Quant Blog

General articles about trading, not necessarily related only to StrategyQuant.

Subscribe and get our weekly newsletter in you inbox.

Přejít k obsahu | Přejít k hlavnímu menu | Přejít k vyhledávání

General articles about trading, not necessarily related only to StrategyQuant.

Subscribe and get our weekly newsletter in you inbox.

When evaluating the success of a trading strategy, a strategy developer can use a large number of strategy metrics. One of them is the profit factor. Profit Factor may be …

22. 11. 2022

In today’s episode, we build on the findings from the previous parts, in which we tried to identify and measure the factors that can affect the true out-of-sample performance of …

15. 3. 2022

A common problem for a trader is to know when his strategy has lost the advantage, or in short, when there is such a situation that does not fit today’s …

28. 2. 2022

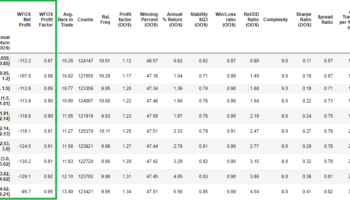

Part 3:Profit Factor, Ret/DD Ratio/ Stability SQ3/ Annual % Return,Winning Percent, Win/LossRatio/ Sharpe Ratio

27. 11. 2021

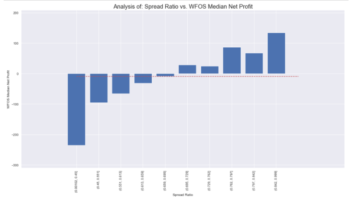

In today's episode, we look at whether using a spread ratio can lead to a better true-out-of-sample (WFOS ) result.

24. 10. 2021

Part 1: Complexity and Number of Trades About a year and a half ago, I came to the conclusion that the edge of my strategy development workflow was shrinking. . …

11. 10. 2021