This article will be about a StrategyQuant success story. The title is a little exaggeration, of course there is no such thing as perfect portfolio, but in this article I’ll present one that is close 🙂

I was contacted recently by two traders who have very good results building and live trading portfolio of strategies generated by StrategyQuant.

Their results can be used as an inspiration and showcase how it is possible to generate very nice looking portfolio of strategies in StrategyQuant.

Nice not only in sense of great equity chart on historical data, but with continued consistent results also in live trading on real (not demo) accounts.

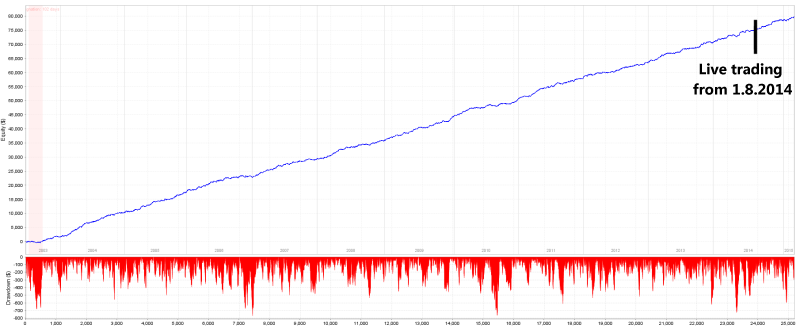

Portfolio equity

Note that they continue to improve and manage the portfolio. It started with less than 20 strategies, currently it trades around 30 strategies.

Their portfolio consists of around 30 strategies right now, trading on multiple symbols on multiple timeframes ranging from 15 minutes to 4 hours.

The last part of the equity is after starting on live account, results in SQ match the results on their live account very closely.

Note very small drawdowns and consistent growth almost all the time.

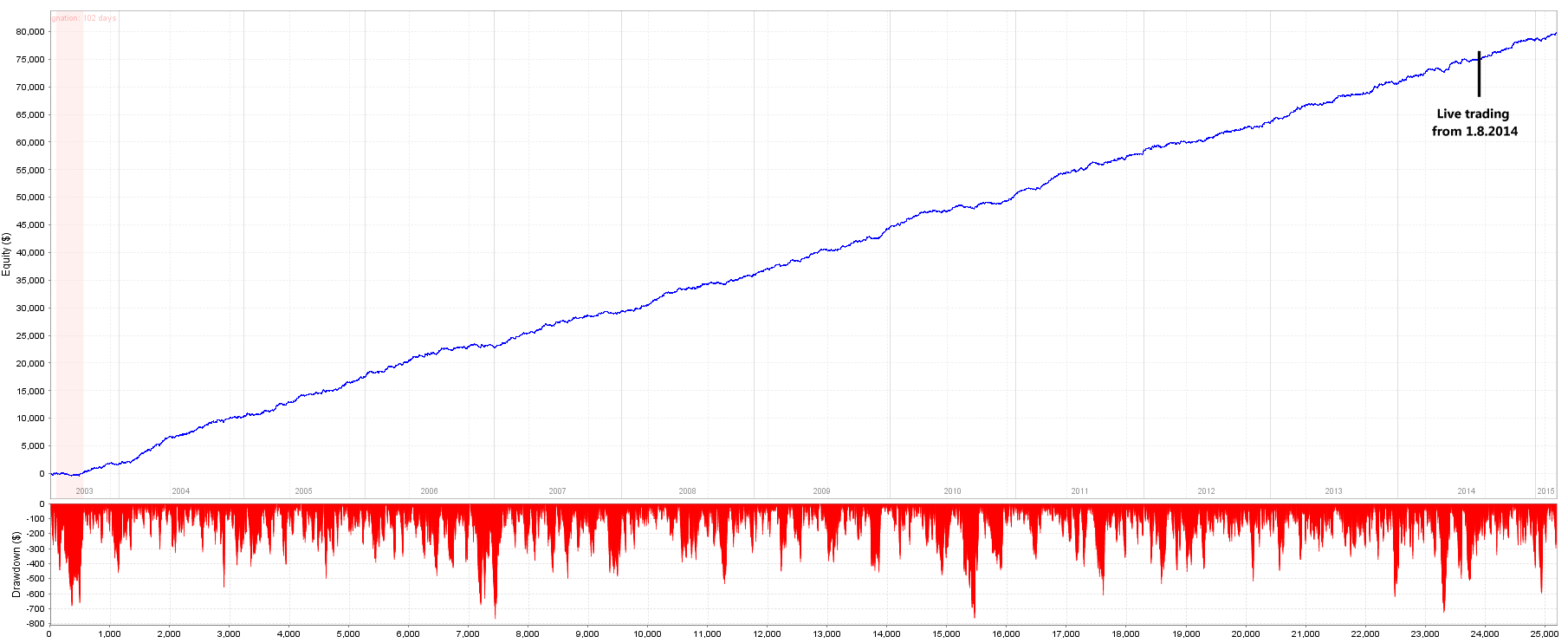

Myfxbook – trading on live account (since February 2015)

The portfolio is traded live since August 2014, I started trading it (for tracking purposes) on a live account in February 2015.

This also shows the power of portfolio – I believe that it is possible to achieve this kind of stability only by a bigger portfolio of strategies.

No single strategy (if it is not curve fitted) would be able to have such consistent returns.

So one thing to learn is that in order to achieve stability in earnings we have to think in terms of portfolios, not searching for one perfect strategy.

The portfolio itself should consist of different, non-correlated strategies that trade at different times, possibly on different instruments / timeframes, with different entry and exit conditions.

Note

as far as I now those traders are not active on our forum. They also clearly expressed that they have NO INTEREST in:

- selling/exchanging their strategies

- teaching or discussing their specific process

- managing external money

They allowed me to publish their results as a showcase and were willing to answer a few questions.

Q & A

Q: Hello, can you tell us a little bit about you?

What is your background, are you traders or programmers?

No, we are not programmers. We are traders who got to automatic trading thanks to StrategyQuant.

Q: When did you get to trading and have you tried some other trading styles? (Intraday, manual trading, etc.)

I started with trading about 3 years ago. My colleague is in trading for even longer.

We tried various different approaches. Binary options, intraday trading and we tested various strategies that can be found on the net. We ended up trading higher timeframes (4H+).

Q: Can you tell us how much time and effort did it take you to get to the point where you are now?

It took longer than a year. We both work with SQ every day. There is simply a big amount of time involved in this.

It is not only the work with the program, but also thinking about the new ideas and the correct approach.

This work is a lot about time. You can think at one point that you are on a good path, but you’ll see the result verified only after a couple of months…

Q: You use only standard technical indicators like moving averages, CCI, RSI, etc. that are available in any platform.

I mean that you don’t use any special custom indicators that would be your “secret”, right?

We never felt any need to use them. We don’t have and we don’t know any magic custom indicator that we would need to have in StrategyQuant and we use standard MT4 as a trading platform.

But it’s up to every trader who works with SQ.

Q: You developed a your own specific know-how, or a way how to work with the strategies. Without disclosing your know-how, could you tell us something about your strategy development process? What are the steps from first strategy generation until you decide that it should be a part of your live portfolio?

It is very difficult to answer this question without revealing something we don’t want.

In any way, it is not a complicated process that would involve some advanced math.

The hard task was to find and refine our process of finding and evaluating the strategies.

Q: How do you consider single strategies and the portfolio as a whole? What portfolio parameters are you trying to improve? What are the most important things that you consider when evaluating a strategy?

In general the new strategy has to satisfy some basic requirements. These requirements are probably as same as most other traders have… robustness tests, etc.

Once we have this strategy we further consider it as a part of the portfolio.

Our goal is to have stable equity with minimal drawdowns.

Q: I like that you are very conservative and don’t chase the biggest possible profits.

Many people with your results would already try to use high % risk per trade, with a vision of how much money they’ll make and what they’ll buy.

Do you consider psychology, staying with both feet on the ground and constant reminding that anything could go wrong (for example the case with Swiss franc recently) an important part of trading?

Trading for us is something we expect to make money and pay the bills in the long term. So we strive to approach it very responsibly.

Psychology is certainly very important. They say that one of the advantages of algo trading is that it is not as emotionally demanding as discretionary trading, but that is not correct.

It is just that one set of negative emotions is replaced with another set.

Especially in the beginning, when you are not sure that what you are doing is right. You have doubts about strategies, whether they’ll really work… Everything takes long etc.

Most probably everybody who got to algo trading has similar experience. It is a long process of continuous build of trust in yourself.

And that case with Swiss franc … we perceived very intensively. Not how it happened, but what happened after. Bankruptcies of brokers, attempts from brokers to recover negative balances from traders and so on.

It was difficult for us to cope with it. The feeling that you can do everything right, but then something like this happens and you’ll lose the money on the account and even more….

There is no 100% protection against things like this (well, we can stop trading completely 🙂

So we are thinking how to minimize the losses from events like these.

Q: Could you give some advice to people who are struggling creating their own strategies? What are the mistakes you made or you see people around making? What could help them succeed?

The question is whether we want to help to create our competition at all 🙂

It is difficult to give exact advice, because there is no general way applicable for everybody. Some people see SQ as a factory that will produce only working strategies if they’ll adhere to the right process.

You have to realize that SQ is an incredible tool, but it is you who decide about your success.

The fact that you’ll create a strategy in SQ that passes all the tests that you prepared is only the beginning, and you are far from finish.

It is also difficult to get through some information noise. There is a lot of information how to do this or that in books and on the net, and it is a problem to find something that will really help you.

Thank you and I wish you a good luck 🙂

Summary

What I personally learned from this example is the power of having bigger portfolio. I really haven’t imagined that a correctly built portfolio can smooth the equity curve and minimize drawdowns that much.

Second message – it takes time and effort. StrategyQuant is a tool that saves you thousands of hours of creating the strategies. SQ is 1000x faster than manual trader in creating and testing trading ideas and generating promising trading strategies. But generating the strategy and testing it for robustness is not the end of the process, it is the beginning, and the process requires some substantial time and work (not counting SQ running time).

The third message is that it is possible to get to profitable algo trading using StrategyQuant. It may be not simple, and it would require a lot of effort and time, but this is why 90% people fail in trading.

There are others who did it, and their only difference from the unsuccessful ones is mostly internal factors – dedication, correct thinking, common sense, finding what works, not following the hype; it is not having fastest computer, or using exotic custom indicators.

I hope this article was useful for you. You can discuss it below.

Emmanuel Evrard

Emmanuel Evrard

How can it be that the real account verified in myfxbook has so different results?

Is there an update on that? Would really like to read about actual success stories…