Great strategy but Metatrader backtest is not the same

6 replies

alanhere

3 years ago #267194

Hi All,

The other day I got this strategy, between 2015 and 2020 it’s got a fitness rating of 0.9

I ran this in the strategy tester using TDS and Dukascopy data (same as what is being used to make this EA) but the Metatrader results are very different. I’ve adjusted spreads and played around with the parameters in TDS. Other strategies I’ve not had issues with but this one looks so great and backtests are so different. Can anyone figure out why?

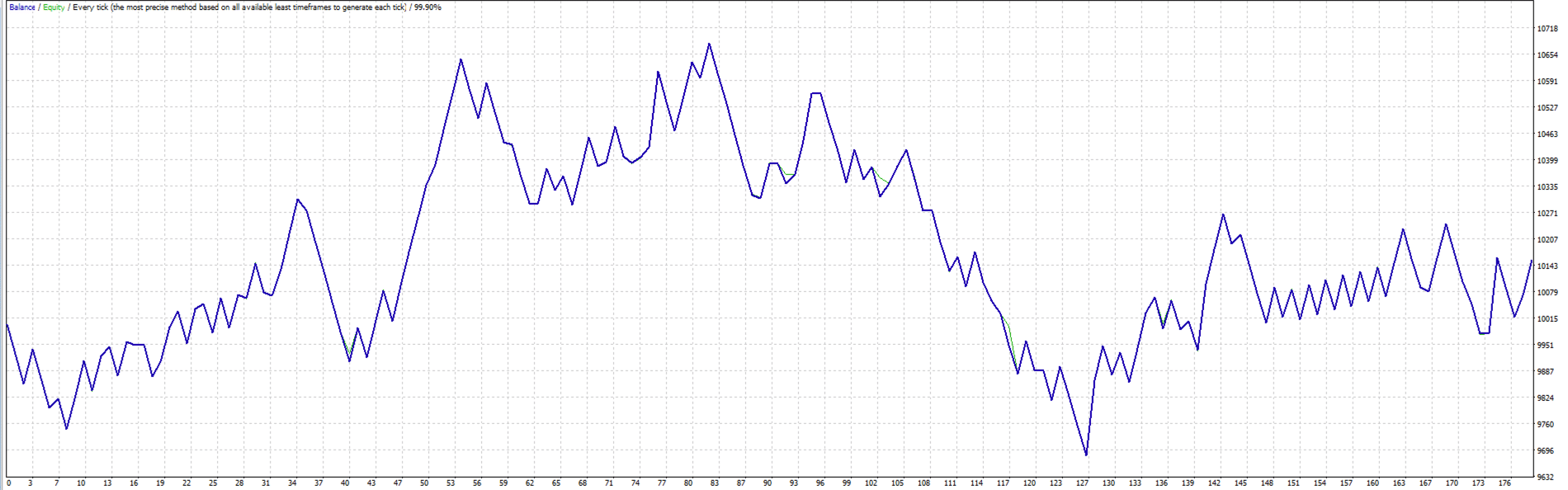

Metatrader strategy tester pics – 2018 to 2020

I include the SQX file.

What I have checked

- Spread dependent. EA doesn’t scalp for a few points, stops are 70 pips and profits targets around 80 pips so not dependent on fast brokers with low spreads

- Time restrictions and dependency on broker times. All my SQ is converted to same time as my broker

It would be great if you could find out what is wrong

tomas262

3 years ago #267208

Hi,

not sure what you could be doing wrong. I have just retested 2020 and get almost 95% match which is acceptable for most strategies

hankeys

3 years ago #267214

problem will be with your backtest in SQX – if i retest the strategy on my GBPUSD UTC2 data with 1M precision i am getting totally different results

if i make tick backtest on GBPUSD data on TDS, my restults are the same

so you are doing something wrong right in the SQX itself – you reall use cloned data to the correct timezone of your broker? or why to you use tick data?

sending everything i made for the comparation also the comparing EQ curve – SQX backtest vs tick backtest in TDS – its the same

You want to be a profitable algotrader? We started using StrateQuant software in early 2014. For now we have a very big knowhow for building EAs for every possible types of markets. We share this knowhow, apps, tools and also all final strategies with real traders. If you want to join us, fill in the FORM.

alanhere

3 years ago #267223

Thanks, can you let me know if you’re using TDS or the standard Metatrader tester?

alanhere

3 years ago #267224

problem will be with your backtest in SQX – if i retest the strategy on my GBPUSD UTC2 data with 1M precision i am getting totally different results if i make tick backtest on GBPUSD data on TDS, my restults are the same so you are doing something wrong right in the SQX itself – you reall use cloned data to the correct timezone of your broker? or why to you use tick data? sending everything i made for the comparation also the comparing EQ curve – SQX backtest vs tick backtest in TDS – its the same

Thanks Hankeys for your efforts and thank you for sending everything over. It’s a promising looking strategy but I want to be sure it’s going to work

hankeys

3 years ago #267227

its TDS…using UTC2 data as timezone

seems, that you are not using cloned data…so its only looking promising, but for UTC2 brokers its not

You want to be a profitable algotrader? We started using StrateQuant software in early 2014. For now we have a very big knowhow for building EAs for every possible types of markets. We share this knowhow, apps, tools and also all final strategies with real traders. If you want to join us, fill in the FORM.

alanhere

3 years ago #267233

its TDS…using UTC2 data as timezone seems, that you are not using cloned data…so its only looking promising, but for UTC2 brokers its not

Thanks Hankeys.. I got it, I’m going to run all my strategies again with multiple timezones and see what they look like..

Viewing 6 replies - 1 through 6 (of 6 total)