Understanding Max DD%

4 replies

kurtjensen

9 years ago #115424

Hi all,

I am new here.. currently evaluating Strategy Quant for a few days.

One thing that strikes me as odd, that I hope you can help me clear up, is how the max dd% is calculated.

The description in the manual says:

“Drawdown is the measure of the decline from a historical peak in running cumulative profit of the strategy. Max DD % is the maximum percentage drawdown of the strategy.”

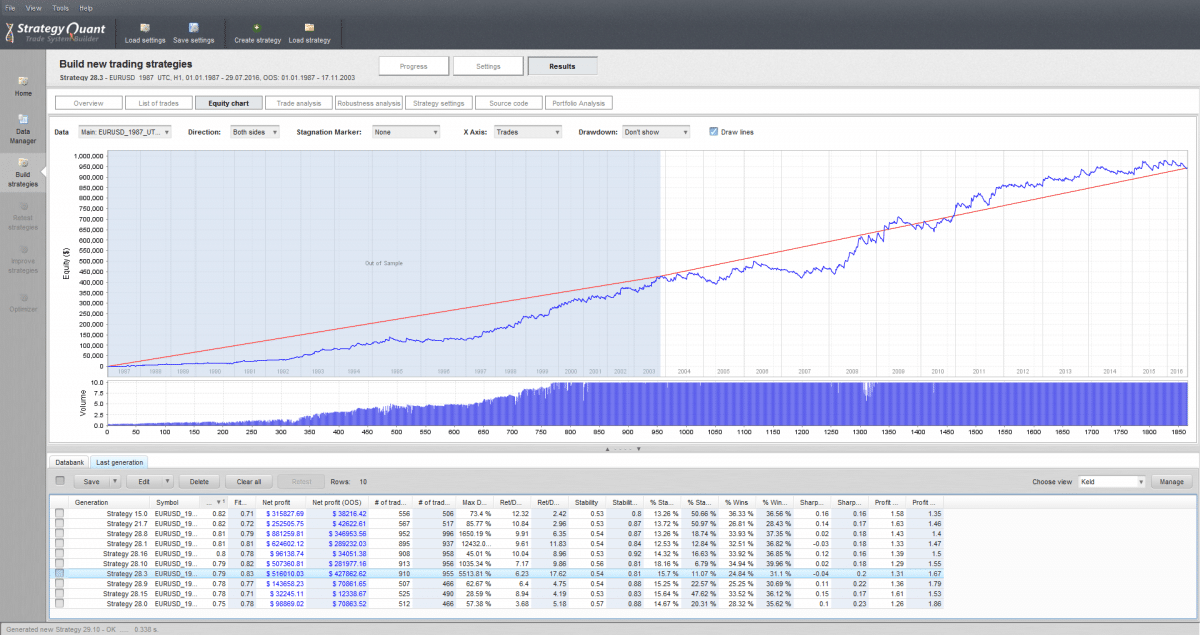

But quite often when building strategies I see large max dd% numbers being registered, without showing up on the equity curve.

For example this one on the attached screenshot says 5513% – but wouldn’t even a 100% drawdown mean you loose your entire accounts value. So why is it not showing up in the equity curve? Apparently the equity curves of a strategy with 40% max dd does not look much different from one with 5500%??

max-dd-5513-percent.png

max-dd-5513-percent.png0

mikeyc

9 years ago #138706

But quite often when building strategies I see large max dd% numbers being registered, without showing up on the equity curve.

You’ve got “show drawdown” turned off on the chart.

For example this one on the attached screenshot says 5513% – but wouldn’t even a 100% drawdown mean you loose your entire accounts value.

SQ does not stop the strategy when it has lost all the money, unlike the Metatrader 4 backtester. So you can have 500% drawdown meaning it would have lost you 5x your capital, if you had traded is over the test period. MT4 would have stopped at 100%.

Basically, your strategies are rubbish so far. 🙂

0

kurtjensen

9 years ago #138717

Ok, hmm I still don’t get it, when I turn on show drawdown in percent, it still shows a different drawdown.

Please see this screenshot:

https://www.dropbox.com/s/1j0275jyorf1h3j/Screenshot%202016-08-06%2008.55.49.png?dl=0

{kind=link}

OOS drawdown on equity graph shows 30% but the top strategy on the list which I am viewing shows 1018% drawdown OOS.

SQ does not stop the strategy when it has lost all the money, unlike the Metatrader 4 backtester. So you can have 500% drawdown meaning it would have lost you 5x your capital, if you had traded is over the test period. MT4 would have stopped at 100%.

I understand this, but why does the equity curve not show the 500% drawdown – logically the equity curve should show that it goes in minus. Can we even trust the equity curve then? Or is it the Max DD% that is somehow wrong? It has to be one or the other imho.

0

pknoell

9 years ago #138732

I guess it’s the DD% from the robustness test. That’s always higher than the normal historical one.

0

tomas262

9 years ago #138792

Hello, you can upload you strategy I can have a look at the trade list and compare DD values

0

Viewing 4 replies - 1 through 4 (of 4 total)