SQ Community Free Strategy Bank Project

21 replies

Ilya

7 years ago #238219

Hi guys, so following Notch’s example, since we are generating strategies all the time, how about we share some well-based strategies generated by our personal work-flows, and the community members can choose to use them, put them on a demo, comment on them, discard them, or test them further or whatever? Some more cooperation in this community won’t hurt. I personally will try to upload one strategy every 2 weeks or so, hopefully some of you can follow up with some sharing of your own as well.

So I present to you, SQ Community Free Strategy Bank!

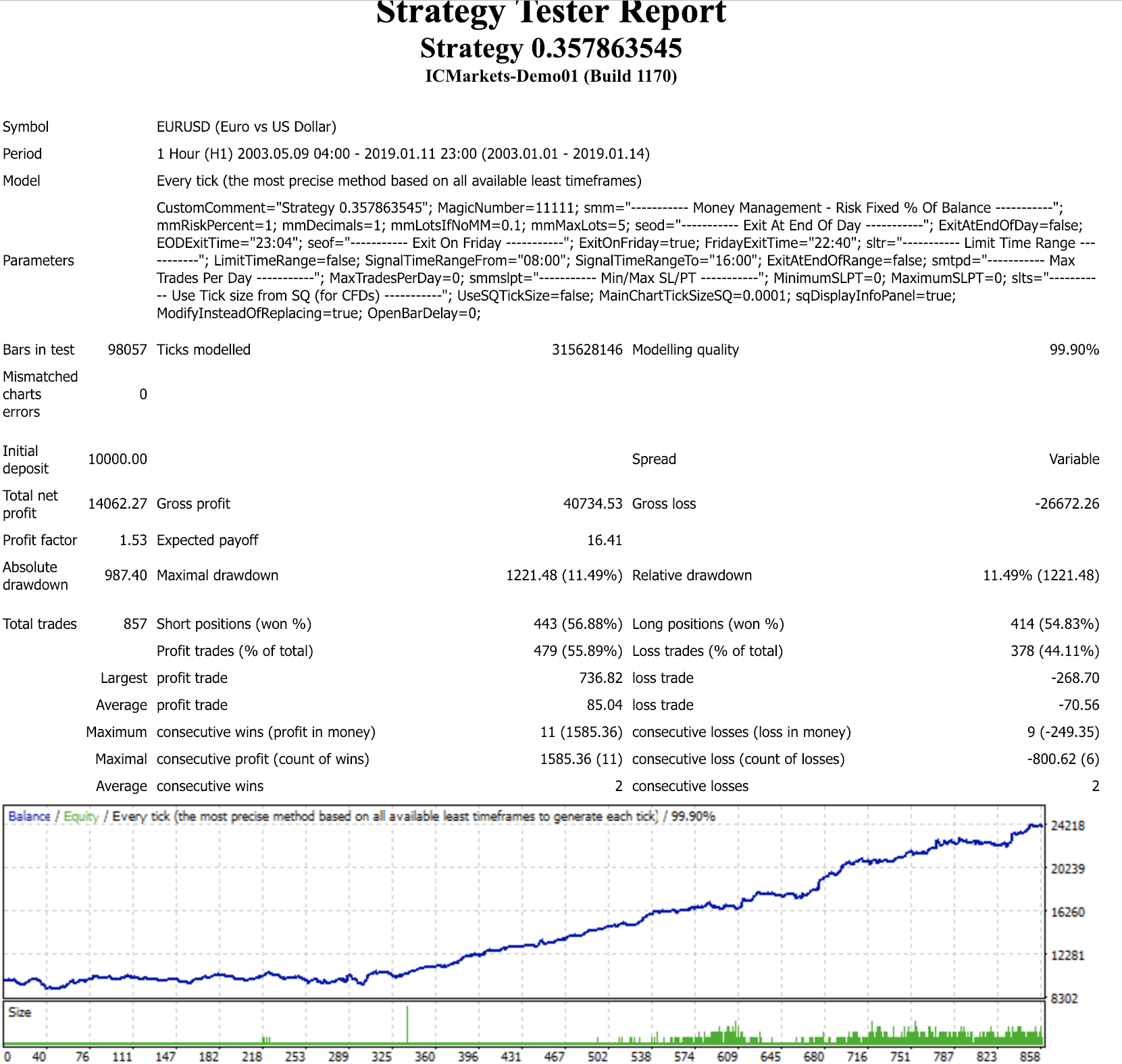

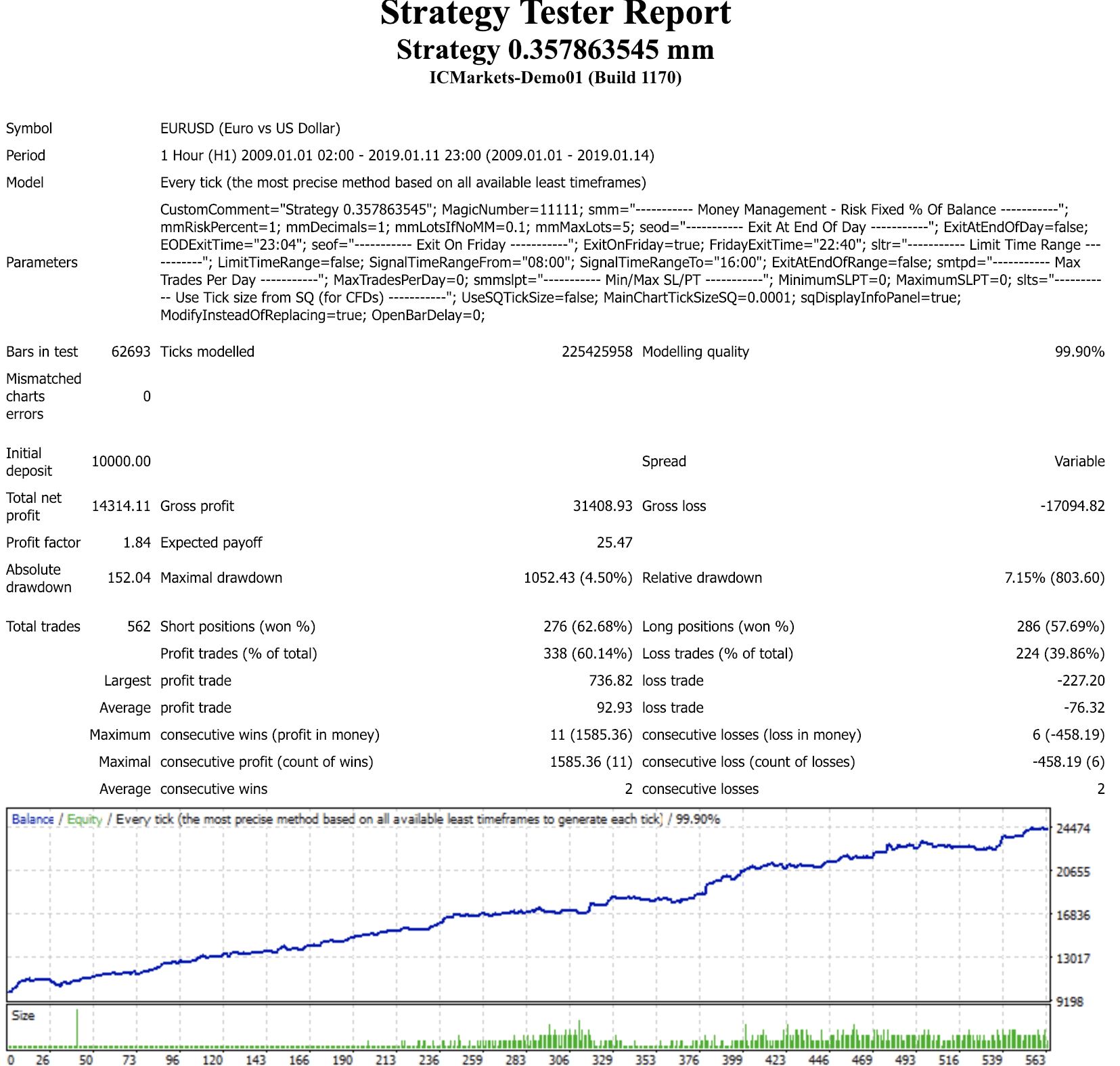

Strategy Name: 0.357863545 (quite unique ah?)

Symbol: EURUSD

Time Frame: 1H

How was the strategy generated?

The strategy was initially generated on 2 years of data using random generation on selected timeframe only, half a year of which was OOS.

How was it tested further?

– It was retested on 15 years of Dukascopy tick data as OOS, to make sure it works through history.

Did I optimize it?

Nope, if I like the strategy enough, I usually don’t optimize it, sometimes I give it a minor bump.

How did I check robustness and try to avoid overfitting?

– The fact genetic evo wasn’t used & the strategy was generated as is randomly using 2 years data, and turns out to work well on the entire data set, makes me more confident that I didn’t overfit it.

– 500 MC (each) runs of: Randomize trades order, skip trades, randomize min distance from price from 0-10, randomize slippage 0-5, randomize spread 1-5, randomize starting bar max change 100.

The above filtered by RETDD at 95% > 40% of original RETDD, and looking at the correspondence of the curves, making sure they remain on the same course and not far detached one from another, and the 2 SQX default filters (Net profit at 80% > 50% of original net profit and Max DD% at 80% smaller than 200% of original DD%)

– 500 runs of Randomize History Data with probability 20% and max price change 20% of ATR. Same filters as above.

– 100 runs of Randomize strategy parameters, with probability 20% and max change 50% (Tough one, credit to Notch for this one). Looking for RETDD at 100% to be > 1.

What do I like about the strategy?

– Working well for 15 years, Booming for 10 years.

– Minimal stagnation and drawdown, 11% for 15 years and only 4.5% for the last 10 years. Good for my nerves.

– Around 56% wins for 15 years and 60%+ for the last 10.

– Not too complicated and sound trading logic. When bears power is falling for 3 hours and price opens below the lower Bollinger band -> go long, and vice versa for short.

What I don’t like about the strategy?

– Relatively low amount of trades. 857 in 15 years, making it 4-5 trades a month, I usually like strategies that trade more frequently.

mt4 real tick 15 years equity curve & report:

mt4 real tick 10 years equity curve & report:

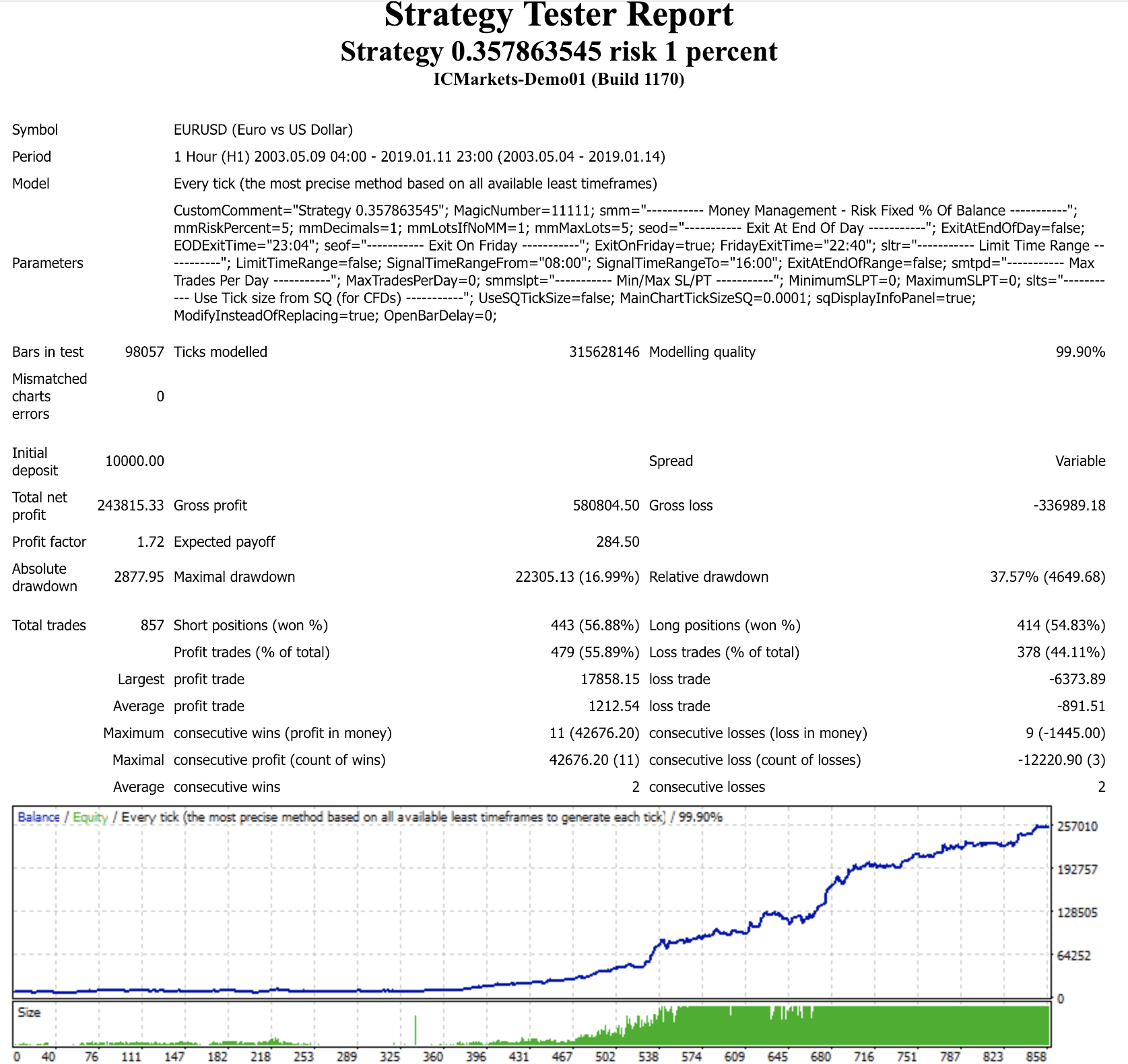

15 years 5% risk, for fun. Don’t use it.

Note: Attached files are using 1% risk of account and 0.1 lot if there’s no MM. Plus, the strategy closes trades on Friday 22:40 GMT+2 DST US, and that’s how the above mt4 tests were generated, adapt to yours if need be.

Let me know what you think, and obviously don’t use it without doing your own testing and fitting it to your trading style. I’ve put it on my live incubation account (Started with 500$ with 1% risk).

Have a good weekend all and wish you a profitable 2019.

Ilya

Ilya

7 years ago #238221

Enric

7 years ago #238235

Hi Ilya. I’ve taken a look to your strat and fails on my personal workflow. Although Ret/DD is good, it doesn’t passes the Multitimeframe test.

I think your initiative is good. I’d publish an example of my own strategies but these are still beeing generated by SQ3, I don’t dare to go real with SQX until it was less bugged. If you think SQ3 strat could be attached I’ll come with one of my own 🙂

Ilya

7 years ago #238236

Hi Ilya. I’ve taken a look to your strat and fails on my personal workflow. Although Ret/DD is good, it doesn’t passes the Multitimeframe test. I think your initiative is good. I’d publish an example of my own strategies but these are still beeing generated by SQ3, I don’t dare to go real with SQX until it was less bugged. If you think SQ3 strat could be attached I’ll come with one of my own 🙂

Hi Enric, yeah I never test multi timeframe or multi symbol, those tests make no sense to me and so far it has been going fine without them 🙂 OK I hope you can also drop a strategy of your own, that would be nice. I’ll try to keep an update here whether my strategy is profitable or fails during live trading.

Cheers

Ilya

Enric

7 years ago #238237

Good. In this case here you have one with all tests passed (my workflow) and working with real money! I challenge you to compare live results 😉

BTW Ilia. Be careful because there’s a bug in SQX with the simetry of the logic on your strategy. Looks like Bears and Bull indicator are not really simetric, should be fixed in B118

Enric

7 years ago #238238

Try again uploading the file

hankeys

7 years ago #238240

my 2 cents:

– always use data for UTC you will be trading. Using UTC0 dukas data if you will be trading with broker on UTC2 will lead to big diff. Close Friday will make another diff.

– close friday too late (22:40) – there are already widened spreads

– always use MM in BT which you will be trading – if ATR SL is in strategy it could lead to another diff. Using %risk or risk in money need bigger capital. Using %risk is the worse MM i think, because the open positions will raise in the time where the strategy will be profiting. But after profits come loosers and you will be trading biggest positions

You want to be a profitable algotrader? We started using StrateQuant software in early 2014. For now we have a very big knowhow for building EAs for every possible types of markets. We share this knowhow, apps, tools and also all final strategies with real traders. If you want to join us, fill in the FORM.

coensio

7 years ago #238257

– always use MM in BT which you will be trading – if ATR SL is in strategy it could lead to another diff. Using %risk or risk in money need bigger capital. Using %risk is the worse MM i think, because the open positions will raise in the time where the strategy will be profiting. But after profits come loosers and you will be trading biggest positions

I think the best practice is to use MM with fixed amount per trade, you can easily scale up, but most importantly you can compare all different strategies with each other.

This is a false statement.

Oliver

7 years ago #238259

Following from Ilya & Enric i have workflowed through to real test account.

please let me know what you think. good or bad

Gianni

7 years ago #238241

Ilya

7 years ago #238321

Hey Notch, thanks for the input.

So you guys are kind of bursting my bubble here. I was trading with fixed risk of account for the last 3 years (2 of them manual). You guys use a fixed amount on each of your strategies? Can you elaborate on the logic?

Ilya

coensio

7 years ago #238323

So you guys are kind of bursting my bubble here.

Bubbles never last forever 😉

1. Ok, I will exaggerate by factor x10 to make this particular example clear.

Let’s say you lost 20% on one trade on your $1000 account, how much % you need to win on the next trade to break-even? You can do some math now 😉

2. Moreover evaluating systems using %risk is pretty messy because the equity curves follow exponential growth instead of linear one,

I am personally interested in a stable equity growth instead of final amount of $. I have learned from some smart people to always chose stability over money.

3. And finally, I would not feel confident in opening orders with larger LotSizes, not even with a large equity (and sufficient freemargin).

That are just my thoughts on that topic..

Gr

Chris

This is a false statement.

kainc301

7 years ago #238373

I think there is a better solution for what you are trying to accomplish. Many people don’t like to share what they find (at least not their best work). In order for everyone to really benefit from a community strategy bank, we’d all have to share our best strategies while still keeping them private. Oxymoron right?

Well no actually. Instead of a database where everyone has access to everyone else’s strategies, we can store all user submitted strategies on a server and include a Neural Network in SQ that learns from this large dataset in order to create better strategies for you. This way, everyone will be incentivized to submit their best work because it will help build something that would help them create better strategies. In other words, we all win without our strategies becoming public and we can all make better material the more data that we submit. Each SQ update would include the AI that trained on the newly updated dataset, allowing all of us to make better and better strategies as time moves along.

I created a feature request for this here https://roadmap.strategyquant.com/tasks/sq4_4042

I know this would take a long time to build. Not expecting any new features soon but I think it would solve what you are trying to accomplish and help everyone on a larger scale than having people contribute a lot of strategies that probably won’t be the best they can be.

Ilya

7 years ago #238375

But to address the original topic: the money management approach is going to be driven by what one hopes to achieve with a particular portfolio; there’s certainly no “one glove fits all” where money management is concerned; I use fix money amount when scalping, I use ATR SL/PT and fixed % risk with large multi-symbol portfolios, I use balance per lot with grids and fixed % risk of account balance with fixed % risk of the square root of cumulative profits for others. This is driven by the trader’s risk preference and can’t be prescribed to experienced traders without a knowledge of the trader’s risk/return indifference curves; doing so would simply be nonsense akin to recommending a 50 indicator manual trading system to a color blind information overload sufferer.

Thanks for clarifying, I understand and agree with that, I have been trading with similar logic.

Ilya

7 years ago #238376

Bubbles never last forever 😉 1. Ok, I will exaggerate by factor x10 to make this particular example clear. Let’s say you lost 20% on one trade on your $1000 account, how much % you need to win on the next trade to break-even? You can do some math now 😉 2. Moreover evaluating systems using %risk is pretty messy because the equity curves follow exponential growth instead of linear one, I am personally interested in a stable equity growth instead of final amount of $. I have learned from some smart people to always chose stability over money. 3. And finally, I would not feel confident in opening orders with larger LotSizes, not even with a large equity (and sufficient freemargin). That are just my thoughts on that topic.. Gr Chris

Hey.

So first of all, evaluating systems indeed cannot be done using %risk. I always use fixed size, to make it proportional and analysis-relevant. My point of interest was regarding live trading.

Regarding your % example, that still doesn’t make sense to me, and will be true only for a system that loses more than it wins, both by % of trades and amount of pips/usd per trade. For example one of my long-used USDJPY systems, has a 60% win ratio, it wins on average 32 pips, and loses on average 21 pips. I have a very stable growth of the account (looking on that strategy alone) based on %risk per trade (risk half a percent), and backtesting it with fixed size (say 0.1 to win/lose a dolar/pip), yields to a less favourable outcome, without significant change of stability. I guess it’s also just a matter of preference.

coensio

7 years ago #238378