Many strategies are contrary to common sense

1 replies

eastpeace

4 years ago #248983

I have had an interesting observation recently. Many of the strategies that SQ generated would be contrary to common sense.

I run some SQ-generated strategies in MultiCharts, because I feel that the equity curve is not bad after some tests in SQ.

Then I found an interesting phenomenon.

// Rule: Trading signals

//——————————————————————

Value1= SQ_Lowest(TypicalPrice, 10)[1];

Value2= SQ_Ichimoku(9, 26, 52, 1)[4];

LongEntrySignal = (Value1 <= Value2);

Value1= SQ_Highest(TypicalPrice, 10)[1];

Value2= SQ_Ichimoku(9, 26, 52, 1)[4];

ShortEntrySignal = (Value1 >= Value2);

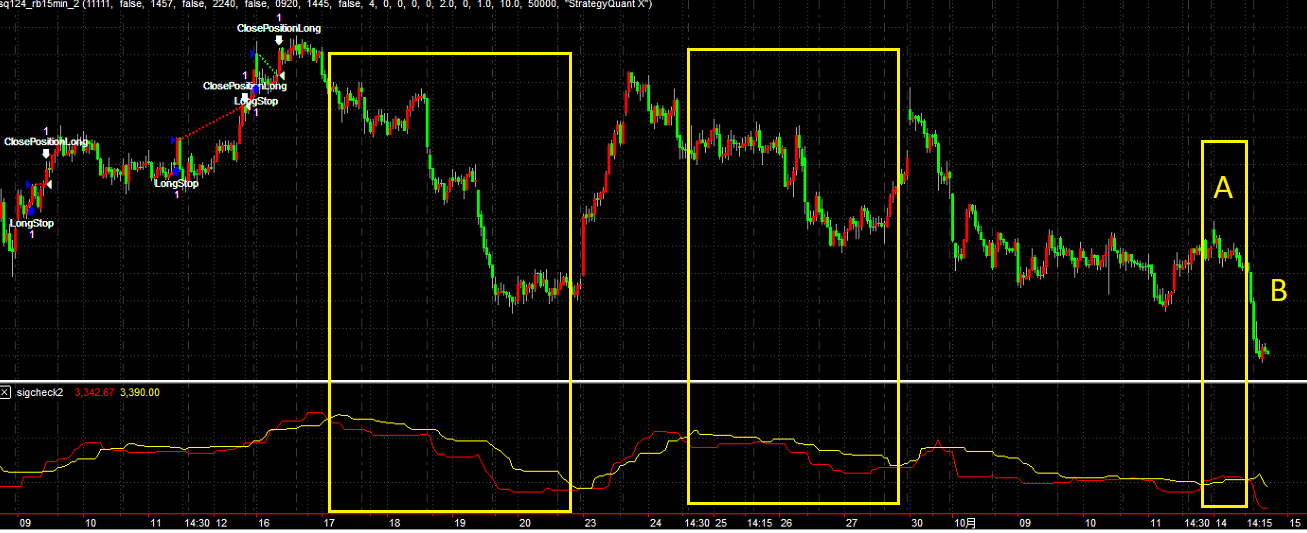

In stage A, the strategy will generate sellshort stop order, and when the price begins to fall, the strategy generates buy entry stop order.

As we know, when the price is falling, short selling is a normal choice. So I plot the long and short entry signal. When value1 is smaller than value2, it tends to fall quickly.

But the strategy will use it as a long entry signal

Many SQ-generated strategies have this problem. They only capture some small opportunities and miss some profitable trading opportunities.

How to avoid generating strategies like that?

tomas262

4 years ago #248986

Hello,

I see nothing wrong with this. This looks like a kind of reversion type of strategy which is quite opposite of a momentum type. When the market falls we tend to fade it and expect a ‘reversion’ back to mean.

The best way to avoid it is to design strategies using ‘idea first’ concept. That means you setup a strategy concept (template) using AlgoWizard and let SQ to work on it and further develop it

Viewing 1 replies (of 1 total)