Portfolio “re-balancing”

9 replies

coensio

4 years ago #255541

I was wondering if anybody here has experimented with portfolio “re-balancing”. The idea is:

If you trade only 1 portfolio based on ‘N’ number of selected strategies you will always get some periods of DD or stagnation. Nothing wrong with that.

But if you incubate a very very large amount of strategies (= a huge collection of diversified systems) you will (most probably) always find a combination of systems that have performed well in the last period of X months.

“Assuming” the current ‘trend/market mood’ during this last X period of months, will continue, you could always trade using the best case portfolio resulting from your incubating collection of systems.

Any body wants to share any experience with this approach?

Thanks!

This is a false statement.

clonex / Ivan Hudec

4 years ago #255547

Hi,

You have to choose a way how to select strategies and periodicity of rebalancing. One way is to use momentum-based approach( rank strategies by xy, then choose some of them),.or approach based on DD of strategies., or choose strategies based on their short term correlation- All of them are in short term plans in my to-do plan. Possible next steps si rebalancing on some kind of portfolio theory, or ML algo. Ill let u know when work will be done.

clnx

coensio

4 years ago #255548

Hi Clonex,

Ok thanks for your input, I see we have similar ideas on our TODO list 😉 One addition: in theory it could be done using historical data but = huge amount of work…

Gr

This is a false statement.

clonex / Ivan Hudec

4 years ago #255570

on way is to make custom project in sqx, take strats, make for example 10 backtests of them ( eg every year) then run script filter and make a portfolio. so you can simulate a rebalancing portfolio of strategies on yearly basis.

complicated but better way is to parse strategy statistics from XML ( p/l.. etc ) ( in python with XML tree, not big problem) and make /compute whole portfolio optimizer by you own 🙂 I chose red pill – the second option:D ( edit: fir ill do the first one which is easy to implement and then ill do the second one)

hankeys

4 years ago #255590

my approach si simple, every quarter remove the old portfolio and trade new one

You want to be a profitable algotrader? We started using StrateQuant software in early 2014. For now we have a very big knowhow for building EAs for every possible types of markets. We share this knowhow, apps, tools and also all final strategies with real traders. If you want to join us, fill in the FORM.

coensio

4 years ago #255593

I think everybody here agrees that strategies need to be replaced overtime, just want to find “the best” (=most optimal) way to do this…In my opinion it would be very similar to doing WFA or maybe even WFM on portfolio level, something like clonex describes, however it requires a huge amount of work…

my approach si simple, every quarter remove the old portfolio and trade new one

Also did something similar but a ‘new portfolio’ can mean many different things e.g.:

1. Portfolio of new fresh (NOT incubated) strategies, built using latest updated historical data

2. Portfolio of new fresh AND incubated strategies built using latest updated historical data and forward tested using X weeks/months.

3. Same as 1 or 2 but only using strategies uncorrelated to previous period/previous portfolio.

4. Same as 1 or 2 but only using strategies uncorrelated to all previously used strategies/portfolios.

So in my perfect idealistic trading world I would have for example hundreds of long-term-uncorrelated strategies incubating on my account across many different markets, and every X weeks I would just rebuilt my (strongest uncorrelated) portfolio using the best performing systems/markets (over the X weeks period). If I only knew the proper X number 😉

It would be similar to totally refreshing my portfolio each X weeks, but with correlation and incubation taken into account.

The background of all of this is the observation that when you incubate a very large number of strategies on many many markets you can clearly see where the money is made and where it is totally pointless to trade at any given moment in time. And this market behavior changes over time…

This is a false statement.

coensio

4 years ago #256532

Hi traders,

So I did my homework on this topic…below the results for whom it may interest:

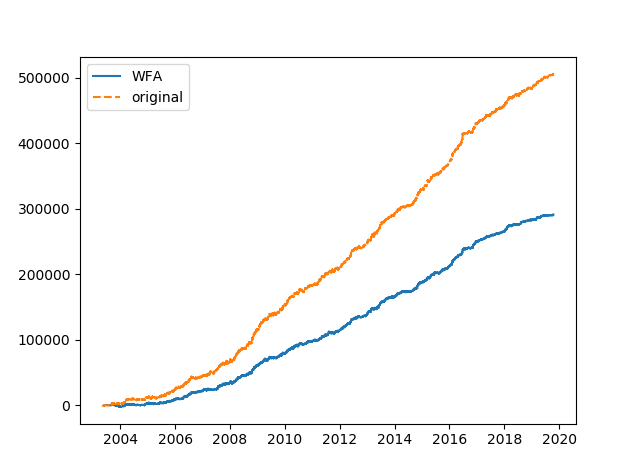

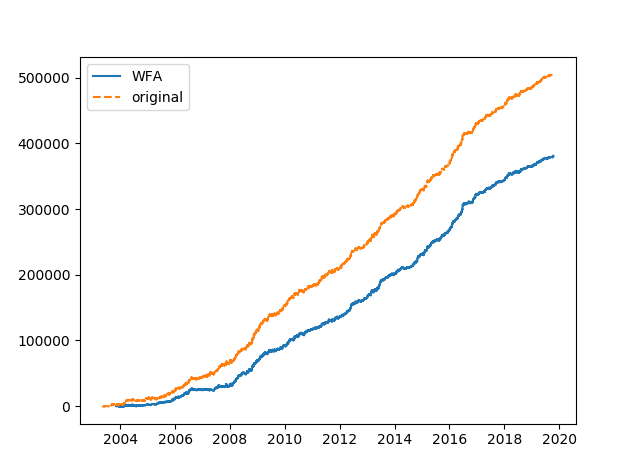

1. A portfolio of 56 diversified forex systems has been analyzed using a WFA approach (see attached Python script)

2. Each X months, portfolio results have been analyzed w.r.t. profit / per strategy and (only) the profitable systems are used in the following period of X months for trading. Etc…etc..moving window = WFA-like optimization method on portfolio level. The idea is to ‘avoid’ trading using systems that did not perform well in the last X period.

3. Below few examples of the original portfolio results v.s. WFA optimized results:

WFA window = 1 month:

WFA window = 3 months:

WFA window = 6 months:

Conclusion:

When looking on the total profit the total results could not be improved, using WFA-based strategy selection method. This is tested on forex and also other markets, like commodities and indices. I did not analyzed/compared Ret/DD figures, because I do not think anymore this is the right way to go, unless someone can prove we can improve other stats like DD. etc…

When, a portfolio is well diversified with a very low correlation between all strategies, the original (long term) result seems to be always better, than the optimized one. (=makes sense if you think about it, otherwise there would be no point of adding more strategies to portfolio). However, so far I found no evidence there is any kind of ‘trend continuity’ or ‘trend in profitability’ of systems, that could be used for periodic portfolio level re-balancing in order to ‘avoid’ trading using ‘currently’ losing systems. I see only ‘noise’, with some small winning edge that can be exploited by the law of large numbers (= trading many many diversified strategies).

I’m sharing my python script in the attachment so maybe someone else can take this idea further.

Gr

This is a false statement.

FILIPE BONALDO ACERBI

4 years ago #256158

I´m using timeseries forecast to build portfolios and got nice results.

Check here and you will see the simplest and effective way to forecast portfolios returns, the mean model.

You can use the last 20 unit of times to forecast next 5.

The steps that you have to follow are:

1- Compute a timeseries profit/loss of your portfolio. It can be whatever time basis that you want daily, weekly,monthly, quarter, annual.

2- compute historical mean of your portfolio (daily, weekly, monthly, quarter or annual mean)

3-compute standard deviation from your historical mean in the 20 most recent time series, for example, standard deviation from the historical mean of last 20 weeks.

4-Calculate T statistic to check if your historical mean is really significant in the recent data. T statistic = historical mean / standard deviation * sqrt(20)

5- Filter portfolios with T statistic > 2.1. Filtering portfolios by t statistic > 2.1 means that you have 95% confidence that the historical mean of your portfolio is significant for recent data (20 weeks, months, quarter, etc).

6- Hold your portfolio for next 5 units of time.

7- Rebuild your portfolio (step 1)

Doing that, you always will have a portfolios with higher chances to get profit in near future avoiding stagnation.

coensio

4 years ago #256545

Check here and you will see the simplest and effective way to forecast portfolios returns, the mean model.

Thanks! Very interesting theoretical read, any chances you can share some real-life examples?

This is a false statement.

FILIPE BONALDO ACERBI

4 years ago #256599

I don´t have enough trading time using this approuch to show results. But you don´t need real results to test it. Split your data in IS+OOS and check OOS. Being OOS the next 5 weeks or the time unit that you want.

Viewing 9 replies - 1 through 9 (of 9 total)