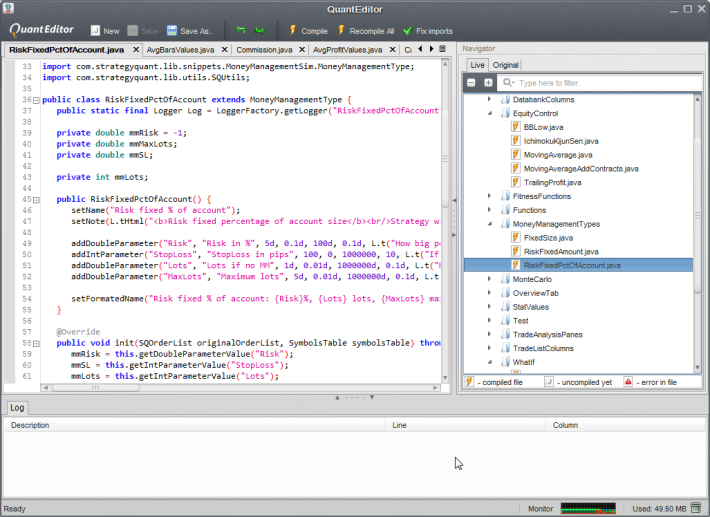

Extendability

You can easily create your own parameters, statistical values, etc. For example, you can implement new money management models or Monte Carlo simulations.

The extensibility also gives you access to the source code of all currently running methods and calculations via built-in QuantEditor, which allows you to see how they work and adjust them if you need to do so.

Learn more in our documentation: Getting started extending the platform

Several examples of extensibility of the software using snippets>

Addition of statistical values

You can add new statistical values and show them in the database or strategy overview. Example

Addition of new what-if scenarios

Such as removing all trades that happen every third Friday in a month. Example of What-If extension

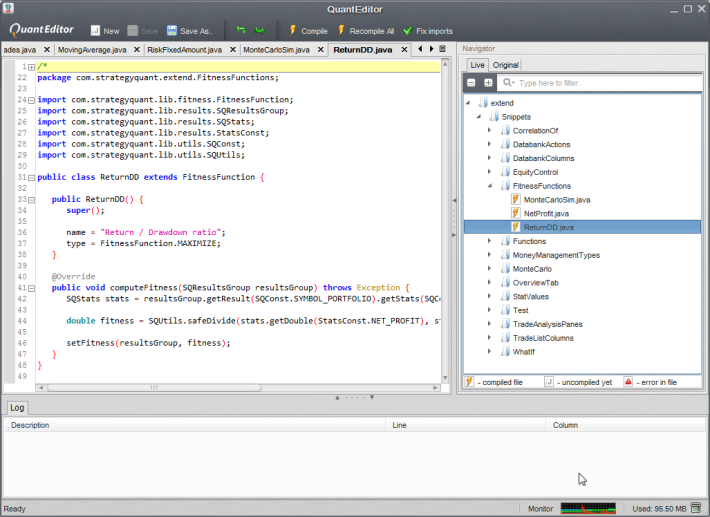

Addition of new Monte Carlo simulations

You can create and add a new Monte Carlo simulation. Example adding new Monte Carlo column