Completely different results with NT and SQ

3 replies

dirkdiggler

8 years ago #114934

Mark

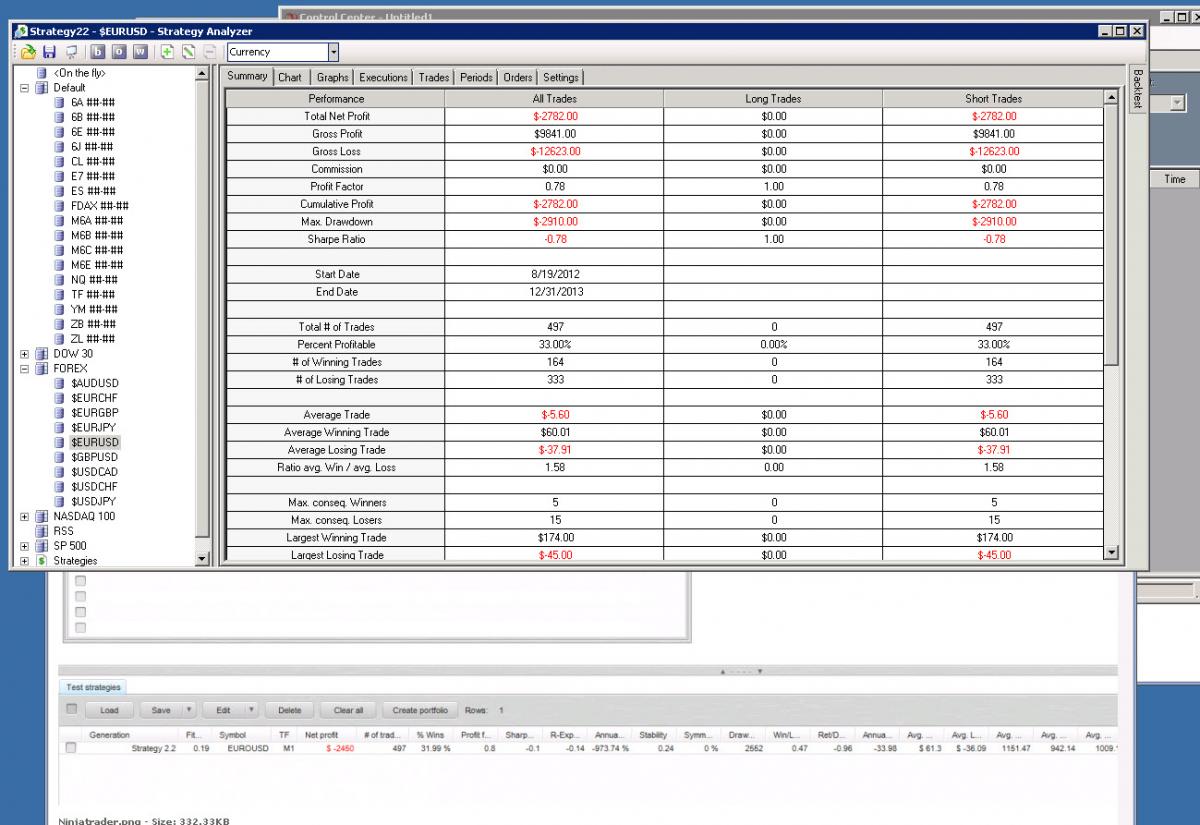

I exported EURUSD minute data from NT into SQ. Set slippage, spread and cost per roundturn to 0 for testing purposes. Generated a strategy and imported the CS code back into NT 7. Ran a backtest on that strategy with the same date range parameters and got two completely different results. I’ve been frustrated lately with your software because it has been extremely off with Ninjatrader. ~100 trades off is not acceptable. Half the time the backtests do not even come close to what SQ shows. And then of course they drastically fall apart in market replay over the same period. But that’s a different story.

See attached screenshots, str file and performance repots. I cannot upload the m1 eurusd data because of the 2mb forum limit but here is the dropbox link. https://www.dropbox.com/s/35chj4rwqqpe82k/%24EURUSD.Last.txt?dl=0

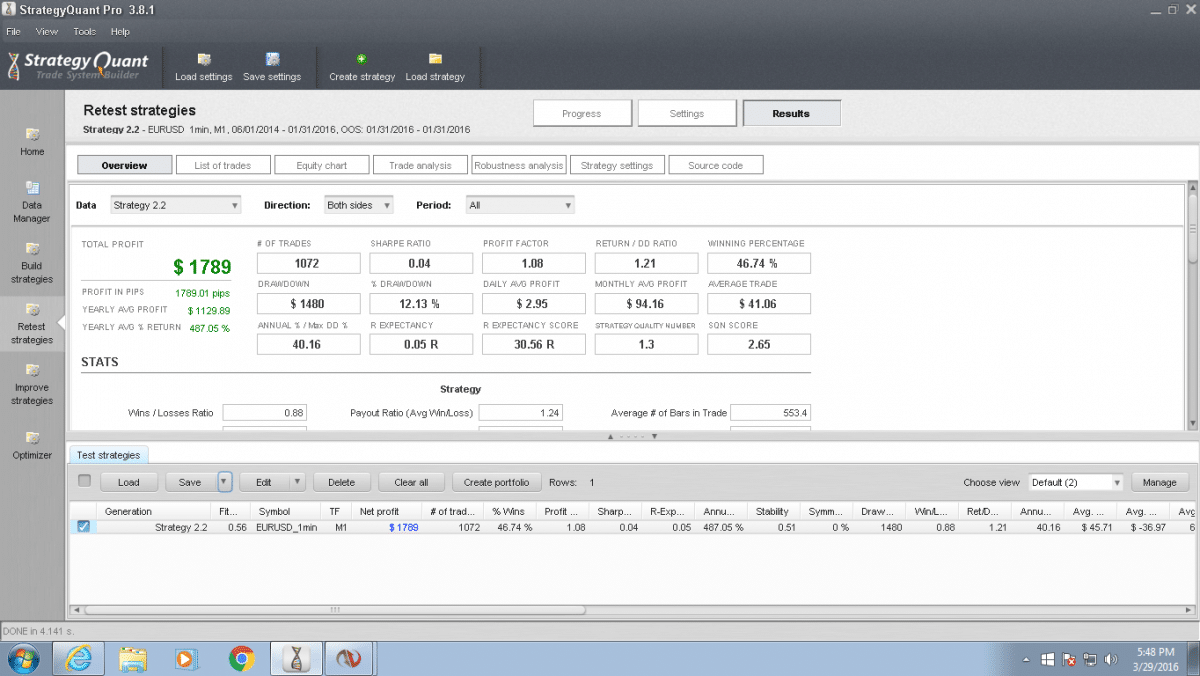

sq 2.2.png

sq 2.2.png nt 2.2.png

nt 2.2.png

mabi

8 years ago #136067

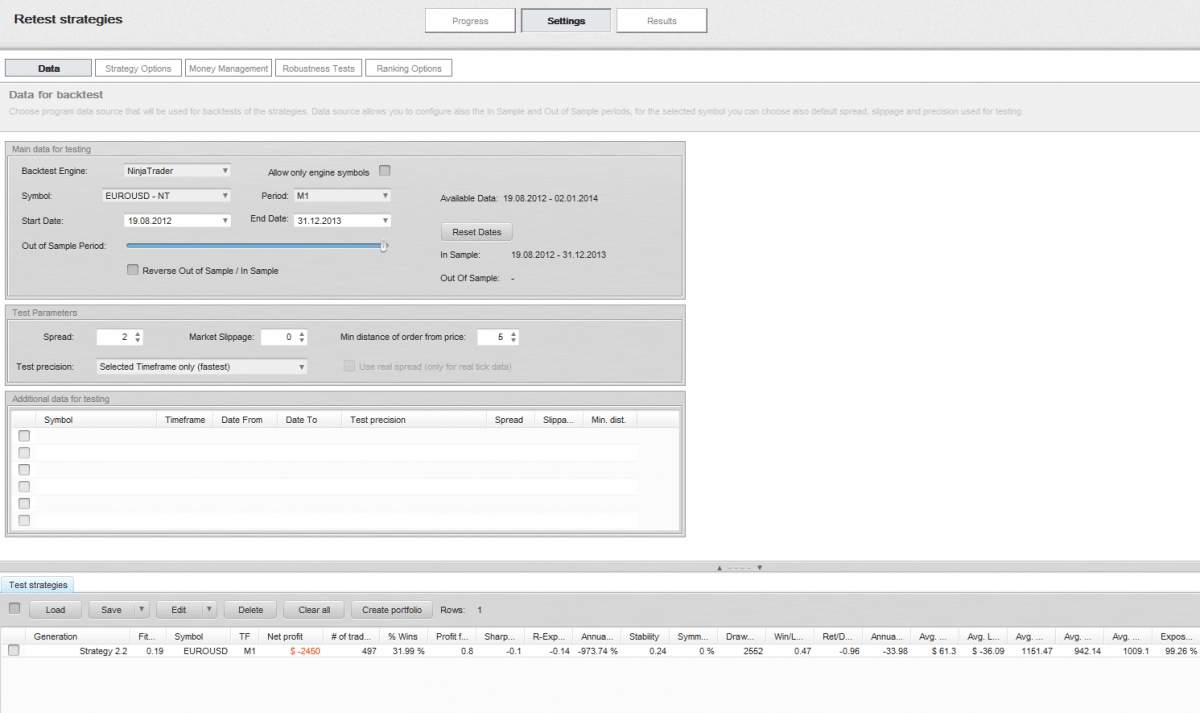

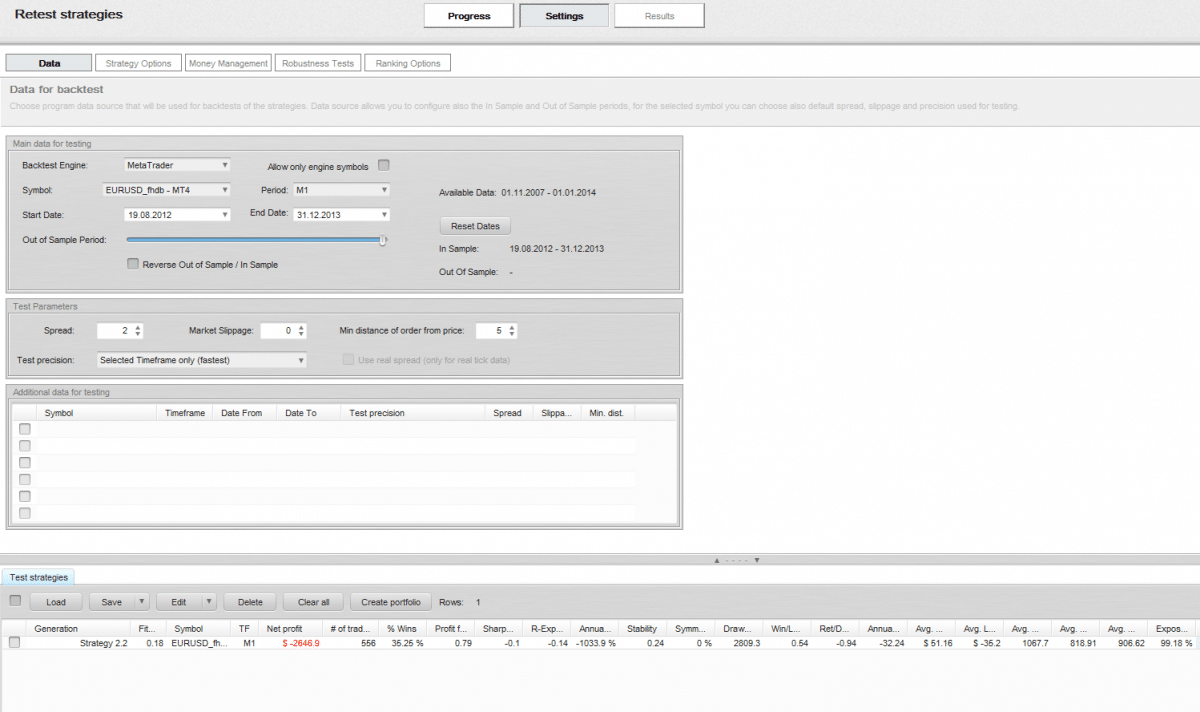

Ninjatrader.png

Ninjatrader.png Metatrader.png

Metatrader.png

Hi dirkdiggler,

I guess it is like this. If your first trade in the comparison is not on the same timestamp you will have a snow balling effect . Howe resistant your strategy is against this you can test in robustness test. Attached screendump´s is from your strategy with Ninjatrader M1 data and Metatrader M1 data. Very different test result, what happend was that one of them took a trade before the other and then it all looked different.

dirkdiggler

8 years ago #136076

An offset is not going to cause a snowball effect as it will just catch up to the next series of entry and exit parameters eventually. Plus the first and last trades line up. This is a major issue in their software and compatibility with ninjatrader. Even though it appears to integrate with Ninja it is essentially worthless. I’m not the first thread about this either. Especially due to the lack of tick level testing which I have to code manually to get an accurate backtest of where the fills would have actually been. Metatrader is the biggest piece of junk platform, I used it once to test it out. There is no comparison to ninja or even Tradestation.

Hopefully they will focus more on the issues with ninja with SQ4.

mabi

8 years ago #136099

I could not import your data file from NT. But since i do not create strategies on 1 min time frame i was interested to se how of it would be. As you see from the Screen dump i had exactly the same number of trades backtesting on NT with your strat in comparison with SQ on the same data imported from NT. Is 300 usd resonable difference ? I problably would be okey with 300 usd on 497 trades.

Comparison NT-SQ.jpg

Comparison NT-SQ.jpgViewing 3 replies - 1 through 3 (of 3 total)