SQ Community Free Strategy Bank Project

21 replies

Ilya

7 years ago #238219

Hi guys, so following Notch’s example, since we are generating strategies all the time, how about we share some well-based strategies generated by our personal work-flows, and the community members can choose to use them, put them on a demo, comment on them, discard them, or test them further or whatever? Some more cooperation in this community won’t hurt. I personally will try to upload one strategy every 2 weeks or so, hopefully some of you can follow up with some sharing of your own as well.

So I present to you, SQ Community Free Strategy Bank!

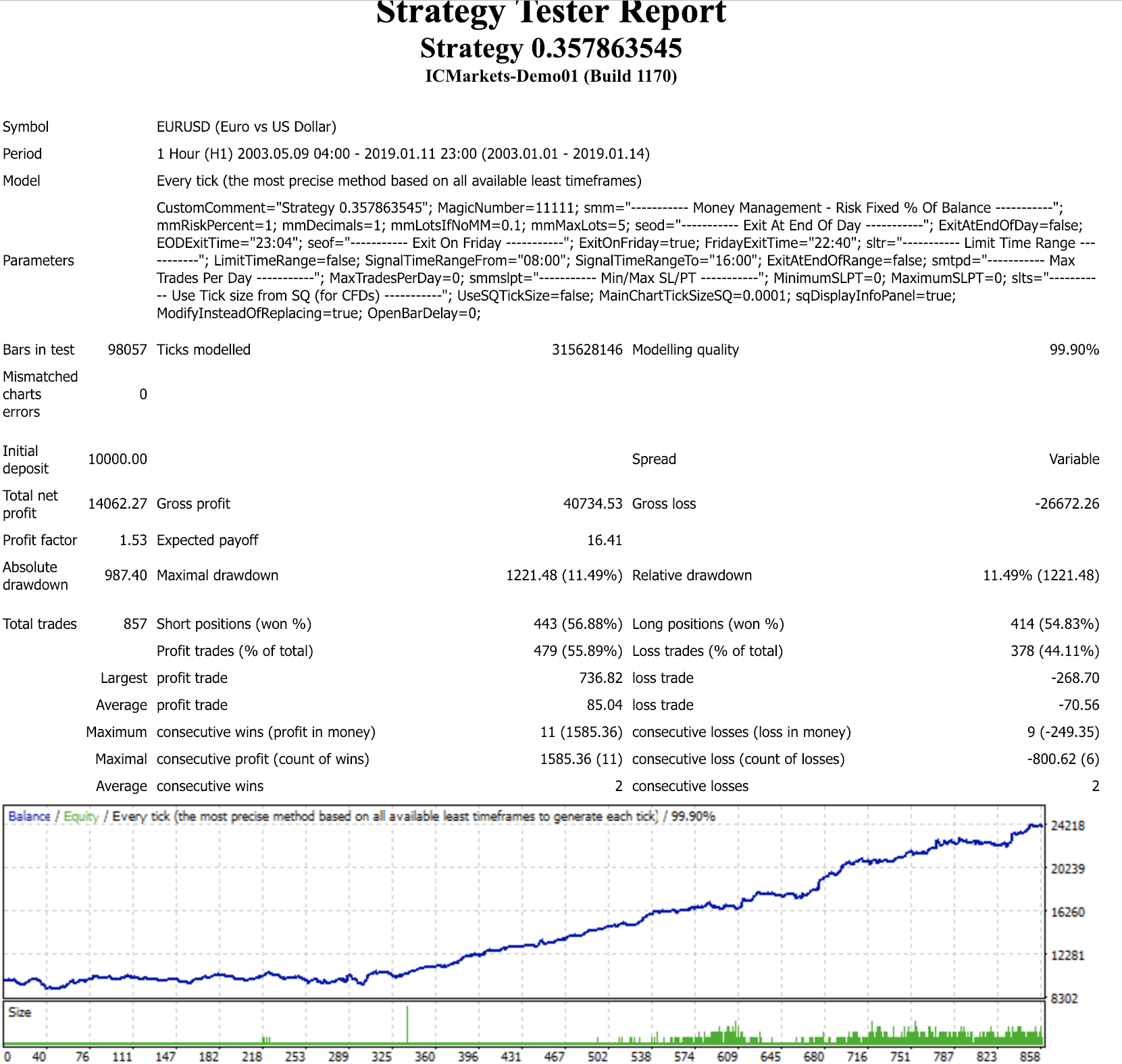

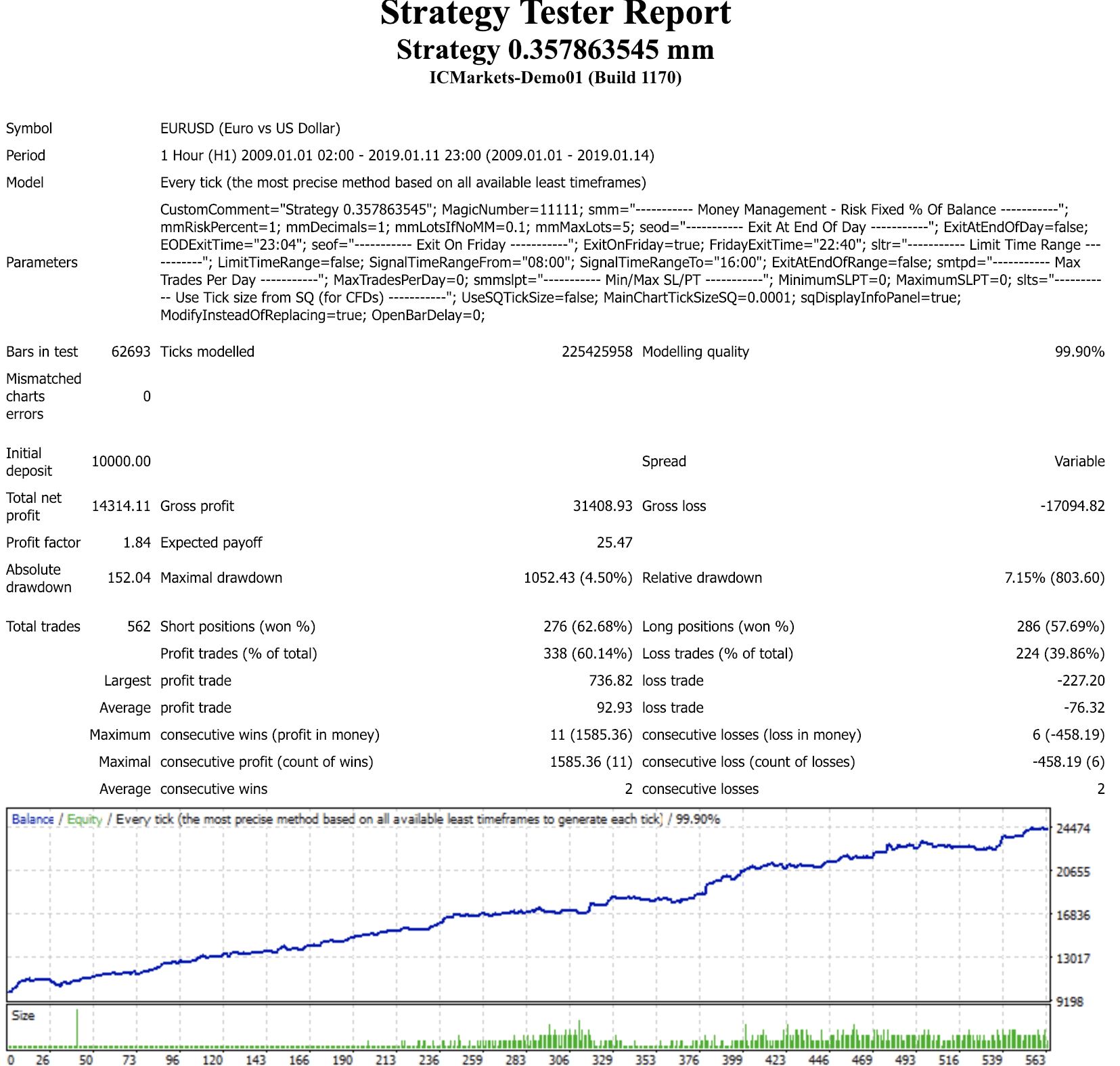

Strategy Name: 0.357863545 (quite unique ah?)

Symbol: EURUSD

Time Frame: 1H

How was the strategy generated?

The strategy was initially generated on 2 years of data using random generation on selected timeframe only, half a year of which was OOS.

How was it tested further?

– It was retested on 15 years of Dukascopy tick data as OOS, to make sure it works through history.

Did I optimize it?

Nope, if I like the strategy enough, I usually don’t optimize it, sometimes I give it a minor bump.

How did I check robustness and try to avoid overfitting?

– The fact genetic evo wasn’t used & the strategy was generated as is randomly using 2 years data, and turns out to work well on the entire data set, makes me more confident that I didn’t overfit it.

– 500 MC (each) runs of: Randomize trades order, skip trades, randomize min distance from price from 0-10, randomize slippage 0-5, randomize spread 1-5, randomize starting bar max change 100.

The above filtered by RETDD at 95% > 40% of original RETDD, and looking at the correspondence of the curves, making sure they remain on the same course and not far detached one from another, and the 2 SQX default filters (Net profit at 80% > 50% of original net profit and Max DD% at 80% smaller than 200% of original DD%)

– 500 runs of Randomize History Data with probability 20% and max price change 20% of ATR. Same filters as above.

– 100 runs of Randomize strategy parameters, with probability 20% and max change 50% (Tough one, credit to Notch for this one). Looking for RETDD at 100% to be > 1.

What do I like about the strategy?

– Working well for 15 years, Booming for 10 years.

– Minimal stagnation and drawdown, 11% for 15 years and only 4.5% for the last 10 years. Good for my nerves.

– Around 56% wins for 15 years and 60%+ for the last 10.

– Not too complicated and sound trading logic. When bears power is falling for 3 hours and price opens below the lower Bollinger band -> go long, and vice versa for short.

What I don’t like about the strategy?

– Relatively low amount of trades. 857 in 15 years, making it 4-5 trades a month, I usually like strategies that trade more frequently.

mt4 real tick 15 years equity curve & report:

mt4 real tick 10 years equity curve & report:

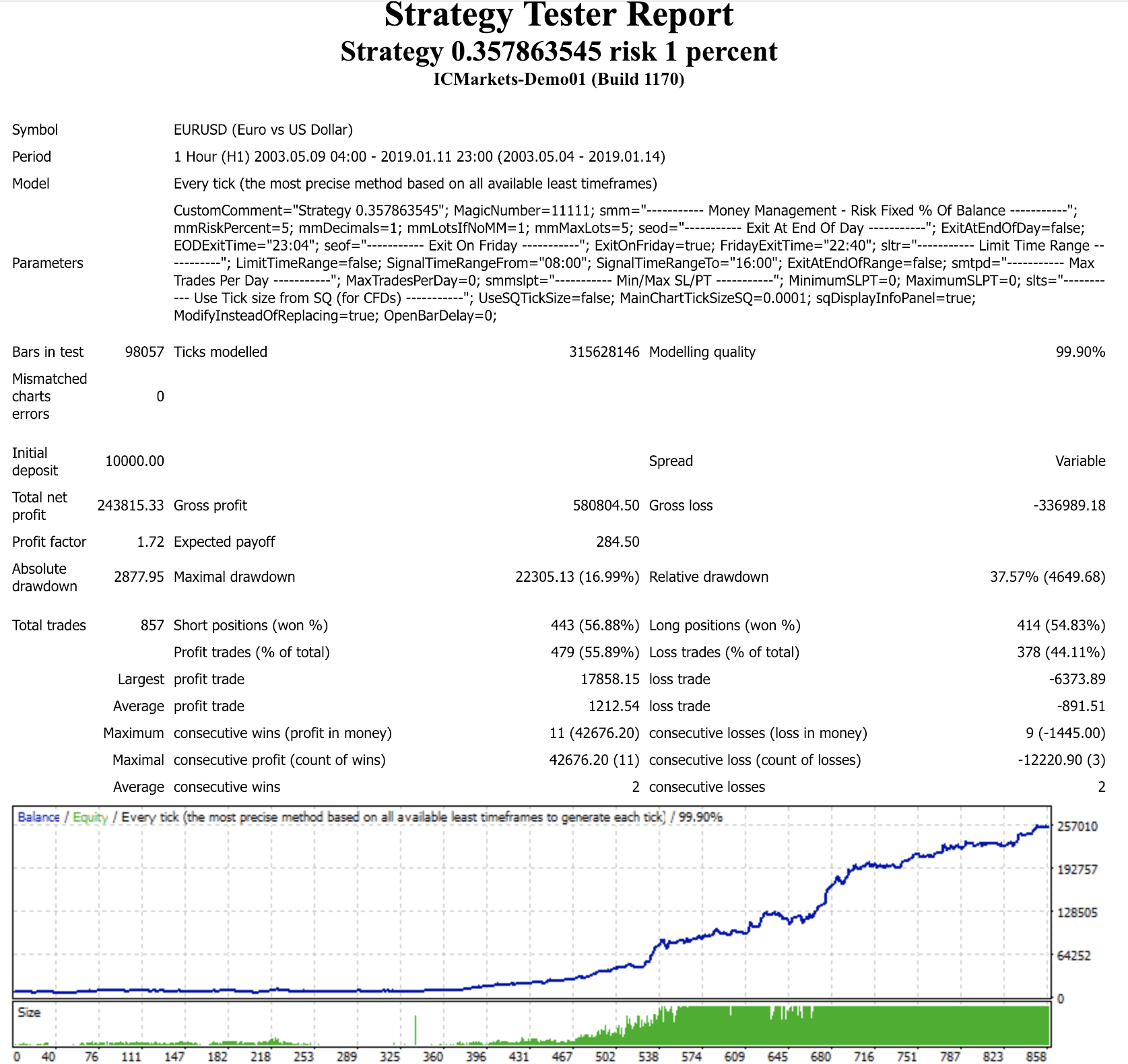

15 years 5% risk, for fun. Don’t use it.

Note: Attached files are using 1% risk of account and 0.1 lot if there’s no MM. Plus, the strategy closes trades on Friday 22:40 GMT+2 DST US, and that’s how the above mt4 tests were generated, adapt to yours if need be.

Let me know what you think, and obviously don’t use it without doing your own testing and fitting it to your trading style. I’ve put it on my live incubation account (Started with 500$ with 1% risk).

Have a good weekend all and wish you a profitable 2019.

Ilya

Enric

7 years ago #238385

Oliver

7 years ago #238386

Ok thanks. your mc test is that on mt4 back test?

I have an issue with strategies im generating in sq3. im wondering if you could help me shine the light on the problem? my sq generates some amazing strategies which when backtested in mt4 they just blow the account. this happens on lots of currency pairs like gbpnzd, gbpaud, euraud, eurnzd, usdjpy, audjpy, nzdjpy , eurjpy etc. any advice would be helpful? i also note this has only started to happen since i upgraded my computer.

thanks

Enric

7 years ago #238387

Hey, no the MC test are the Inbox SQ3. I stick on MC tests although not everyone shares my confidence in MC: https://medium.com/@mikeharrisNY/fooled-by-monte-carlo-simulation-eee0b312e489

Some differences between SQ3 and MT4 backtests are ‘normal’. Just make sure that you are testing with same data, same parameters on both sides and both equities should be similar.

Also, MT4 is a bit triccky on the backtest. For some reason if you’re Online it reload the historical data and breaks the backtest. My advice to you would be to Offline your PC, empty the MT4 historical data, reload the data (same data you have in SQ3) and do the MT4 backtest. Should work

Phillip van Coller

7 years ago #238763

Thanks for sharing Ilya.

I like the way you came up with this strategy.

Our of curiosity how long did it take you to generate this strategy?

Ilya

7 years ago #238845

Hey guys, sorry for the absence, have a lot of work these days 🙂

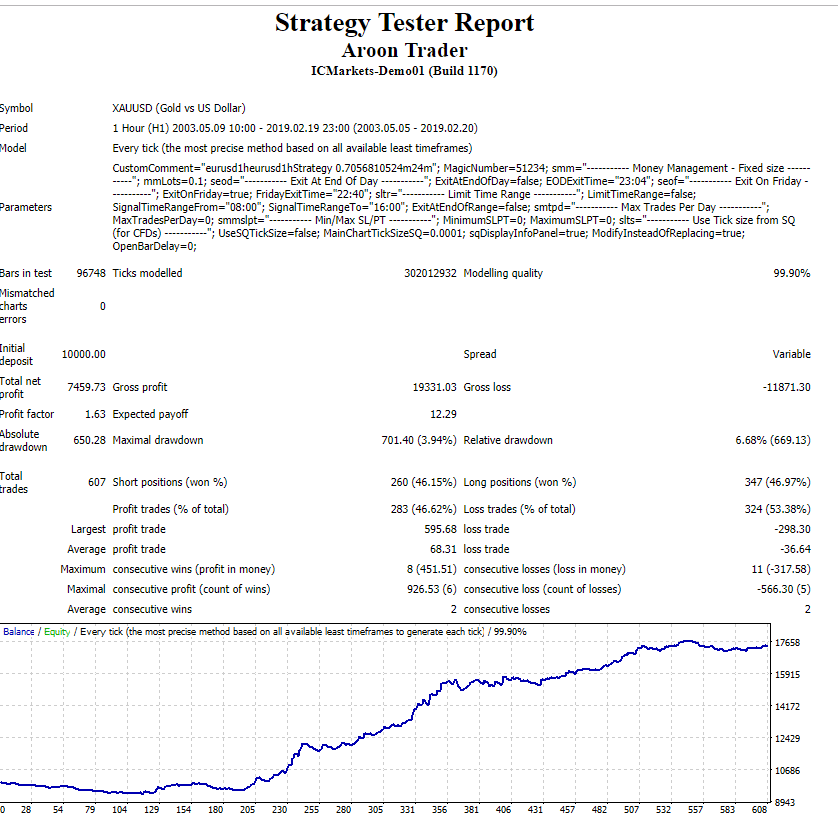

I’m attaching another one of my strategies, running for a month on a live account with profitable results on 3 symbols.

Generation & Testing same as in the original message, including all MC tests.

+ I chose this one since it can nicely also trade multiple markets such as XAUUSD, EURUSD, USDJPY.

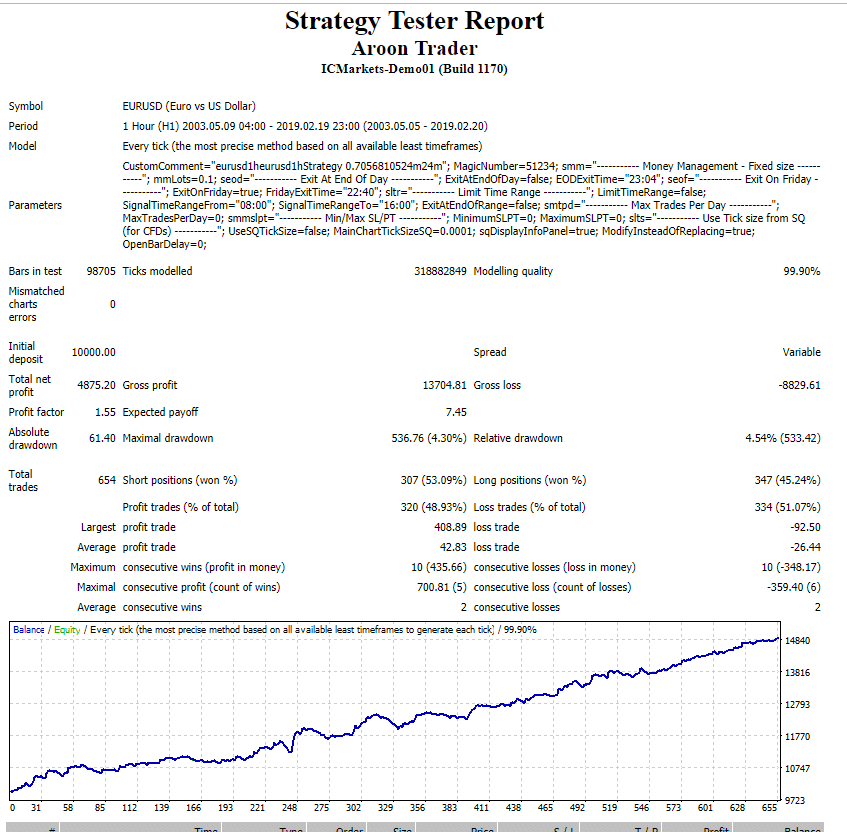

Here are 15 years BT real tick XAUUSD:

Here’s EURUSD:

Enjoy.

Ilya

Ilya

7 years ago #238846

Thanks for sharing Ilya. I like the way you came up with this strategy. Our of curiosity how long did it take you to generate this strategy?

Hey Phillip. My normal work flow is generating Sunday -> Friday, and then handle MC, Optimization, etc on Friday & Saturday, hopefully get 1 or 2 good ones that I can put on a small live account, and generate again. Trying to diverse symbols and generation conditions to make it interesting and diverse. So for me, whether the strategy appears in the DB after 1 hour or 6 days, it’ll take at least around 1 week to get any strategy out of the process, given I’m not overloaded with work, as I am nowdays for example 🙂

Cheers,

Ilya