Please ‘rate’ my new strategy EURUSD H1

28 replies

coensio

4 years ago #242350

Below few screenshots of one of my new strategies (using my new approach), so without saying anything upfront (to prevent biasing you)…I’m asking you what is your opinion on this kind of strategies, please rate it before I will add it to our databank or not..

Is it any good? or bad? or ugly? 😉 Is this tradabe in your opinion? What would you improve?

The only thing I’m thinking about is to adapt DOW-filter and get rid of monday trades….

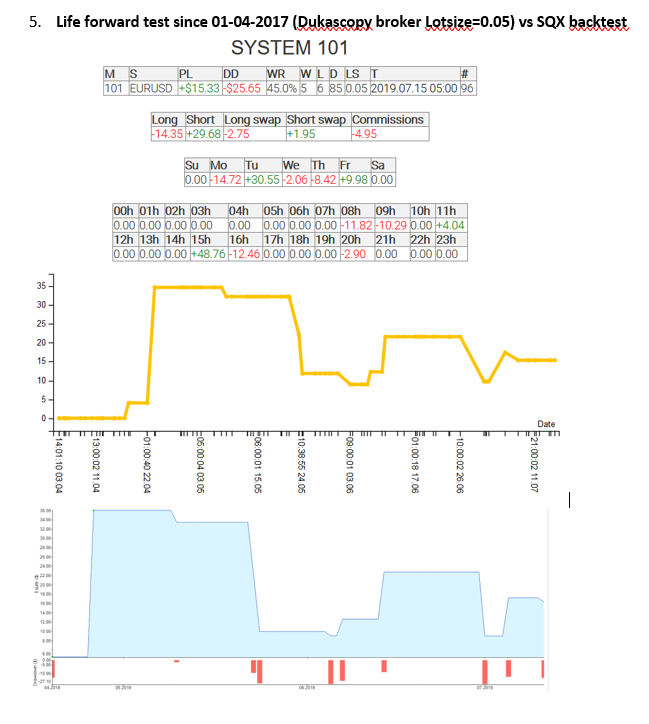

So far I have only just few trades on the life account…but so far the correlation vs BT is pretty OK.

This is a false statement.

Laur2000

4 years ago #250260

Difficulties with attachments… only 5MB…

Laur2000

4 years ago #250265

next

Laur2000

4 years ago #250276

next strategies

Laur2000

4 years ago #250281

more

Laur2000

4 years ago #250285

final

hankeys

4 years ago #250289

to Laur2000 – there is nothing much to say, they look to me good, but without knowing your workflow, hard to say

only one thing – you have only one market, one TF – many strategies are too correlated, so you have duplicities and similar strategies

You want to be a profitable algotrader? We started using StrateQuant software in early 2014. For now we have a very big knowhow for building EAs for every possible types of markets. We share this knowhow, apps, tools and also all final strategies with real traders. If you want to join us, fill in the FORM.

Laur2000

4 years ago #250331

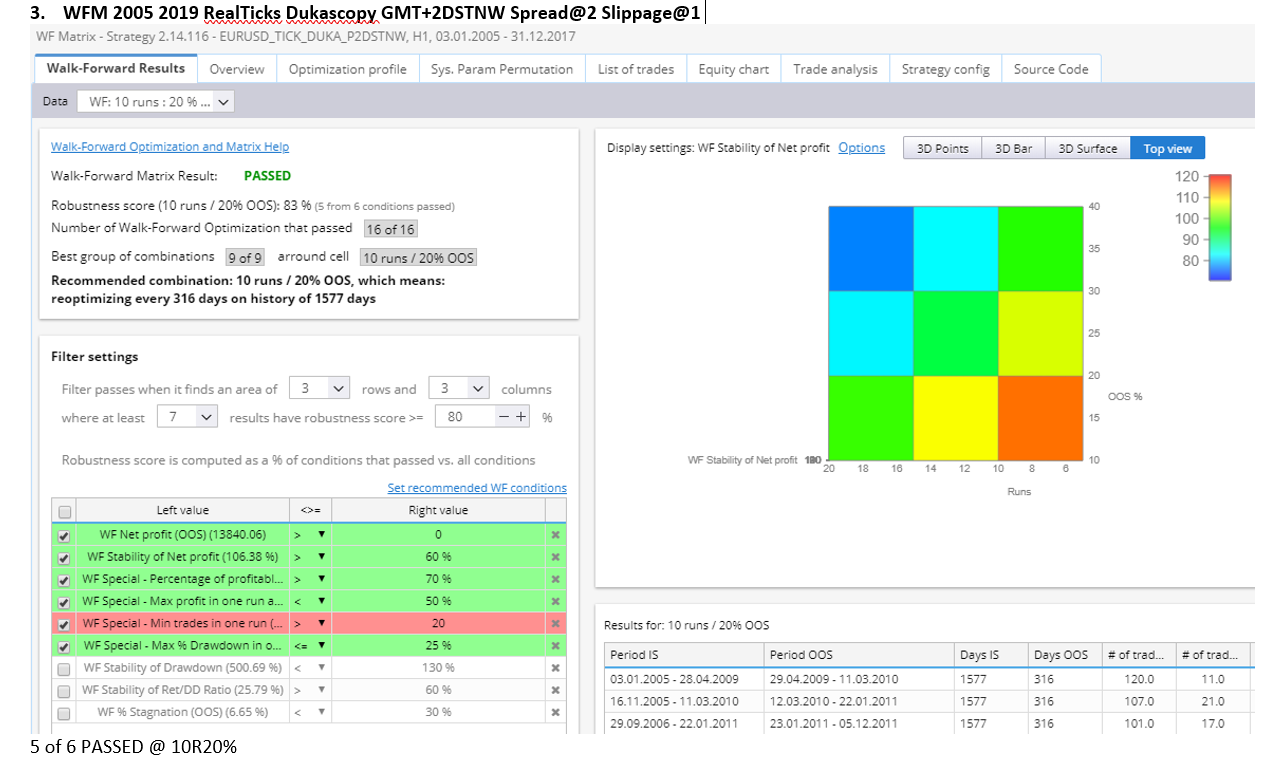

0. Strategy generation (2010-2016)

1. OOS1: This test will run all strategies on an Out-Of-Sample period (5 years of data 2005 to 2010)

2. Slippage at 3: Test at higher slippage of 3pips.

3. GBPUSD market: Test on a different market.

4. A: TF_M30: Test on a lower TimeFrame. B TF_H4: Test on a higher TimeFrame.

5. MC random trades: Monte-Carlo randomized trades test. (200)

6. MC skipping trades: Monte-Carlo random skipping of trades test. (200)

7. MC random parameters: Monte-Carlo randomized strategy parameters test. |(200)

8. MC random volatility ATR: Monte-Carlo randomized market volatility test. (200)

9. MC random slippage: Monte-Carlo randomized slippage test. (50)

10. MC random spread: Monte-Carlo randomized spread test. |(50)

11. Last OOS2 test: Final test using 2 year ‘unseen’ market data. (2017-2019(

12. WFO

13.WFM

hankeys

4 years ago #250336

looks good…delete duplicities and move to another TF or market

You want to be a profitable algotrader? We started using StrateQuant software in early 2014. For now we have a very big knowhow for building EAs for every possible types of markets. We share this knowhow, apps, tools and also all final strategies with real traders. If you want to join us, fill in the FORM.

Gianfranco

4 years ago #250337

hello…. am I wrong or do I see sqx files in the xml and csv only strategies? or you just want an opinion on equity

hankeys

4 years ago #250345

you need to make a retest of his strategies, dont know why, but i see only zero values, but after retest its ok

You want to be a profitable algotrader? We started using StrateQuant software in early 2014. For now we have a very big knowhow for building EAs for every possible types of markets. We share this knowhow, apps, tools and also all final strategies with real traders. If you want to join us, fill in the FORM.

Fabrizio D'Aprile

3 years ago #258467

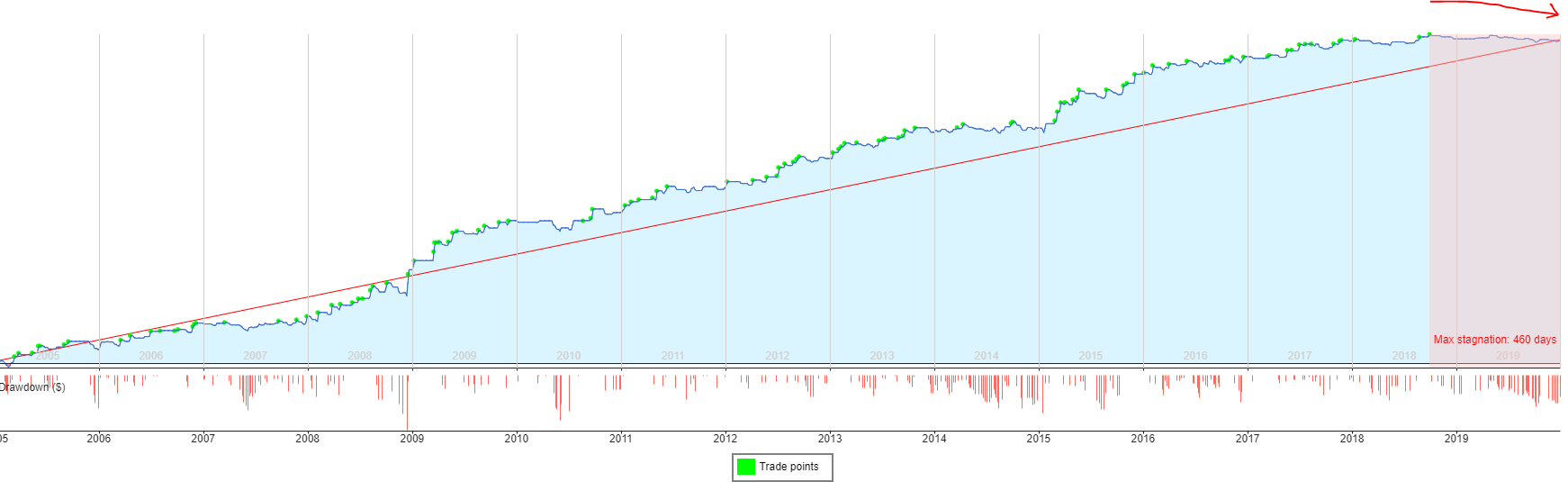

Okay, but we need to optimize it correctly with enough OOS data – these current settings are curve-fitted to 2003-2018:

SteveChou

3 years ago #258847

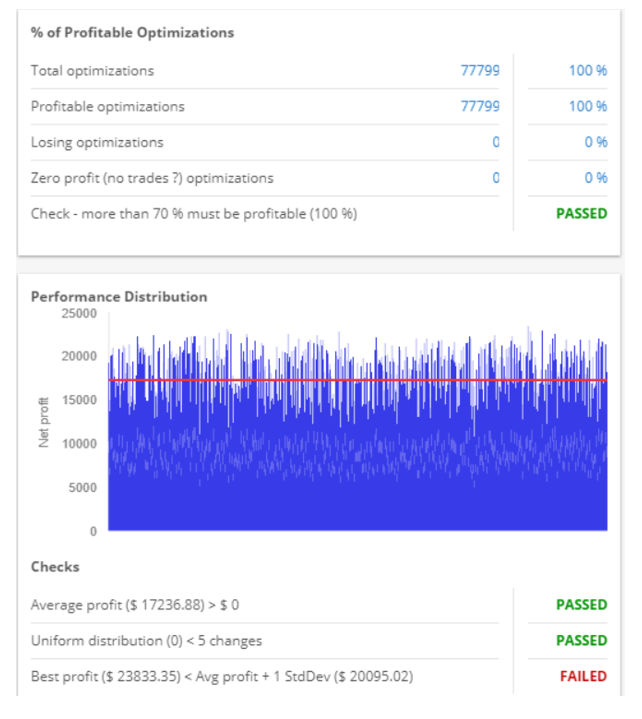

The last check on performance distribution fails. What factor do you use. I increase the factor most time to 2 or 2.5.

Yes indeed, I’ve used the standard setting equal to 1, with this standard setting most of strategies will fail on this check..increasing it to 2.5 helps to pass this test in majority of cases.

Do you compare the trades with metatrader4?

Yes I do a quick check, but no TDS….

I feel this check option “performance distribution~ best profit < average profit+1 std” was very strange, because if the performance distribution is an normal distribution.

I think it is very hard to let the best profit < average profit+1 std. Am I right?

Or it is easy to do?

mabi

3 years ago #258874

Probably my last forum comment because I am wasting too much time testing hypothesis based on what I read here and I no longer use the excellent SQ for development (it remains an absolutely outstanding tool) so it is a daft thing to continue to read these posts. The current hypothesis is: “the strategy above is 2 for 1 penny/cent, they can be built within 2 hours from start to finish”; I’m an hour and a half in the process, running Consenio’s WF strategy config’ on strategies I’ve generated but what is the point? By now you must ALL realize generating good looking models meeting with the requisite criteria of an excellent looking model is actually a walk in the park, it is easy to do. We all know this. The thing is most traders are posting vanity backtests – whether here or elsewhere – for many many months or years. Some post good strategies with 1-month half-lives so one can download them or give them to associates to use for 2-3 months then consign them to the bin. Where are the live trading results to back up the vanity backtests; surely the live results are for months or years? There are no longer live results because if the above strategy fails, we will not hear about it again if it succeeds we will. Basically, an additional form of bias. I’m suggesting there is a great deal of self-delusional going on here. Based on the available evidence (and to be honest, there really is not a lot) Hankey is the best 100% SQ built algo developer and trader on the forum. This is based on available evidence. On average Hankey can achieve a profit factor of 1.05 to 1.15 in live trading with stagnation periods to match; in general, this is the reality. I sincerely consider a consistent and reliable 1.15 profit factor in live trading to be a big accomplishment and I’m confident this is more than 99.9% of traders using SQ are managing to achieve IF THEY ARE COMPLETELY HONEST WITH THEMSELVES meaning they do not conveniently forget about the bad models’ equity decimation of the past. Do you think a model with a profit factor of 10 gives you a better chance of achieving a higher profit factor in live trading? Do you think modeling a profit factor of 1.15 to 1.3 gives you a better chance of deploying a model that performs as per backtest on the live account? Or haven’t you even bothered to empirically test it, relying instead on unfounded assumptions, with the arrogance of knowledge with no evidence of knowledge thereby deterring those who can actually help you from lending the vital helping hand? 1-year prediction – I’ll write my next comment then: 1. Hankey’s average PF will increase to 1.15 to 1.2 enough to make a person fabulously rich over the course of time; 2. vanity backtests and the kudos from posting them will remain the dominant force on the forum. Vanity backtests are 2 for a penny just like mine below! However, I can virtually guarantee (99% confidence) the performance below will continue to mirror the backtest but I rely on the empirical method and not unfounded assumptions. I’ll post the live results in 12 months time when I next post. Green pips all and I hope you develop!!!

Notch! any preview from your live results it is closing in on one year 🙂