Documentation

Applications

Last updated on 20. 11. 2021 by clonex / Ivan Hudec

Equity moving average simulation

Page contents

In this tutorial we will show you how to create and simulate equity curve control in What If Crosscheck .

What-If scenarios in StrategyQuantx is the tool that allows you to test various hypothesis of trading your strategy.

Equity control simulation function allows to simulate switching a strategy on and off based on the equity curve. The assumption is based on the hypothesis that is better to trade strategy if its performance is above its average. Good article dedicated to this topic is possible to read here.

Finished snippet you can download here.

Step 1 – Create new What if snippet

Open CodeEditor, click on Create new and choose List of trades column option- Name it EquityMATrading.

This will create a new snippet EquityMATrading.java in folder User/Snippets/SQ/Whatif

Step 2 – Define snippet parameters

Since we want to compute equity average, we need to include a parameter – MAPeriod that allows us to specify a period of the moving average.

@ClassConfig(name="() Equity MA Trading", display="Equity MA(#MAPeriod#) Trading ")

@Help("Help text")

public class EquityMATrading extends WhatIf {

public static final Logger Log = LoggerFactory.getLogger(EquityMATrading.class);

@Parameter(name="MAPeriod", defaultValue="10", minValue=2, maxValue=100000, step=1)

public int MAPeriod;

Step 3 – Implement filter(OrdersList orders) method

The filter(OrdersList orders) method is used to filter the original list of orders in the strategy. OrdersList is a class that stores the list of trades of a strategy and provides methods to manipulate with the list of trades. You can loop troght entire OrdersList and get data for very Order using method get(int index).

Here you need to pay attention to how you loop trough the list of orders. In our example, we are using the classic for loop, so we can not manipulate the orders list during the loop.

Instead, we create a temporary OrdersList ol where we store the trades that have met our conditions. We copy this orderslist at the end of the snippet into the main orderslist

Step 4 – Using Whatif snippet EquityMATrading

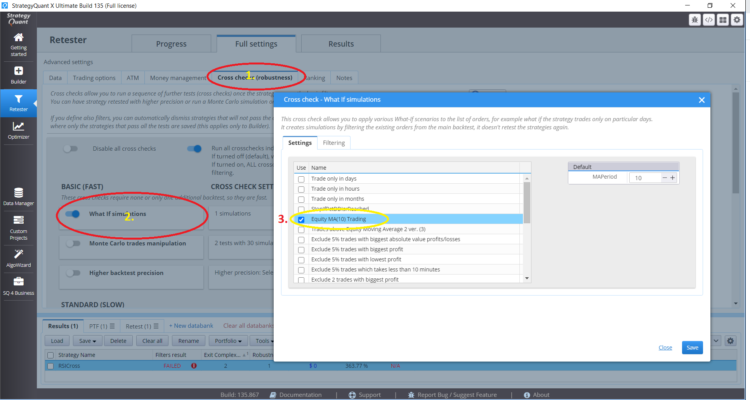

To add a snippet in Crosschecks you can use this snippet to simulate what would happen if you traded your strategy if its equity curve is above its moving average.

Full commented code of the snippet

package SQ.WhatIf;

import org.slf4j.Logger;

import org.slf4j.LoggerFactory;

import com.strategyquant.lib.SQTime;

import com.strategyquant.tradinglib.ClassConfig;

import com.strategyquant.tradinglib.Help;

import com.strategyquant.tradinglib.Order;

import com.strategyquant.tradinglib.OrdersList;

import com.strategyquant.tradinglib.Parameter;

import com.strategyquant.tradinglib.WhatIf;

import com.strategyquant.tradinglib.results.stats.comparator.OrderComparatorByOpenTime;

import it.unimi.dsi.fastutil.objects.ObjectListIterator;

@ClassConfig(name="() Equity MA Trading", display="Equity MA Trading (#MAPeriod#)")

@Help("Help text")

public class EquityMATrading extends WhatIf {

public static final Logger Log = LoggerFactory.getLogger(EquityMATrading.class);

@Parameter(name="MAPeriod", defaultValue="10", minValue=2, maxValue=100000, step=1)

public int MAPeriod;

@Override

public void filter(OrdersList orders) throws Exception {

// New instance of OrdersList in which we store trades that are above the moving average

OrdersList newOL = new OrdersList("AboveMovingAverage");

// We are looping trough whole OrdersList orders in order to compute Moving Average

for(int i = MAPeriod;i < orders.size();i++){

// Current last order we are deciding whether or not to go to newOL

Order order = orders.get(i);

// get balance of order

double balance = order.AccountBalance;

// filter balanced orders

if(order.isBalanceOrder()) continue;

double sum = 0;

// compute Moving Average of Equity

for(int k =1;k<=MAPeriod;k++){ /// robim ma , pricom zaratavam prvy orders.get(i-1) a posledny orders.get(i-MAPeriod) pri vyratavani MA

Order o = orders.get(i-k);

sum = sum + o.AccountBalance; // o.PL = order Profit/Loss

}

// average of equity

double avg = sum/MAPeriod;

// we are comparing get(i-1) with moving average

Order lastOrder = orders.get(i-1);

// if last order equity > average of equity

if(lastOrder.AccountBalance>avg) {

// we add order.get(i) to newOL

newOL.add(order);

}

avg =0; // reset average variable

sum =0; // reset sum variable

}

// sorting newOL by positions open time

newOL.sort(new OrderComparatorByOpenTime()); //// sorting orders by open time

// we are replacing OrdersList orders with OrdersList newOL and we recieve only trades above moving average

orders.replaceWithList(newOL);

}

}

Was this article helpful? The article was useful The article was not useful

very good 🙂