How best to use this thing

15 replies

jpcoder

4 years ago #255005

I’m on a trial of the StrategyQuant software and as of yet have not found a way to use this thing to generate a profitable strategy. Are there some tutorials somewhere that explain how best to use this software to get descent results? I’ve heard about some course that comes with the purchase of the software, but it doesn’t make sense to purchase the software just to find out how to use it. What good is a trial without being able to use it and evaluate it’s worth? If it’s possible to generate profitable strategies then I could justify the cost, but right now I can’t see that.

tomas262

4 years ago #255011

Hello,

you can generate some basic strategies just by using the “default” setting. Do you run the latest version 126?

What instrument and timeframe did you test to run the builder?

jpcoder

4 years ago #255012

Yes, running 126. I’ve tried Default, Market and some of my own combinations. I’ve tried EURUSD and GBPUSD on multiple time frames from 15m to D1.

jpcoder

4 years ago #255013

I’m also not sure what to expect from a strategy that this tool will generate. What type of return it typical?

hankeys

4 years ago #255015

one strategy means nothing – we are mostly traders of portfolios – more diversified strategies traded together in 1 account

return? this is equation of your capital and willingness to risk

You want to be a profitable algotrader? We started using StrateQuant software in early 2014. For now we have a very big knowhow for building EAs for every possible types of markets. We share this knowhow, apps, tools and also all final strategies with real traders. If you want to join us, fill in the FORM.

Gianfranco

4 years ago #255018

portfolio example. 2 months. the most profitable strategies for now are on DAX and xauusd. because there’s little movement on the other assets. it’s obviously not the first portfolio I make… it takes a lot of effort

knowledge of the markets on which you want to build strategies. not all assets are the same… but I have so much to understand. even though I’ve been operating in the markets for several years. I still miss the touch that makes the difference…..

for now discrete results

anyway pretty in line with backtests

different results with different brokers

also this is a job to find brokers for your purpose

ivan

4 years ago #255019

I usually use the Net Pips column because Net profit depends on other factors too

also very important is to put the profit in the context of time, in what time was that profit made. To have e better picture, i divide the net pips to number of trades, for example 500 pips on 5 trades, that’s 100 pips per trade. If for example the strategy makes 100 pips on 50 trades, that’s garbage.

Also, in what time interval was that profit made, it can be 100 pips per week or per month or greater.

A net profit or a net pips performance without the number of trades or time interval, one cant asses the performance

Timisoara, Romania

3900X 3.8 Ghz 12 cores, 64GB RAM DDR4 3000Mhz, Samsung 970 EVO Plus M.2 NVMe

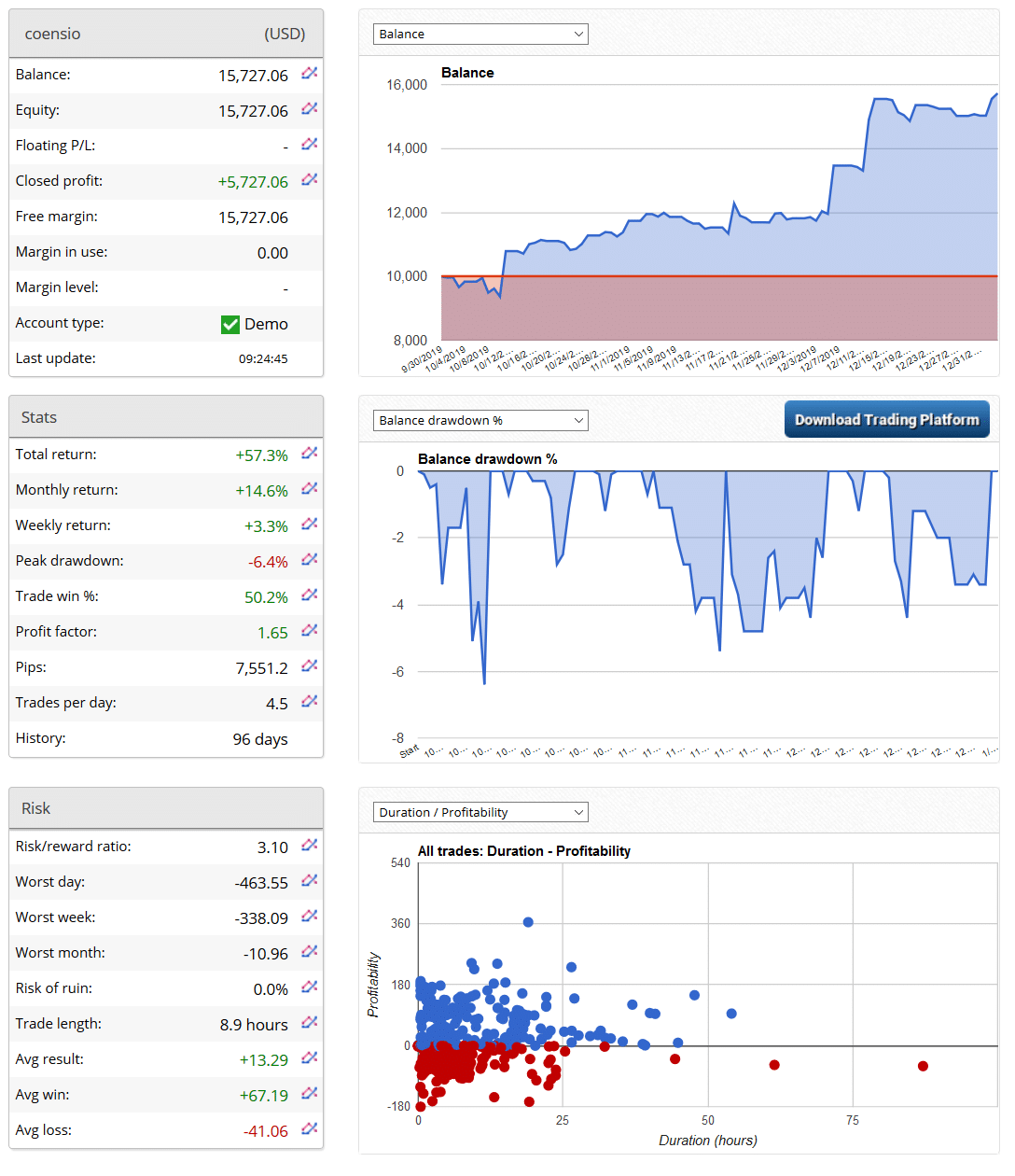

coensio

4 years ago #255021

Yes indeed we also have some evidence that strategies from new SQX can easily ‘beat’ the market giving a nice winning edge, but ‘beating’ your broker is the whole different story 😉

So yes you could say that: StrategyQuant platform “works”.

However, about the timeline (based on my own experience):

* It will take you several months of full dedication to master SQX features and feel comfortable while operating the platform.

* It will take you another several months to build you first portfolios (I recommend to aim for at least 50…100 uncorrelated systems on as many different markets as possible)

* It will take you another few months maybe even years to forward test your workflows on a real broker and real account(s)

* Probably it will take you 1 to 2 years to start making(or losing) real money 😉

This is a false statement.

Gianfranco

4 years ago #255023

I stirred the waters for a simple photo… it wasn’t my intention. it is a simple portfolio of a person who is trying to be profitable with automated strategies. my observation was that I’m having better results with dax and gold with other assets I’m not satisfied …

and it would also seem with sp500… but not with currencies splecially with eurusd

ivan

4 years ago #255046

whenever a beginner has this typical problem, in investigating, 2 major possible problems must be cleared out of the way

first: on what hardware was the generating done? we must eliminate the possibility that the generating was done on a too weak procesor

second: what method or how was the final assessment/evaluation of the strategies performed? the user, in this case, Jon Jones, reached the conclusion that the strategies dont work. How was this conclusion reached ? we must eliminate the posibility tat the stratgies work but the evaluation on the real test account was flawed.

@Jon Jones: you were a bit vague and too short in your last statement. We understand that a generation process took place. Can you tell us a bit more on what happened next ?

Timisoara, Romania

3900X 3.8 Ghz 12 cores, 64GB RAM DDR4 3000Mhz, Samsung 970 EVO Plus M.2 NVMe

ivan

4 years ago #255047

and last but not least, its important to understand the generation process itself. Its like hitting the gates at skiing on a certain distance. You must hit as many gates possible on that distance. If you stop the generation halfway, there is a great chance, the strategies in the databank wont pass the filter stage and Monte Carlo and you are either left with 0 strategies, or with flawed strategies if you decide to use them anyway although they didn’t pass the filters.

Almost in every case, the speed of the generating process is highest at start, lets say 300/hour or 200/hour and decreases constantly (although with small ups and downs) until after a few days it drops to lets say, 20/hour. Only then you have the certainty that you harvested most combinations. If you stop sooner, you only harvest a portion m that pair and timeframe and the quality of the strategies is lower.

Timisoara, Romania

3900X 3.8 Ghz 12 cores, 64GB RAM DDR4 3000Mhz, Samsung 970 EVO Plus M.2 NVMe

ivan

4 years ago #255049

every pair and timeframe has a different “length” and a different number of possible combinations because it depends on many factors, precision used, building blocks, how many years is the history but its important to “harvest” most of the possible combinations. An incomplete harvest must be avoided because its time and electricity wasted

Timisoara, Romania

3900X 3.8 Ghz 12 cores, 64GB RAM DDR4 3000Mhz, Samsung 970 EVO Plus M.2 NVMe

Jason

3 years ago #258109

Thanks Ivan, that makes sense. I’m also on a trial version. What kind of “strategies per hour” is considered reasonable?

I appreciate this depends on many factors including data set length, timeframe etc. Ive seen some of the support videos in the 4 million range whereas Im getting around 100k to 200k initially using 15min bars on a 3 year data set. I have no reference to measure against so I dont know if thats slow or OK.

I’m using an i5 which obviously isn’t the fastest by a long way but if decent results depend on a computer system upgrade then thats a bigger consideration for me in purchasing SQ.

jaukb

3 years ago #259549

From my experience, its just not possible to extract a accurate perception about if this software works at all.

And then your asked to cough up big $$$?

sorry no.

kasinath

3 years ago #260350

The product has a lot of promise and looklooks great. See this 4 part video series that walks through the creation of sub portfolio. They are using strategy quant x.

This video has inspired me to buy the product, but first I need to know if the indicators I use are available in the product. I posted a question but it is still being moderated. I hope someone will moderate / approve my post and then reply.

Andre Alexa

3 years ago #267779

*Thx for the info shared here. I am watching the thread*

Viewing 15 replies - 1 through 15 (of 15 total)