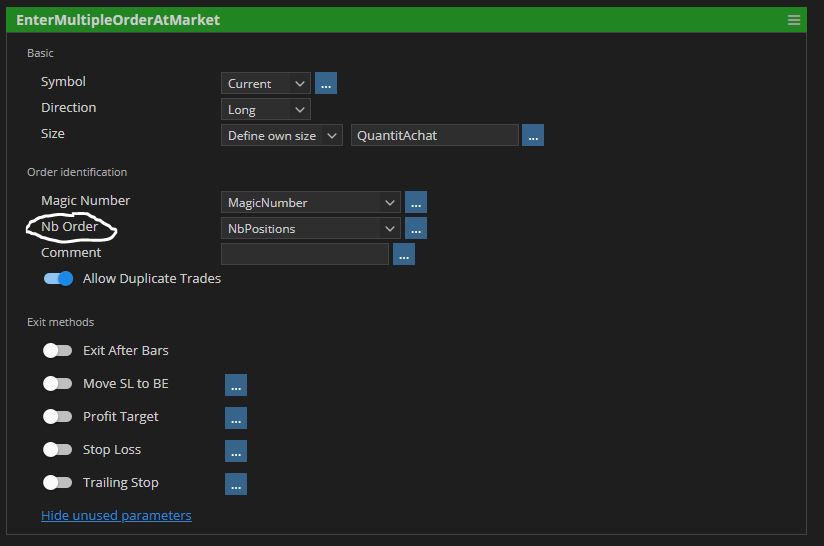

Orden de mercado múltiple

A continuación se muestra un fragmento de órdenes múltiples en el mercado .

Enviará varios pedidos a la vez con un número mágico diferente.

En la captura , puede seleccionar el nb (número) de orden y un número mágico.

Por ejemplo, si selecciona 3 como número de órdenes y 1000 como número mágico, se crearán 3 órdenes de mercado con el siguiente número mágico: 1000, 1001 y 1002...

(puede crear tantos pedidos como necesite)

A continuación, puede cerrar parcialmente algunas de las órdenes de mercado en un objetivo de beneficios y luego cerrar otras órdenes en diferentes objetivos de beneficios o stop loss.

package SQ.Blocks.Order.Open;

import java.util.ArrayList;

import com.strategyquant.datalib.TradingException;

import com.strategyquant.datalib.UpdateEventTypes;

import com.strategyquant.lib.SQTime;

import com.strategyquant.lib.SQUtils;

import com.strategyquant.lib.SettingsMap;

import com.strategyquant.tradinglib.ATM;

import com.strategyquant.tradinglib.ATMExit;

import com.strategyquant.tradinglib.BlockDefinitionException;

import com.strategyquant.tradinglib.BuildingBlock;

import com.strategyquant.tradinglib.CategoryOrder;

import com.strategyquant.tradinglib.Editor;

import com.strategyquant.tradinglib.Editors;

import com.strategyquant.tradinglib.ExitMethod;

import com.strategyquant.tradinglib.ExitTypes;

import com.strategyquant.tradinglib.Help;

import com.strategyquant.tradinglib.IActionEventListener;

import com.strategyquant.tradinglib.IFormula;

import com.strategyquant.tradinglib.ILiveOrder;

import com.strategyquant.tradinglib.Order;

import com.strategyquant.tradinglib.OrderCloseTypes;

import com.strategyquant.tradinglib.OrderTypes;

import com.strategyquant.tradinglib.Parameter;

import com.strategyquant.tradinglib.Required;

import com.strategyquant.tradinglib.ReturnTypes;

import com.strategyquant.tradinglib.SortOrder;

import com.strategyquant.tradinglib.StrategyBase;

import com.strategyquant.tradinglib.atm.exits.None;

import com.strategyquant.tradinglib.atm.exits.TrailingStop;

import com.strategyquant.tradinglib.simulator.Engines;

import SQ.ExitMethods.StopLoss;

import SQ.Functions.OrderFunctions;

import SQ.Internal.ActionBlock;

import SQ.Internal.MMFormulaBlock;

// Modified in France by Emmanuel Evrard for the StrategyQuantX Community :)

@BuildingBlock(name="(MMKT) Enter Multiple Order at market", display="EnterMultipleOrderAtMarket", returnType=ReturnTypes.Order)

@Help("Opens Multiple order at current market price")

@SortOrder(400)

@CategoryOrder(100)

public class EnterAtMarketMultiOrder extends ActionBlock

{

private static final int MaxDistanceFromMarketHash = "MaxDistanceFromMarket.MaxDistanceFromMarket".hashCode();

private static final int MaxDistanceFromMarketPctHash = "MaxDistanceFromMarket.MaxDistancePct".hashCode();

// Basic parameters

@Parameter(defaultValue="Any", category="Basic", showIfDefault=false)

@Editor(type=Editors.SelectionSymbolsWithAny)

public String Symbol;

@Parameter(defaultValue="1", category="Basic")

@Editor(type=Editors.Selection, values="Long=1,Short=-1")

public int Direction;

@Parameter(category="Basic")

@Editor(type=Editors.Formula, formulaName="Size")

@Required

public IFormula Size;

// Other parameters

@Parameter(defaultValue="MagicNumber", category="Order identification", showIfDefault=false)

@Help("Magic number is used to identify the first trade, it should be unique for every trade you open.")

@Editor(type=Editors.SelectionVariables)

public int MagicNumber;

@Parameter(defaultValue="Number Of Order", category="Order identification", showIfDefault=false)

@Help("Number Of Order is used to set the quantity of order, Their MagicNumbers are successives to the above MagicNumber")

@Editor(type=Editors.SelectionVariables)

public int NbOrder;

@Parameter(defaultValue="", category="Order identification", showIfDefault=false)

public String Comment;

@Parameter(defaultValue="false", category="Order identification", showIfDefault=false)

@Help("If set to true, it will allow to place multiple trades with the same Magic Number")

public boolean AllowDuplicateTrades;

public ExitMethod[] ExitMethods;

//------------------------------------------------------------------------

//------------------------------------------------------------------------

//------------------------------------------------------------------------

@Override

public void OnAction() throws TradingException

{

if((!AllowDuplicateTrades || !engineSupportsDuplicateTrades()) && checkLiveOrderExists(0, true) != null)

{

// market is not flat and duplicate trades are not allowed

return;

}

// open trade

byte orderType = (Direction > 0 ? OrderTypes.Buy : OrderTypes.Sell);

double sl = computeSL(orderType, (Direction > 0 ? Strategy.MarketData.Chart(Symbol).Ask() : Strategy.MarketData.Chart(Symbol).Bid()));

double size = computeSize(orderType, 0, sl);

ATM atm = Strategy.getATM();

if(atm != null && atm.isApplicable(Strategy, size, sl, orderType))

{

double pt = computePT(orderType, (Direction > 0 ? Strategy.MarketData.Chart(Symbol).Ask() : Strategy.MarketData.Chart(Symbol).Bid()));

int MagicNumber1 = MagicNumber;

for(int i = 0; i < NbOrder; i++)

{

MagicNumber = MagicNumber1 + i ;

openATMOrder(atm, -1, size, sl, pt, orderType, 0);

}

}

else

{

int MagicNumber1 = MagicNumber;

for(int i = 0; i < NbOrder; i++)

{

MagicNumber = MagicNumber1 + i ;

openNormalOrder(-1, size, sl, orderType, 0);

}

}

}

//------------------------------------------------------------------------

protected void openATMOrder(ATM atm, double openPrice, double fullSize, double sl, double pt, byte orderType, int barsValid) throws TradingException

{

ExitMethod slExit = getStopLossExit();

double sizeSoFar = 0;

if(Strategy.getEngine() == Engines.MetaTrader4 || Strategy.getEngine() == Engines.MetaTrader5Hedged) {

for(int i=0; i<atm.getExitsCount(); i++) {

ATMExit atmExit = tryCloneATMExit(atm.getExit(i));

boolean isLastExit = (i == atm.getExitsCount()-1);

double size = atmExit.computeSize(fullSize, sizeSoFar, isLastExit);

if(size > 0) {

ILiveOrder order = Strategy.Trader.Open(orderType, Symbol, openPrice)

.setSize(size)

.setMagicNumber(MagicNumber)

.setComment(Comment)

.Send();

sizeSoFar += order.getSize();

if(order.isSuccessful()) {

handleBarsValid(order, barsValid);

// add standard SL

if(slExit != null && !order.isClosedOrder()) {

slExit.setForOrder(order, Strategy);

}

// add ATM exit

atmExit.setForOrder(order, Strategy, sl, pt);

}

}

}

}

else {

ILiveOrder order = Strategy.Trader.Open(orderType, Symbol, openPrice)

.setSize(fullSize)

.setMagicNumber(MagicNumber)

.setComment(Comment)

.Send();

if(order.isSuccessful()) {

handleBarsValid(order, barsValid);

// add standard SL

if(slExit != null && !order.isClosedOrder()) {

slExit.setForOrder(order, Strategy);

}

for(byte i=0; i<atm.getExitsCount(); i++) {

ATMExit atmExit = tryCloneATMExit(atm.getExit(i));

boolean isLastExit = (i == atm.getExitsCount() - 1);

double size = atmExit.computeSize(fullSize, sizeSoFar, isLastExit);

if(size > 0) {

sizeSoFar += Strategy.getEngine() == Engines.MetaTrader5Netted ? openNewATMNettingOrder(order, atmExit, size, sl, pt, i) : openNewTSATMOrder(order, atmExit, size, sl, pt, i);

}

}

}

}

}

//------------------------------------------------------------------------

private double openNewTSATMOrder(ILiveOrder mainOrder, ATMExit atmExit, double size, double sl, double pt, byte exitIndex) throws TradingException {

mainOrder.registerEvent(UpdateEventTypes.BarOpen, new IActionEventListener() {

private ILiveOrder exitOrder = null;

private double actualSL = -1, actualPT = -1;

private double lastTS = -1;

private boolean filled = false;

@Override

public void OnActionEvent(StrategyBase strategy) throws TradingException {

if(mainOrder.isClosedOrder()) {

if(exitOrder != null) {

exitOrder.Close(OrderCloseTypes.Deleted);

exitOrder = null;

}

return;

}

if(!mainOrder.isMarketOrder()) return;

//SL and PT must be calculated when order is filled. Otherwise it may use old indicator values (TradeStation fills on next bar)

actualSL = computeSL(mainOrder.getOrderType(), mainOrder.getOpenPrice());

actualPT = computePT(mainOrder.getOrderType(), mainOrder.getOpenPrice());

if(atmExit.exitLevel instanceof None) {

None noneExit = (None) atmExit.exitLevel;

if(noneExit.checkExitAfterBars(mainOrder)) {

noneExit.deactivate();

Strategy.Trader.Open(mainOrder.isLong() ? OrderTypes.Sell : OrderTypes.Buy, mainOrder.getSymbol(), 0)

.setSize(size)

.setMagicNumber(MagicNumber)

.setComment(Comment)

.setExitIndex(exitIndex)

.Send();

}

}

else if(atmExit.exitLevel instanceof TrailingStop) {

if(filled) return;

double newTrailingPrice = SQUtils.fixPrice(Strategy.getInstrumentInfo().tickStep, atmExit.exitLevel.getNettingPrice(Strategy, mainOrder, actualSL, actualPT));

if(mainOrder.isLong()) {

if(newTrailingPrice > mainOrder.getOpenPrice() && newTrailingPrice > actualSL && newTrailingPrice > lastTS) {

//move trailing exit closer to current price

lastTS = newTrailingPrice;

}

}

else {

if(newTrailingPrice < mainOrder.getOpenPrice() && newTrailingPrice < actualSL && (newTrailingPrice < lastTS || lastTS < 0)) {

//move trailing exit closer to current price

lastTS = newTrailingPrice;

}

}

if(exitOrder != null) {

if(exitWasFilled(exitOrder)) { //Trailing stop has been hit

filled = true;

return;

}

else {

exitOrder.Close(OrderCloseTypes.Replaced);

}

}

if(lastTS > 0) {

exitOrder = Strategy.Trader.Open(Direction > 0 ? OrderTypes.SellStop : OrderTypes.BuyStop, Symbol, lastTS)

.setSize(size)

.setMagicNumber(MagicNumber)

.setComment(Comment)

.setExitIndex(exitIndex)

.Send();

exitOrder.registerEvent(UpdateEventTypes.OrderFilled, new IActionEventListener() {

@Override

public void OnActionEvent(StrategyBase Strategy) throws TradingException {

if(exitWasFilled(exitOrder)) {

filled = true;

}

}

});

}

}

else {

if(filled) return;

double exitOpenPrice = SQUtils.fixPrice(Strategy.getInstrumentInfo().tickStep, atmExit.exitLevel.getNettingPrice(Strategy, mainOrder, actualSL, actualPT));

if(exitOpenPrice <= 0) {

return;

}

if(exitOrder != null) {

if(exitWasFilled(exitOrder)) return;

else {

exitOrder.Close(OrderCloseTypes.Deleted);

exitOrder = null;

}

}

exitOrder = Strategy.Trader.Open(Direction > 0 ? OrderTypes.SellLimit : OrderTypes.BuyLimit, Symbol, exitOpenPrice)

.setSize(size)

.setMagicNumber(MagicNumber)

.setComment(Comment)

.setExitIndex(exitIndex)

.Send();

if(exitOrder.isSuccessful()) {

exitOrder.registerEvent(UpdateEventTypes.BarOpen, new IActionEventListener() {

@Override

public void OnActionEvent(StrategyBase strategy) throws TradingException {

boolean mainOrderExists = false;

for(int i=Strategy.Trader.getOpenOrdersCount(false) - 1; i >= 0; i--) {

ILiveOrder order = Strategy.Trader.getOpenOrder(i, false);

if(order.getOrderId() == mainOrder.getOrderId()) {

mainOrderExists = true;

}

}

if(!mainOrderExists) {

exitOrder.Close(OrderCloseTypes.Deleted);

}

}

});

exitOrder.registerEvent(UpdateEventTypes.OrderFilled, new IActionEventListener() {

@Override

public void OnActionEvent(StrategyBase Strategy) throws TradingException {

if(exitWasFilled(exitOrder)) {

filled = true;

}

}

});

}

}

}

});

return size;

}

//------------------------------------------------------------------------

private double openNewATMNettingOrder(ILiveOrder mainOrder, ATMExit atmExit, double size, double sl, double pt, byte exitIndex) throws TradingException {

// for None attach a BarOpen event listener and close after number of bars set

if(atmExit.exitLevel instanceof None) {

mainOrder.registerEvent(UpdateEventTypes.BarOpen, new IActionEventListener() {

@Override

public void OnActionEvent(StrategyBase strategy) throws TradingException {

if(mainOrder.isClosedOrder() || !mainOrder.isMarketOrder()) return;

None noneExit = (None) atmExit.exitLevel;

if(noneExit.checkExitAfterBars(mainOrder)) {

noneExit.deactivate();

ILiveOrder exitOrder = Strategy.Trader.Open(mainOrder.isLong() ? OrderTypes.Sell : OrderTypes.Buy, mainOrder.getSymbol(), 0)

.setSize(size)

.setMagicNumber(MagicNumber)

.setComment(Comment)

.setExitIndex(exitIndex)

.Send();

}

}

});

return size;

}

else if(atmExit.exitLevel instanceof TrailingStop) {

mainOrder.registerEvent(UpdateEventTypes.BarOpen, new IActionEventListener() {

private ILiveOrder exitOrder = null;

private double lastTS = -1;

private boolean filled = false;

@Override

public void OnActionEvent(StrategyBase strategy) throws TradingException {

if(filled) return;

if(mainOrder.isClosedOrder()) {

if(exitOrder != null) {

exitOrder.Close(OrderCloseTypes.Deleted);

exitOrder = null;

}

return;

}

if(mainOrder.isMarketOrder()) {

double newTrailingPrice = SQUtils.fixPrice(Strategy.getInstrumentInfo().tickStep, atmExit.exitLevel.getNettingPrice(Strategy, mainOrder, mainOrder.getSL(), mainOrder.getPT()));

double prevTS = lastTS;

if(mainOrder.isLong()) {

if(newTrailingPrice > mainOrder.getOpenPrice() && newTrailingPrice > mainOrder.getSL() && newTrailingPrice > lastTS) {

//move trailing exit closer to current price

lastTS = newTrailingPrice;

}

}

else {

if(newTrailingPrice < mainOrder.getOpenPrice() && newTrailingPrice < mainOrder.getSL() && (newTrailingPrice < lastTS || lastTS < 0)) {

//move trailing exit closer to current price

lastTS = newTrailingPrice;

}

}

if(prevTS != lastTS && lastTS > 0) {

if(exitOrder != null) {

exitOrder.Close(OrderCloseTypes.Replaced);

}

exitOrder = Strategy.Trader.Open(Direction > 0 ? OrderTypes.SellStop : OrderTypes.BuyStop, Symbol, lastTS)

.setSize(size)

.setMagicNumber(MagicNumber)

.setComment(Comment)

.setExitIndex(exitIndex)

.Send();

exitOrder.registerEvent(UpdateEventTypes.OrderFilled, new IActionEventListener() {

@Override

public void OnActionEvent(StrategyBase Strategy) throws TradingException {

if(exitWasFilled(exitOrder)) {

filled = true;

}

}

});

}

}

}

});

return size;

}

// for other types create limit orders

double exitOpenPrice = SQUtils.fixPrice(Strategy.getInstrumentInfo().tickStep, atmExit.exitLevel.getNettingPrice(Strategy, mainOrder, sl, pt));

if(exitOpenPrice <= 0) {

return 0;

}

ILiveOrder exitOrder = Strategy.Trader.Open(Direction > 0 ? OrderTypes.SellLimit : OrderTypes.BuyLimit, Symbol, exitOpenPrice)

.setSize(size)

.setMagicNumber(MagicNumber)

.setComment(Comment)

.setExitIndex(exitIndex)

.Send();

if(exitOrder.isSuccessful()) {

exitOrder.registerEvent(UpdateEventTypes.BarOpen, new IActionEventListener() {

@Override

public void OnActionEvent(StrategyBase strategy) throws TradingException {

boolean mainOrderExists = false;

for(int i=Strategy.Trader.getOpenOrdersCount(false) - 1; i >= 0; i--) {

ILiveOrder order = Strategy.Trader.getOpenOrder(i, false);

if(order.getOrderId() == mainOrder.getOrderId()) {

mainOrderExists = true;

}

}

if(!mainOrderExists) {

exitOrder.Close(OrderCloseTypes.Deleted);

}

}

});

return size;

}

else return 0;

}

//------------------------------------------------------------------------

private boolean exitWasFilled(ILiveOrder exitOrder) {

return exitOrder.isMarketOrder() && exitOrder.getCloseTime() > 0;

}

//------------------------------------------------------------------------

protected void openNormalOrder(double openPrice, double size, double sl, byte orderType, int barsValid) throws TradingException {

ILiveOrder order = Strategy.Trader.Open(orderType, Symbol, openPrice)

.setSize(size)

.setMagicNumber(MagicNumber)

.setComment(Comment)

.Send();

if(order.isSuccessful()) {

handleBarsValid(order, barsValid);

for(ExitMethod exitMethod : ExitMethods) {

if(!order.isClosedOrder()) {

if(AllowDuplicateTrades) {

//we have to clone the exit method, otherwise it makes problems when strategy has duplicate trades enabled (problem example: Trailing Stop is set only for the first order)

try {

ExitMethod exitMethodCloned = (ExitMethod) exitMethod.clone(true, Strategy);

exitMethodCloned.setForOrder(order, Strategy);

}

catch (BlockDefinitionException e) {

Log.error("Cannot clone exit method '" + exitMethod.getClass().getName() + "' for order #" + order.getOrderId(), e);

}

}

else {

exitMethod.setForOrder(order, Strategy);

}

}

}

}

}

//------------------------------------------------------------------------

protected void handleBarsValid(ILiveOrder order, int barsValid) throws TradingException {

if(order.isClosedOrder() || order.isMarketOrder()) return;

// order is placed, now handle order validity

if(barsValid != 0) {

order.registerEvent(UpdateEventTypes.BarOpen, new IActionEventListener() {

@Override

public void OnActionEvent(StrategyBase strategy) throws TradingException {

checkBarsValid(order, barsValid);

}

});

}

}

//------------------------------------------------------------------------

protected void checkBarsValid(ILiveOrder order, int barsValid) throws TradingException {

if(order.isClosedOrder()) return;

if(order.isPendingOrder() && order.getBarsInTrade() >= barsValid) {

order.Close(OrderCloseTypes.Expired);

}

}

//------------------------------------------------------------------------

protected double computeSL(byte orderType, double orderPrice) throws TradingException {

ExitMethod slExit = getStopLossExit();

if(slExit == null) {

// no SL

return Order.NOT_DEFINED;

}

return SQUtils.fixPrice(Strategy.getInstrumentInfo().tickStep, slExit.computeValue(orderType, Strategy, Symbol, orderPrice));

}

//------------------------------------------------------------------------

protected double computePT(byte orderType, double orderPrice) throws TradingException {

ExitMethod ptExit = getProfitTargetExit();

if(ptExit == null) {

// no PT

return Order.NOT_DEFINED;

}

double tickStep = Strategy.getInstrumentInfo().tickStep;

return SQUtils.fixPrice(tickStep, ptExit.computeValue(orderType, Strategy, Symbol, orderPrice));

}

//------------------------------------------------------------------------

private ExitMethod getStopLossExit() {

ExitMethod slExit = null;

for(ExitMethod exitMethod : ExitMethods) {

if(exitMethod.getExitType() == ExitTypes.StopLoss) {

slExit = exitMethod;

break;

}

}

return slExit;

}

//------------------------------------------------------------------------

private ExitMethod getProfitTargetExit() {

ExitMethod ptExit = null;

for(ExitMethod exitMethod : ExitMethods) {

if(exitMethod.getExitType() == ExitTypes.ProfitTarget) {

ptExit = exitMethod;

break;

}

}

return ptExit;

}

//------------------------------------------------------------------------

protected double computeSize(byte orderType, double price, double sl) throws TradingException {

MMFormulaBlock sizeFormula = (MMFormulaBlock) Size;

return sizeFormula.computeSize(Strategy, Symbol, orderType, price, sl);

}

//------------------------------------------------------------------------

protected ILiveOrder checkLiveOrderExists(int direction, boolean includeClosingOrders) {

int count = Strategy.Trader.getOpenOrdersCount(includeClosingOrders) - 1;

for(int i=count; i >= 0; i--) {

ILiveOrder order = Strategy.Trader.getOpenOrder(i, includeClosingOrders);

if(OrderFunctions.identify(order, Strategy, Symbol, direction, MagicNumber, Comment) && order.isMarketOrder()) {

return order;

}

}

return null;

}

//------------------------------------------------------------------------

/**

* this method is called only in Tradestation engine, to handle exits (SL, PT, etc.) as same as they are handled in TS.

* @throws TradingException

*/

public void OnApplyExits() throws TradingException {

ArrayList<ILiveOrder> orders = getOpenOrders(Direction);

ATM atm = Strategy.getATM();

boolean slPlaced = false;

if(orders != null) {

for(int i=0; i<orders.size(); i++) {

ILiveOrder order = orders.get(i);

boolean atmUsed = atm != null && atm.isApplicable(Strategy, order.getSize(), order.getSL(), order.getOrderType());

for(ExitMethod exitMethod : ExitMethods) {

if(!atmUsed || exitMethod instanceof StopLoss) {

if(exitMethod.setExit(order, Strategy)) {

slPlaced = true;

}

}

}

if(!slPlaced && order.getSL() != Order.NOT_DEFINED) {

// we have to set SL from order - handling if there is no SL, only for Trailing stop or Move2BE

int direction = order.isLong() ? -1 : 1;

byte orderType = (direction > 0 ? OrderTypes.BuyToCoverStop : OrderTypes.SellToCoverStop);

ILiveOrder slOrder = Strategy.Trader.Open(orderType, order.getSymbol(), order.getSL())

.setComment("SL")

.setMagicNumber(order.getMagicNumber())

.Send();

}

}

}

}

//------------------------------------------------------------------------

private ArrayList<ILiveOrder> getOpenOrders(int direction) {

ArrayList<ILiveOrder> orders = null;

for(int i=0; i<Strategy.Trader.getOpenOrdersCount(false); i++) {

ILiveOrder order = Strategy.Trader.getOpenOrder(i, false);

if(order.isPendingOrder()) {

continue;

}

if(OrderFunctions.identify(order, Strategy, Symbol, direction, MagicNumber, Comment) && order.isMarketOrder()) {

if(orders == null) {

orders = new ArrayList<ILiveOrder>();

}

orders.add(order);

}

}

return orders;

}

//------------------------------------------------------------------------

protected boolean engineSupportsDuplicateTrades() {

return Strategy.Trader.supportsDuplicateTrades();

}

//------------------------------------------------------------------------

private ATMExit tryCloneATMExit(ATMExit exit) throws TradingException {

ATMExit clone = exit.clone();

if(clone == null) {

throw new TradingException("Unable to create ATMExit object");

}

return clone;

}

//------------------------------------------------------------------------

protected boolean checkOpenPriceWithinRange(double openPrice) {

try {

SettingsMap settings = Strategy.getSettings();

if(settings.containsKey(MaxDistanceFromMarketHash) && settings.containsKey(MaxDistanceFromMarketPctHash) && ((boolean) settings.get(MaxDistanceFromMarketHash))) {

double maxPctDistance = SQUtils.round2((double) settings.get(MaxDistanceFromMarketPctHash));

double currentPrice = Direction > 0 ? Strategy.MarketData.Chart(Symbol).Ask() : Strategy.MarketData.Chart(Symbol).Bid();

double distancePct = SQUtils.round2(Math.abs(currentPrice - openPrice) / currentPrice * 100);

if(distancePct > maxPctDistance) {

Log.debug("Order skipped - too far from market. Open price: {}, Market price: {}, Max distance: {}%", openPrice, currentPrice, maxPctDistance);

return false;

}

}

}

catch(Throwable t) {

Log.error("Error while checking open price max distance", t);

}

return true;

}

}

{kind=link}

¡Buen trabajo!

¡Gracias Bentra !

Hola,

could you guide me how can i add this code to the exsisting strategy?