My best portfolio on demoaccount

11 replies

tnickel

5 years ago #237362

Hi,

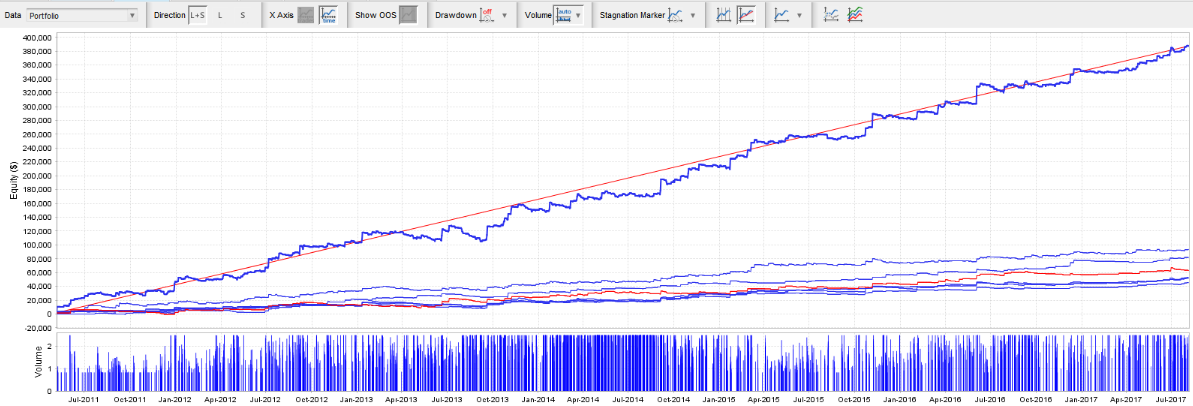

here is my best Portfolio on demoaccount.

If you want you can install this on demo or realaccount.

I attached the mq4 stratgies this Posting.

I attached a Analysis of this strategies too.

please install this strategies on demo/real accounts. We can compare the results and search the best broker for this.

I will be happy for Response

https://monitortool.jimdofree.com/

Ilya

5 years ago #237371

Hi Thomas,

First of all, I’d like to thank you for sharing. Honestly I never understood all the “Secrecy” people have about their strategies or methods, there is nothing to lose by sharing knowledge, all that can happen is that you benefit other people.

Secondly, the equity curve looks nice, each strategy is interesting by itself and they seem to combine well. Personally, I’d be happy to get STR files in order to check robustness, as I’ve found that that’s the most important test that creates a difference between past results and live results. I would not put any strategy on a real account without making sure it is robust, able to withstand minor changes of conditions, volatility, spread, and can even stay in the plus when trades are skipped, and entry/exit parameters change slightly. I do understand your lack of will to give out the STR files though, it is obviously for you to decide.

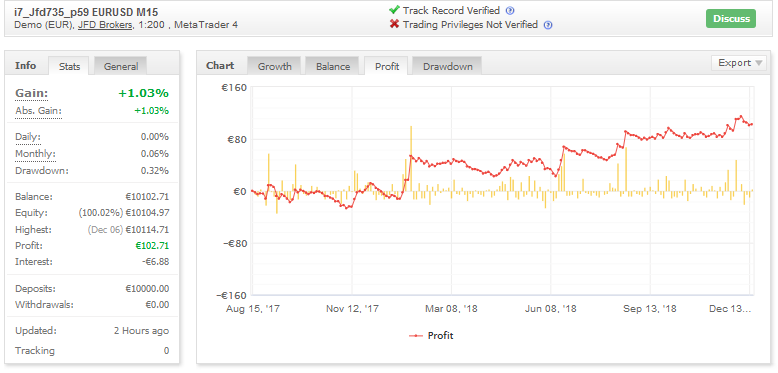

I’ll be following your myfxbook demo portfolio, could you drop a link?

Cheers

Ilya

Ilya

5 years ago #237372

Also, since the account only gained 1% in 4 months, I assume you just use a small lot size per trade for the demo? I wonder if you can publish a backtest using at least 1% risk per trade?

tnickel

5 years ago #237373

Here you can download this

https://drive.google.com/drive/folders/1_9RBGfpFQr3d1fkwNZSiomJ_OWWWip9M

https://monitortool.jimdofree.com/

Ilya

5 years ago #237374

https://strategyquant.com/forum/topic/my-best-portfolio-on-demoaccount/#237373

Thanks 🙂 I’ll be testing them through the week with my workflow and come back with my 2 cents.

Ilya

Schutten

5 years ago #237375

Hi,

I have been developing for quite some now as well. First with SQ3, now slowly moving to SQ4 as well. I have been running a demo account for only 2 months or so, to early to draw conclusions. Currently I am trading about 8 pairs in a portfolio on H1 chart. Robustness is always a issue and a challenge to overcome. As there are no STR files available (which I understand) there is not really a way to ‘challenge’ the systems besides backtesting them on a different set of data. I have tickdata available for IC markets. I will have a look at that…

hankeys

5 years ago #237423

many times i was trying to start bigger cooperation and sharing the strategies, because it doesnt make sense, that we dont want to help each other…for now have no luck with old SQ

now its time for SQX cooperation, because settings are endless 🙂

but trying to find something like “best broker” is nonsense – if you are trading only forex pairs, you will get to conclusion that the best broker is one, from which you can withdraw your money 🙂 spreads, slippages, other costs dont differ to much

trading indices is a bigger questiong, there are huge diffs…

You want to be a profitable algotrader? We started using StrateQuant software in early 2014. For now we have a very big knowhow for building EAs for every possible types of markets. We share this knowhow, apps, tools and also all final strategies with real traders. If you want to join us, fill in the FORM.

Schutten

5 years ago #237591

I agree with ‘best broker’ difference. However there is a difference in broker feeds. Dukascopy for example has much more ticks then a average broker. Its always good practice to build ea’s on data from the broker which will be used for trading.

afhampton

5 years ago #237726

Hi Thomas:

Thank you for sharing your strategies. May I ask how you have your SQX build process set up? I’m quite familiar with SQ 3.8 and am getting familiar with SQX Build 116. Would you be willing to share your build settings config file as a reference? I would like to compare it to how I am set up to note the differences. I’m currently building on the EURUSD H1 with only two filters on Dukascopy M1 data from 2003.05.05 – 2018.12.21. The two filters are profit factor >= 1.3 and # of trades >= 500. Not doing any crosschecks at this point and the generation method is Random. Still very few strategies are making it through. I would like to see what you are doing that I am not that might make a difference.

Thanks for considering.

Aaron

tnickel

5 years ago #237740

hi afhampton,

this strategies are build with sq 3.8.1

I have done this work in a team. I am not allowed to tell all details.

PF 1.3 and #trades >=500 are good filters, symetry and stability are good filters too.

With 4.X I don´t found good strategies at the moment. After my filtering all strategies are killed with 4.X. 4.X have so many nice features, I think it will take a while to generate good strategies with this software.

The pfd book “How to trade profitably in forex using StrategyQuant software ” descripe all what you need for 3.8.2

To find the optimum filtering we need a tool or analysis software. I have written a tool two years ago to find optimal filter parameters. But this was a lot of work. I stopped the project after a while. I don´t have the time to complete this software ( I hope that mark frick will write a similar software to find the optimal filtering process)

At the moment it is only generate, filtering and test on demoaccount. This is a very difficult way.

The problem of this M15 Portfolio is the spread and slippage on real account. It will be interesting if this portfolio is profitabel on real account or not.

thomas

https://monitortool.jimdofree.com/

afhampton

5 years ago #237741

Thank you for the response Thomas. I certainly understand about not being able to share the settings. No worries. I’ve got a pretty effective setup for 3.8.2. It was more SQX that I was interested in.

It sounds like you and I use a very similar approach to performing robustness testing based on Zdenek’s book and video course. I have worked through both of them quite extensively and built an excel spreadsheet to guide my process. That worked fine for strategies built on 3.8.2 but SQX requires us to approach it a little differently. Still working out my process for that but need to get the build/generation optimized first. It seems that that is where some of us need a bit more coaching with SQX. With one config, it produced over 2000 strategies in a few hours that passed my two basic filters. Then, once restarted (without making any changes), it only produced 17 strategies over a 10 hour period. Seems strange to have such a significant difference and I have been unable to get back to producing a high volume that pass those two basic tests (even though the server I’m running on is capable of producing 350,000 strategies per hour per SQX).

If anyone else out there has any suggestions for the initial setup, feel free to share them.

Also, since Thomas was kind enough to share his results from his strategies, here are some of mine I’ve been forward testing for over a year now (some are now being traded on live accounts). The reason you don’t see any with negative balances is because as soon as it violates its historical performance benchmark/filter (such as Max DD%), I drop the strategy. For example, if it exceeds Max DD% of 30%, then it gets filtered out in my testing in SQ. So if it does it while forward testing on a demo account, I drop it as well.

https://www.myfxbook.com/members/afhampton

Joseph

4 years ago #242230

You sound like a statistician your self 🙂

Viewing 11 replies - 1 through 11 (of 11 total)