100% automated and 100% accurate SQ workflow test case

71 replies

coensio

7 years ago #238903

My first 100% automated and 100% accurate workflow, StrategyQuant ‘custom projects’ test case

DISCLAIMER: The presented results below are still preliminary, there is still a small chance that my positive results are influenced by an undiscovered bug in the current version of SQ-X (build 118.84) or that I’ve just made a stupid mistake somewhere in my workflow resulting in a huge ‘Data Mining Bias’. However I did my best and rechecked everything multiple times…Moreover since this all is based on a relatively new ‘custom projects’ feature of SQ-X, nothing of this has been tested yet on a real account…but I think I have built a strong case supporting I could be right on this one

My claim: It looks like I’ve managed to create a 100% automated and 100% accurate workflow using StrategyQuant feature called ‘custom projects’.

100% automated means: I push 1 button before going to bed, and every morning my workflow automatically generates, validates and selects few new strategies which are ‘ready to go’

‘Ready to go’ means: I can deploy them immediately to my live account. Without a need of further processing.

100% accurate means: Every single strategy that has been selected by this automatic workflow (~50 so far), has been profitable in the 2 years period from the generation date.

To test my workflow I’ve adapted my SFT method as described in this topic: See HERE.

The workflow is based on standard validation test (common knowledge) as shared by SQ team in their free courses, however with a very rigorous settings. The workflow does not use any advanced validation methods like WFA,WFM,OP,SPP. Instead a customized Monte-Carlo test is used to simulate behavior of a SPR method. No portfolio analysis is performed (some systems can be correlated!).

My automatic workflow test case is split into two verification periods:

1. End of year 2014.

2. End of year 2016.

At each point in time 1 and 2, I used my workflow to automatically generate and automatically select 20 NEW strategies (out of several hundreds thousands systems) without ANY manual intervention and then ALL of selected systems where forward tested using SFT (future data). Let me be clear on one thing: I did not cherry picked any strategies.

It seams that every single selected strategy was profitable in the period following the selected generation date. See figures blow:

Test case 1: Strategy creation @ 2014.12.31, Simulated Forward test: 2015.01.01…2016.12.31.

Real-Ticks (Dukascopy data), Real-spread (no commissions)

Test case 2: Strategy creation @ 2016.12.31, Simulated Forward test: 2017.01.01…2018.12.31.

Real-Ticks (Dukascopy data), Real-spread (no commissions)

My conclusions so far:

1. If there are no mistakes, then it seems that it is totally possible to use SQ-X automated ‘custom projects’ to automatically generate and select profitable trading systems.

2. No advanced validation/filtering methods needed. Of course these tests should only improve total result and minimize DD on portfolio level.

3. The results in SFT of >2014 are slightly better than >2016. Workflow is somehow sensitive to used data during strategy generation (due to changing market condition). It seems that years 2017 and 2018 are very difficult years for trading using the selected trading type.

4. It is not 100% proven yet, but it’s a pretty damn good result so far, taking into account it’s based on a simple workflow that is using basic filtering principles.

5. Some of the strategies can be correlated, but for the sake of this investigation no manual correlation filtering has been performed. This would jeopardize the objectivity of this test case.

6. The filtering settings are very rigorous, this workflow filters out only the most robust strategies. According to my statistics only 0.05% of the generated strategies are able to pass this workflow.

TODO:

– Refine the workflow and implement further strategy selection, perform correlation tests, WFM analysis and additional portfolio level related tests.

– I’m also waiting for 01.03.2019 and build 119 with new features 😉

Greets,

Chris

This is a false statement.

0

hankeys

6 years ago #257807

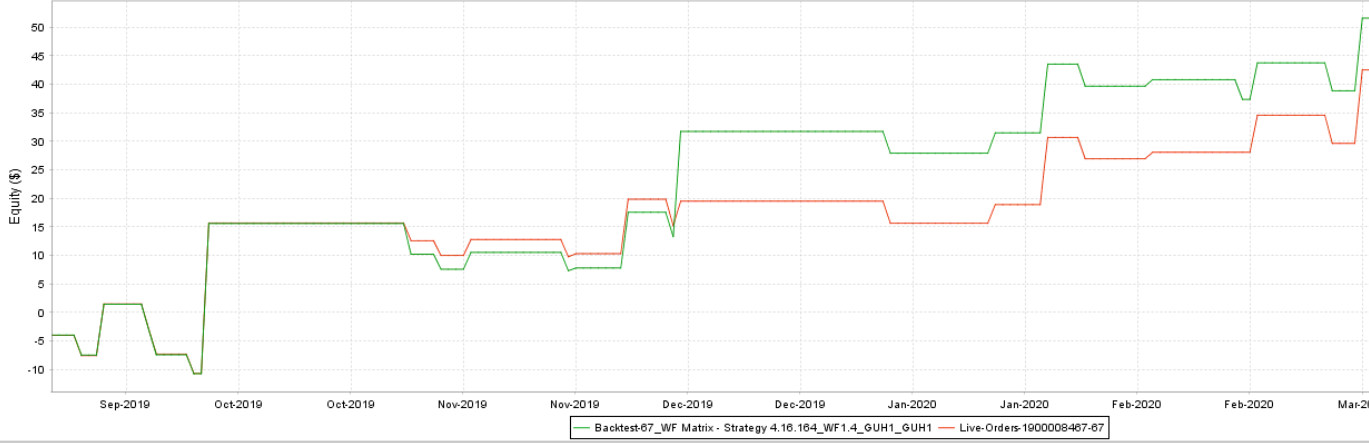

differences will be everytime and everywhere – backtest is only a backtest with fixed spread and fixed slippage and on dukascopy data – every datafeed could be different, mostly at the evening when spread widening occurs

but 60 trades is nothing in 1000 trades total – what counts is the USD comparation and this as you can see was different too in 2019/10, real account hit zero line, but backtest was in the profit (and not small) but after some time the real account is going very well as a backtest

truth is – assumption that your backtest will be always the same as real account is nonsense – we can never simulate real live performance – till B126 the SQX backtest has issue with gap filling (so the backtest is more like a demo) – its fixed most probably only in B127

some brokers have also no trading times (5 minutes every day) or some of them using no trading hours in the evening, etc. etc. everything counts

basic is the direction of EQ curves and try to be hard to your backtest – use slippage, use wider spread, not use tick data with ECN spreads (lower values) and try to get on real account at least 70% of backtest performance

You want to be a profitable algotrader? We started using StrateQuant software in early 2014. For now we have a very big knowhow for building EAs for every possible types of markets. We share this knowhow, apps, tools and also all final strategies with real traders. If you want to join us, fill in the FORM.

0

coensio

6 years ago #257810

Thanks for your good feedback hankeys…I know about all issues including the gap filling one (I even think it was my own bug ticket), but i do not think this all is addressing my point I’m trying to make..so summarizing:

What I see that some of my strategies are “more or less” correlate to my live trading and some are totally not..using THE SAME SETTINGS.

So if I “think” I finally have found a good SQX set of settings for reliable strategy generation, because one of multiple of generated strategies correlate (acceptably) with my LIVE trading, I would like to use those SQX settings to build more strategies and sleep well…while live trading.

BUT, this is impossible since if I build and test more strategies there will be ALWAYS strategies that do not correlate, even when generated with the previously found “good SQX settings”.

So the only way I see is to incubate and select only those strategies that do follow the “expected” SQX behaviour, and trade only those BUT this takes many months of testing and as we know some of strategies will expire after X months.

I hope this makes sense….

This is a false statement.

0

hankeys

6 years ago #257814

real account is real account, demo is demo and backtest is backtest – we cant simulate everything

the picture above from me is averaged portfolio of 50 strategies…and every strategy could behave differently throught times

you can have better strategies than backtest…and on the other side the real behavior of strategy could be worst….task for the user is simple – make backtest not so precise…because backtest will never be picture of real behavior of strategy in the past on real account and future will be everytime different, because in real account we are getting many variables which cant we control

You want to be a profitable algotrader? We started using StrateQuant software in early 2014. For now we have a very big knowhow for building EAs for every possible types of markets. We share this knowhow, apps, tools and also all final strategies with real traders. If you want to join us, fill in the FORM.

0

eastpeace

6 years ago #257860

Hello, coensio,

What’s your custom filters setting in Ranking?

Is it same in 30 minute TF and 1H TF?

And in the OSS and in the last future part, is it same?

0

alanhere

6 years ago #258561

Very interesting guys.. I’ve been working with this product for a couple of years and finding that the execution is different on different brokers. Just having the same algos in a portfolio across two different brokers can yield quite different results.

Besides the obvious differences between brokers.. ie spreads, types of accounts, commissions.. I’ve selected different brokers with similar attributes (spreads, ECN or STP etc)

The algos I’ve been building are ones with stops and profit targets >20 pips.. so, I’m not targeting small pip amounts… so less dependency on spreads. I’ve put no time dependency on any of the algos and brokers times are the same.

However, I’m finding that the execution can be quite different and I am not 100% sure it is always the broker. The reason why I say this is that I’m also other algos from 3rd parties and some execution at exactly the same times with similar pricing. However, my algos created by SQX are the ones where the executions can be off by quite a bit.

Looking at the MQL4 code that is generated, there is a lot of stuff in them… I was thinking of trying to take out the execution entries and exits of the code into a ‘clean template’ and seeing if it makes a difference but am not skillful enough to do this…

Just wanted to share some thoughts and if anyone has found this too

0

mabi

6 years ago #258578

Alan if the order is an stop or limit order it is placed at the broker and would execute even if the MT4 is offline which could be a couple of days from now. Now to further confuse you i can have same strategies on same broker having diffrent results but you cant look at one trade after a year they will have very simular result.

0

Joseph

5 years ago #268198

It sounds like we might spend a year and a half developing and incubating only for the strategy to expire in a few months… I came here looking for motivation to get back on the horse… Oh boy!

0

coensio

4 years ago #275555

Another year comes to an end…it’s time for our yearly honest update, so below you will find my conclusions and tips after few years of live trading SQX systems:

1. In algo-trading 1 year is not statistically significant 😉

2. So after years of try and error, this is one of my best long term algo-trading results: as example see figure below, last 2 years of trading on my live account on TradeStation. Now you can see more or less what you can expect…and I am pretty sure there are many traders here with much better results!

3. For those who are saying that SQX doesn’t work: SQX works. Period. SQX strategies can make money. Period. Once you know what to do, it is not that hard to find a strategies that really make money. Period.

4. Finding long term strategies is pretty hard, but it is really possible to find them. Previously I could find only short term strategies, that stopped working after few months of trading. Now I see years of constant profitability. Once a year I run WFA to re-optimize systems.

5. Forget about forex, try something else like futures!

6. Find a good borker: avoid “cheap” MT4/MT5 brokers.

7. Stick to your own plan and try to do the opposite of what everyone is telling you 😉 Remember that only 2% of traders make money.

8. The one most important thing I can share with you is:

!!! Before you will start developing and tweaking your workflows, first make sure you see a good correlation between your live trades and what you see when you backtest your strategy in SQX!!!

This is the key to success, at least in my opinion, this single improvement allowed me to develop my workflows and in the end to find profitable strategies.

Initial capital: $2000

Profit = +$4000, (+200%)

Return retracement ratio: 14.74.

Greets,

See you next year 😉

Chris

This is a false statement.

0

ivan

4 years ago #275556

this is a very good post to say the least, if not one of the best i have read in a while here. Beginners should read and note because rarely you see so much good info crammed in a so short post.

regarding the forex exclusivity, i have seen the recent post of thomas262 where he recommends the same approach, to diversify. I would add only the observation that in a lesser extent, the cause for this (beginners focus too much on forex only and draw incorrect conclusion) is the fact that the marketing of SQ, every demo and presentation of SQ advertises that is a forex focused software

regarding the profitability, again, this is one of the most important information sought after, how much money one can make and doubling the account in one year (12 months) is a really good result and almost the top of one can expect. I am mentioning this because i have seen so many questions from beginners and so many exaggerated expectations like 6 or 8 times the account in a year. I dont know where or from whom they get these expectations.

some can argue that even doubling the account in a year is not enough to feel something in the pocket, one needs to start with 10.000 for that and there is also the thought that some of the profit should stay put to increase the account but nevertheless this is impressive

many thanks and i am sure more appreciation will follow

Timisoara, Romania

3900X 3.8 Ghz 12 cores, 64GB RAM DDR4 3000Mhz, Samsung 970 EVO Plus M.2 NVMe

0

tomas262

4 years ago #275560

Thanks for your post coensio. It’s great to see your hard work pays off.

Just to add to the point 5) great point about futures

.. one can also check stocks since there is an endless amount of opportunities in these markets. While the list of companies can be selected manually (yes, it will be biased) the SQ strategy can do the “dirty work” in terms of trades execution. An algo-trader does not really need to scan&trade all 3000 stocks from the Russell 3000 index as a basket to play the stock market. Just pick any (or your favorite) top 5 US / UK / EU / JP / CH / … companies that have a long term grow potential and grew well historically and develop a decent (not perfect) systems for them. Good examples could be CocaCola, Caterpillar, Facebook, Google and many others similar. Do the same for different exchanges / continents / currencies. Even if any of those company goes belly up (low prob) you can always find another one into your list. I would also like to see such systems having profit factor at least 1 on at least 70% of stocks used in my portfolio.

Have a risk management for each stock in play. Once the system hits the maximum historical drawdown with a specific stock you can for example reduce the lot size to 50 % …

It really does not have to be rocket science or an ultra-hardcore data-mining quest to have a decent portfolio …

I also mention mention stocks because they have no or very little leverage which can prevent from erasing many of beginner’s trading accounts

0

Marcus Smith

4 years ago #276178

I don’t know why, but I decided to read the conversation from the beginning. I really understand that it is important to find a good broker who can analyze everything and make the right forecast. These are just my general thoughts.

0