2014, I’ve found the most success and enjoyment through algorithmic trading. Early on, I struggled with discretionary trading and made and lost a significant amount of money before discovering algo-trading.

In my free time, you can find me actively participating in discussions on quantitative finance and system building Discord servers. I really enjoy the collaborative nature of these communities as we work together to solve trading puzzles. Trading has always been a fun hobby for me, even when I hit some bumps in the road early on.

Como você começou com algo-trading?

My journey into algo-trading began in late 2020 when I programmed a watch list in a popular stock scanning software package. The list filtered microcap stocks and ranked them by the strength of their setup. Every day, I would short the top 5 ranked stocks without fail. This simple system worked very well for a long time, teaching me the value of religiously following a set of trading rules.

In 2022, I developed a basic trend-following algorithm on TradingView. This was a period of extremely strong volatility and trend moves, and the strategy performed amazingly well. However, I was not being smart about risk management, putting my entire account into each trade. Still, I followed the algorithm’s rules religiously, just as I had with the watch list.

During the September 2022 FOMC meeting, I followed the TradingView algorithm’s rules so strictly that I lost 28% of my account in about an hour. It was an emotional rollercoaster, but I managed to recoup those losses over the next few days. As soon as my account balance crossed back above its original value, I stopped trading that algorithm entirely.

Around that time, I had been watching Ali Casey’s Stat Oasis YouTube channel and decided to download SQX to learn more about algorithmic trading. While my previous systems had worked well, I never felt confident they would continue to perform in the future. Listening to Ali discuss robustness testing opened my eyes to the importance of building reliable, adaptable strategies.

With some savings from my trading profits, I invested in SQX and any courses I could find to help me master the software. I was hooked immediately. The process of developing, testing, and refining trading algorithms has been endlessly fascinating and rewarding.

Quanto tempo levou para ter sucesso, e qual foi o ponto de ruptura?

My journey to successful algo-trading began in early 2023 when I quickly put together a portfolio of daily chart swing strategies using the knowledge gained from various courses I had taken. While this initial portfolio performed reasonably well throughout the year, the infrequent trading meant the returns were modest.

However, I never stopped learning and improving my skills. I built a powerful PC dedicated to running SQX 24/7 to support my custom research projects. I immersed myself in the literature on robustness testing, data mining, and genetic algorithms to deeply understand the tools I was using.

The breakthrough came in late 2023 when I learned not to focus on individual strategies, but rather the process I used to develop them. Inspired by the work of longtime SQX user Coensio, who has a great SQX course, publishes a blog on trading system development and runs a great discord community on the subject, I realized the importance of refining my workflow and forward-testing it, just as I would with the strategies themselves. This insight unlocked my ability to create robust intraday strategies, which had previously eluded me.

Within a few weeks of adopting this new process-driven approach, I developed a dozen day trading strategies that passed rigorous robustness tests. I deployed these live, trading a single micro futures contract to learn and refine my workflow further using everything I had learned from courses, books, white papers, and videos.

As of early 2024, my algo-trading business has scaled to a portfolio of 56 strategies. I have implemented robust monitoring and risk management processes. Crucially, I can now replace my entire strategy portfolio with new ones built on recent data in just 2-3 weeks, thanks to my streamlined workflow.

In summary, it took me about a year to go from my initial success with daily chart strategies to achieving a high level of proficiency and scalability in early 2024. The key turning point was shifting my focus to refining my development process, which unlocked my ability to create robust intraday strategies and rapidly iterate on my portfolio.

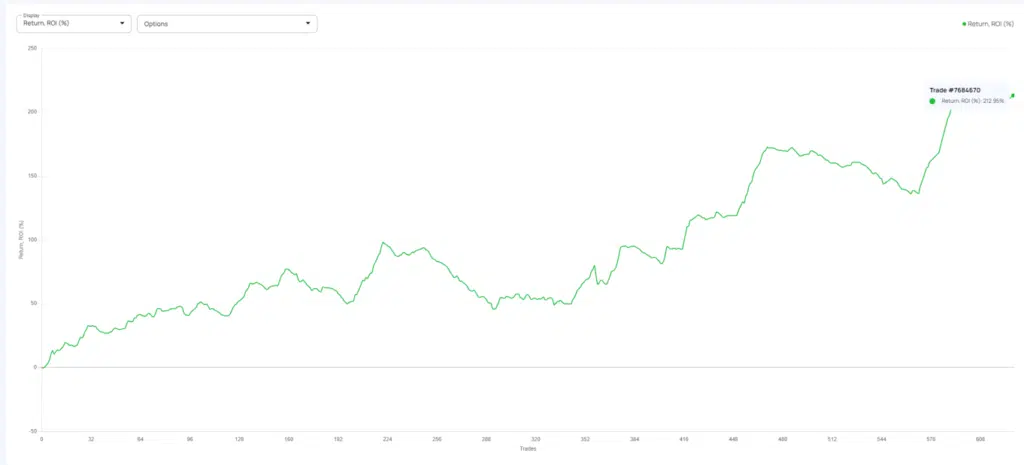

EDAU live performance since begging of 2024

O que você mais gosta em algo-trading?

The freedom is what I enjoy most about algo-trading. In my early days of discretionary trading, I was chained to my computer, constantly stressed and distracted. With “The List”, I had to be at my desk every day at 3:45 PM EST to frantically enter orders before the market close at 4 PM. It was an extremely stressful process that consumed my attention during times I couldn’t afford to be distracted.

Similarly, when I was trading my TradingView algorithm, I had no flexibility. That system required me to sit by my computer all day waiting for alerts so I could quickly enter positions when the entry bar closed. I ended up staring at charts constantly, unable to step away and enjoy life. Despite my trading performance, I was unhappy and anxious.

In contrast, today I only have to check my portfolio once a week on weekends, as my CQG data feed often resets on Friday nights. Otherwise, I never have to look at the markets if I don’t want to. By taking the time to learn MultiCharts’ steep learning curve, I’ve built a completely hands-off trading setup that takes advantage of all the auto-trading features.

Você poderia nos dizer mais sobre o fluxo de trabalho que você está utilizando para criar e selecionar as melhores estratégias?

The foundations of my workflow are protected by NDA, so I can’t provide specific step-by-step details. However, I can share that I make extensive use of various robustness testing techniques, including OOS testing, alternative market testing, WFO, and WFM analysis.

Where I’ve found the most success is in researching, testing, and refining the criteria I use for filtering and selecting robust strategies. For example, I do all my OOS testing on earlier data, so I can leverage the most recent market conditions for strategy development. On January 1, 2009, the ES futures were trading at ~$1,000 a contract with relatively light volume when compared with today. As I write this the upcoming contract is trading at $5,500 with higher volume/more noise. How do we normalize and draw meaningful conclusions from such discrepancies in price/volume? I spend a lot of time researching and testing filter configurations which achieve this goal.

Another example would be walking strategies forward. We all know 2020 was a banner year and that literally everything you threw at the market basically printed money hand over fist. How do we walk strategies forward in such a way that we don’t get false positives based entirely on a single year of outperformance in 2020? The answer? Creative use of filters.

This is where the automation features in SQX have been invaluable. I’ve been able to run tens of thousands of tests, refine my filtering criteria, and then walk the most promising filter configurations forward to validate their performance. This iterative process of research, testing, and forward validation has allowed me to develop proprietary workflows that can identify strategies that are truly robust across a variety of market conditions.

My advice to others would be to focus on mastering the process of strategy research and development rather than just trying to find “a strategy” that works. By learning how to efficiently generate, test, and validate large numbers of strategies, you can build a portfolio of robust trading systems that can perform well in diverse market environments. It’s a journey of continuous improvement, but the payoff in terms of sustainable trading performance can be substantial.

Qual é a sua filosofia de criar um portfólio ideal?

My approach to building an optimal portfolio is centered around three key principles:

1) Diversify across timeframes, strategy types, and strategy logic

2) Add strategies before adding contracts

3) Maintain low correlation between strategies

The rationale behind these principles is to create a portfolio that is resilient to various market conditions and minimizes overall risk. By diversifying across timeframes (e.g., short-term, medium-term, long-term), I ensure that my strategies are not overly dependent on any particular market environment.

Similarly, incorporating a mix of strategy types (e.g., trend-following, mean-reversion, volatility-based) and strategy logic (e.g., technical indicators, fundamental factors) further enhances the portfolio’s robustness. This approach helps to capture different market dynamics and reduces the risk of any single strategy dominating the portfolio’s performance.

Another key aspect of my philosophy is to prioritize adding new strategies over increasing the number of contracts per strategy. Research suggests that the benefits of diversification diminish exponentially after around 10-12 strategies. By rejecting this limitation, I can maintain low correlation between my strategies, typically keeping the correlation coefficient below 0.50. Remember: adding contracts to existing strategies is a guaranteed correlation of 1.0.

In summary, my philosophy emphasizes diversification across timeframes, strategy types, and logic, while prioritizing the addition of new strategies over increasing contract sizes. This approach aims to create a well-diversified, low-correlation portfolio that can navigate various market conditions and deliver consistent risk-adjusted returns.

Você está usando para estratégias parâmetros recomendados por otimização ou está usando uma maneira diferente?

I do not optimize my strategies. I use WFO/WFM as robustness tests and replace my strategies at regular intervals.

Toda carteira às vezes sofre de drawdown. Qual é a sua abordagem para superá-la e manter a confiança em seus robôs?

I proactively manage drawdowns by preparing for them before they occur. First, I size my strategy positions conservatively, ensuring I can hold every single one overnight while being down 1.5x the maximum historical portfolio drawdown. To calculate this, I use Quant Analyzer to run 100,000 Monte Carlo simulations with random resampling and no skipped trades. I then take the 100th percentile drawdown and use that as my historical max.

This is a conservative approach because it’s impossible for me to hold all my strategies overnight. By sizing for a third of the absolute maximum risk my portfolio could incur, I create a significant buffer against drawdowns.

Second, I closely monitor individual strategy performance. If a strategy hits a losing streak, I run the same Monte Carlo process I use for the portfolio overall to determine if the strategy’s drawdown has met or exceeded the historical max. If so, I turn off that strategy and replace it with a new one.

Despite these precautions, drawdowns still occur, as evidenced by my equity curve. However, I find that knowing exactly when a strategy is “broken” alleviates any stress associated with drawdowns. Experience also plays a key role in my ability to handle drawdowns. Having lost far more in the past than I’ve ever seen my portfolio draw down, I’ve developed a high tolerance for temporary setbacks.

In summary, my approach to managing drawdowns involves conservative position sizing, close monitoring of individual strategy performance, and a focus on maintaining a long-term perspective. By preparing for the worst and having the experience to weather temporary storms, I’m able to maintain confidence in my trading robots and stay the course during challenging market conditions.

What strategies do you trade? Intraday or Swing?

I trade a mixture of both.

What kind strategy logic do you trade? Breakout, mean reversion?

I trade all kinds of strategy logic: breakout, mean reversion, trend following, etc. I practice what Ali Casey preaches, however, and only build strategies that match the character of the instrument I trade on the timeframe I am trading.

What kind of correlation do you use for building portfolio?

I generally keep to below 0.40 correlation in losses only.

Do you use position sizing ?

No, everything in my portfolio is sized equally.

Existe alguma fonte de conhecimento que você gostaria de recomendar a outros comerciantes?

I have mentioned a few sources already. However, no single source of knowledge will “complete” your journey to learning algo-trading. You have to aggregate knowledge which is available and make it your own.

Você tem alguma dica sobre o que evitar ou estar ciente em algo-trading?

The most important thing to avoid in algo-trading is introducing bias into your process. My entire approach is completely systematic, from the initial building blocks and genetic settings all the way through to final strategy selection. Falling into the trap of choosing strategies based on the best-looking OOS curve or highest-performing backtest results is a surefire recipe for failure.

It’s critical to maintain objectivity and avoid confirmation bias when evaluating your strategies. Don’t selectively choose data or time periods that support your existing beliefs about what should work. Rigorously test your strategies across a wide range of conditions and be willing to discard ideas that don’t hold up. I can’t say how many times I have spent a week or more researching and testing an idea that fails. When an idea fails, the time spent researching it is gone, yet it was not wasted.

Gostaria de compartilhar algumas recomendações para outros desenvolvedores de algoritmos, em que se concentrar, etc.?

One key technique I employ is stacking edges to enhance the performance of my trading strategies. Since I only trade U.S. index futures, I leverage the fact that these markets tend to have a long-term, mean-reverting, upward bias on the daily chart, even if intraday charts can exhibit strong trending behavior.

This insight shapes my approach in SQX. For example, when building daily chart swing strategies, I incorporate long-only mean reversion logic along with favorable seasonality patterns. This allows me to stack multiple edges in my favor and improve the robustness of my strategies.

Another useful heuristic I’ve found is to pay attention to how quickly SQX starts finding viable strategies after you initiate the build process. If the software immediately generates dozens of promising candidates, it’s a good sign that you’re on the right track. Conversely, if SQX takes a long time to start finding strategies, it may indicate that you’re overfitting to the data and curve-fitting.

That said, this rule of thumb isn’t absolute. Even if SQX struggles to find strategies initially, it doesn’t mean you can’t ultimately be successful. But the odds are certainly more favorable if the software can quickly identify multiple promising candidates based on your initial parameters.

In summary, my top recommendations for other algo-developers are:

1) Look for opportunities to stack multiple edges in your favor, such as leveraging market biases and seasonality patterns

2) Pay attention to how quickly SQX generates viable strategies as a rough gauge of whether you’re on the right track

3) Remain open-minded and persistent even if the initial results aren’t promising, as the path to success isn’t always straightforward

By incorporating these principles into your workflow, you can increase your chances of developing robust, profitable trading strategies.

Tomas Vanek

Tomas Vanek