Hello, could you introduce yourself? What is your profession?

Hello, I am Bentra and I run the Darwin “SUG” on Darwinex. I also have a blog which is under construction at www.bentra.ca. I have recently made moves to focus mostly on trading but I still entertain web development or other software development contracts from time to time. Previously, I played poker professionally for many years which I believe helped a great deal to get me in the correct mindset (psychology and illusions from randomness, statistics-based decisions, the importance of sample size, making the mathematically best decisions when there are unknown factors at play etc.) for trading.

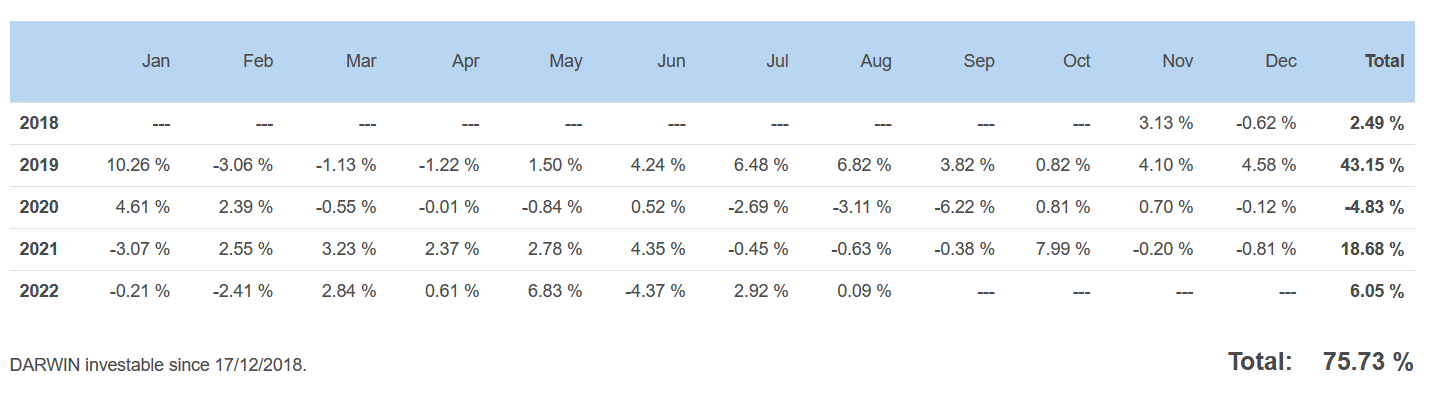

Current Trader’s Bentra real trading results

How did you start with algo-trading?

I started dabbling in trading stocks around 2007 but then I got sucked into forex by the advertisements about 24/hr markets etc. Began reading and dabbling in manual trading at first but eventually, I discovered mql and the programmer in me preferred automated trading.

How long it took to be successful, and what was the breaking point?

It was very gradual, by the time I had reasonable proof I was consistently (but only slightly) profitable in trading it was around 2017. I’m talking about track records of 3+ years and 1000’s of trades. So I guess you could say I must have been slightly profitable around 2014 in order to produce the beginning of a 3-year track record, but I didn’t know it for sure yet at that point. Mostly around that time (2005-2018), I was focused on poker though.

What do you like the most on algo-trading?

Well, I like that I can work whenever I want, I don’t have to be at work when the market opens if I don’t want. I’m really a programmer at heart, so giving instructions to computers is most comfortable for me. Algo-trading to me is about being creative and then running experiments which I really like. I can answer my own questions by running tests which I wouldn’t be able to do if I were a manual trader.

Could you tell us more about the workflow which you are using for creating and selecting the best strategies?

Every workflow is different. I don’t do any testing or filtering unless I have evidence that such a filter will help me in the future for building whatever specific type of strategy I am building. For me, a lot of time is spent figuring out what testing and filtering will help for each different scenario.

What is your philosophy of creating an optimal portfolio?

This is a work in progress for me. I think my drawdown from 2020 was from not being diversified enough, they were all one strategy type at that time. SQX is helping me fill the gaps there.

Are you using for strategies parameters recommended by optimization or you use a different way?

Lately, I’ve been just building and testing and then launching as is without any optimization. One day I’d like to experiment more with optimization but with the current limitations of optimization task plus with how easy it is to just generate new strategies from scratch (which are already coming out of the builder a little on the fit side from genetics and from sheer numbers,) I’m staying away from any optimizations for now. But I have high hopes for optimizations and walk forwards in the future, especially sequential optimizations.

Every portfolio sometimes suffers from drawdown. What is your approach to overcome it and maintain confidence in your robots?

Haha, well, hopefully, you already have 3 or 4 years of demo or small account trading in profit that you can look back on to derive confidence. (and if not, then stick with the small account or demo trading until you do.) So basically look at the bigger picture. Use any drawdown time as motivation to keep learning and testing and be skeptical about past assumptions, even if you’ve tested your assumptions, retest them if there’s any doubt!

That being said, if you are extremely confident your tests are giving slightly pessimistic results compared to real-life executions, and you are very confident that your out-of-sample testing contains no significant look forward or other bias, and you’re confident you have enough statistical significance then you can feel good about that. And if not then make it so! You can practice with a “build forward” technique similar to a walk forward but build+filter+test+filter then check your work on unseen data, then roll forward a year and do it again. If you can produce strategies that do well in absolutely unseen out-of-sample data ~70%+ of the time then you can be confident in that too.

Is there any source of knowledge which you would like to recommend to other traders?

SQX is a great knowledge source. Get creative and come up with your own theories and test them. I would also recommend Martyn Tinsley on youtube and books by Robert Pardo, David Aronson, and Kevin Davey.

Do you have any tips about what to avoid or be aware of in algo-trading?

Avoid not having enough statistical significance! Build symmetrically and on other markets for more if needed.

Would you like to share some recommendation to other algo-developers, what to focus on, etc.?

Build symmetrically even if you don’t intend to run short and long, just for the extra stats and make sure they’re really symmetrical. Get creative with templates. Come up with your own theories and questions, experiment, and test to answer and prove. SQX is a great tool for these things.

thank you Bentra !