In this interview, we catch up with Naoufel, a seasoned trader, to explore his journey through the stormy market of 2023. Naoufel is successful trader with verfied track record who use StrategyQuant X for creating his strategies. Additionaly he recently took part in the US Investing Championship with the great results.

Q#1: Hello Naoufel, I am glad to meet you again. It has been one year since we last met and discussed your approach to producing more than 200k in verified profit in your portfolio. Since that moment, a lot has happened, and the markets have remained turbulent. How has your trading been going over the last year?

2023 has certainly been an interesting year.

Most people might focus on the fact that the S&P 500 is up 19% from the start of 2023 through to Dec 1, but it’s worth looking at the chart to see that it was quite a volatile year.

We saw:

- A move up of 11% from the last week of 2022 through to the start of February

- SPX then gave up those gains by pulling back by 9% from the start of February through to mid March

- We then saw a huge move up of 21% from mid March until the end of July

- We then saw a bearish 5 wave zig-zag move down of -6%, +5%, -7%, +4% and -7%; overall, this was a choppy bearish pullback of nearly 11% which ended by late October

- November has been extremely bullish, seeing a 12% increase in just one month

Given that some of my algorithms incorporate market regime analysis, it took approximately two months for them to adjust and start showing substantial activity. Notably, some algorithms that were effective in 2022 became out of sync with the current market dynamics. My practice is to allow algorithms a three-month period to assess if they are still aligned with the market. During this period, I had to pause some strategies and replace them with ones that demonstrated better synchronicity with current market conditions.

I meticulously track multiple strategies that I initially set aside and put them into incubation. By maintaining a pool of rigorously backtested and forward-tested strategies, I can more efficiently substitute poorly performing algorithms with more effective ones.

The role of an algorithmic trader is not only to create robust systems but also to strategically choose and manage these systems, akin to a coach managing a sports team. This involves identifying which ‘players’ (algorithmic strategies) need to be benched and which ones are emerging as ‘rising stars’ and should be put into play.

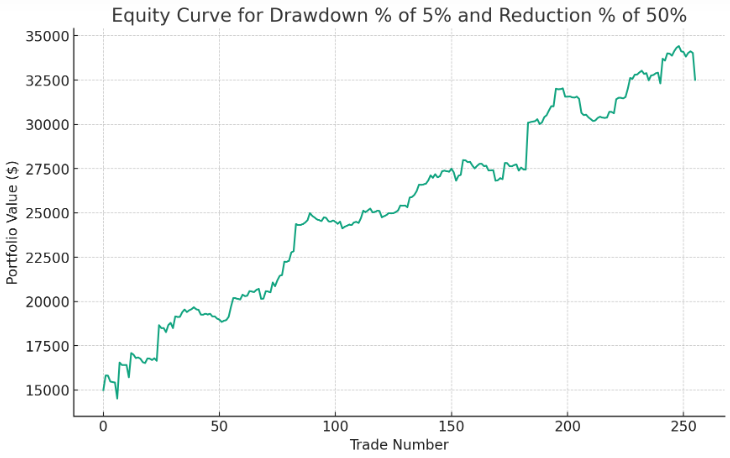

Additionally, an experimental development in my trading approach this year has been an evolution of my implementation of dynamic sizing, guided by the concept of ‘progressive and regressive’ exposure. This approach entails increasing investment exposure during periods of good performance and decreasing it when performance wanes. I’ve backtested various scenarios using this risk management technique. Specifically, I simulated different drawdown thresholds ranging from 5% to 20% in 5% increments, and varied the reduction in exposure from 50% to 75% in 25% increments. The most effective strategy emerged as reducing investment by 50% after a 5% portfolio decline, offering the most favorable risk-adjusted returns. This finding underscores the importance of adaptable risk management in algorithmic trading.

Here’s a simulation of the equity curve of reducing investment by 50% after a 5% portfolio decline:

In this strategy:

- When the equity curve drops by the specified drawdown threshold (5% in the best-performing scenario), the position size is reduced by the set reduction percentage (50% in this case).

- If the equity curve then recovers and achieves a new all-time high, the position size is reset to full size (100%), regardless of previous drawdowns or reductions.

This approach allows for the dynamic adjustment of risk exposure based on the recent performance of the trading strategy, aiming to protect capital during downturns and capitalize on favorable market conditions when trends reverse. More testing is needed to confirm the benefit of this approach.

In essence, the dual focus on strategic algorithm selection and dynamic risk management has been pivotal in navigating the shifting market landscape of 2023.

Therefore some of the main factors leading to a successful 2023 trading year have been:

- Selection of multiple robust strategies, following our methodology as described in the Mining for Gold course (https://university.tradingdominion.com/p/mining-for-gold)

- Strategic algorithm selection, where we can swap out non performing strategies with other strategies which have been incubated

- Dynamic risk management

- Trading dozens of strategies within an overall portfolio for the diversification benefits

- Focus on being able to make profits during bullish periods, but then being able to keep drawdowns contained during pullbacks

Q#2: During 2023, you participated in the US Investing Championship. Could you tell us more about that? And congratulations on the great results.

Thank you for the congratulations. Participating in the 2023 US Investing Championship was an interesting experience. It’s a competition that brings together some of the most skilled traders and money managers from across the globe.

My approach to the competition centered around the MFG methodology (https://university.tradingdominion.com/p/mining-for-gold). With the help of our custom workflow, I leveraged platforms like StrategyQuant to develop and optimize robust trading strategies.

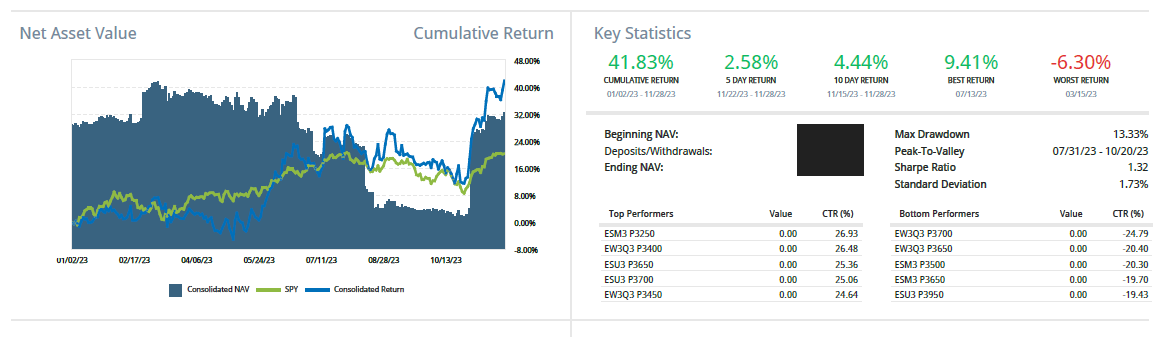

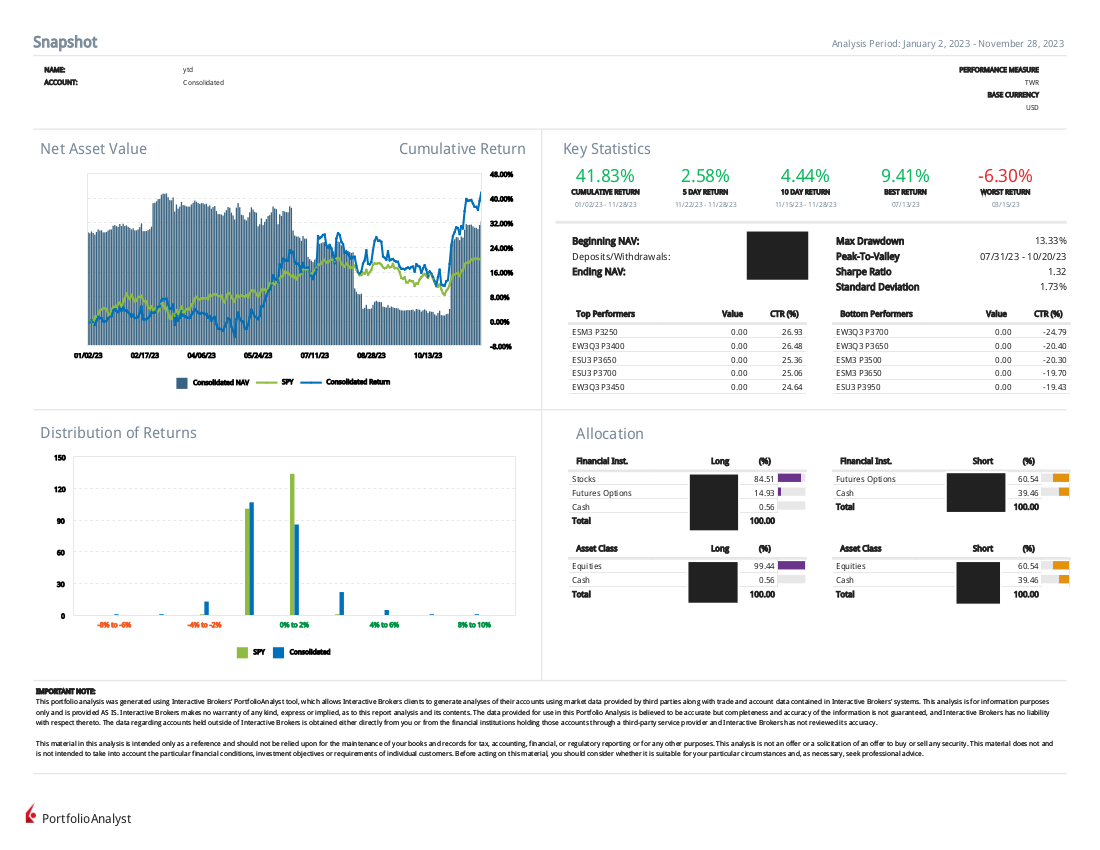

MFG strategies primarily focused on breakouts. While the US Investing Championship doesn’t provide risk-adjusted metrics like the Sharpe ratio or maximum drawdown ratio, my focus was still on producing significant returns while maintaining a good Sharpe ratio and shallow drawdown metrics. You’ll see some competitors with extraordinary returns, but what was their drawdown? Additionally, some competitors might just gamble the required minimum of 20k for entry in hopes of achieving high percentage returns. However, what’s more important is that the returns are audited and verified by a third party. Having skin in the game is crucial; you want to learn from someone who trades with their own money and whose results are verified by a third party, like Kinfo, or in this case, by the US Investing Championship

The results so far for US investing championship is +42% YTD with a drawdown of 13% and a Sharpe of 1.32. The results could also be corroborated by Kinfo (https://kinfo.com/portfolio/12154/performance), which is a third-party firm that verifies your trades.

Q#3: You have had an active track record at Kinfo since May 2019. What is your secret recipe for staying in the trading business, remaining successful, and being able to sustainably grow your trading account?

Since establishing my track record on Kinfo in May 2019, my approach to maintaining success in algorithmic trading has been deeply influenced by the principles outlined in Andrew S. Grove’s “Only the Paranoid Survive”. Central to this approach is a blend of anticipation, adaptability, and leveraging advanced tools such as StrategyQuant for strategy development, workflow automation, and robustness testing.

1. Anticipation and Adaptability: I continually monitor market trends, new hot symbols and sectors to anticipate significant shifts. This vigilance allows me to adapt my trading strategies in alignment with evolving market conditions, a process greatly enhanced by the analytical capabilities of SQX

2. Continuous Strategy Evolution: The dynamic nature of the markets demands constant evolution of trading strategies. Here, our specialized StrategyQuant workflow, a cornerstone of the “Mining for Gold” course, enables me to create, test, and refine a diverse range of strategies across different markets efficiently. The MFG workflow increases the chance that strategies that made it to the end are robust and ready to be incubated.

3. Robust Risk Management: In line with Grove’s concept of constructive paranoia, I apply meticulous risk management to my trading activities. I simulate various market scenarios and assess the risk profiles of my strategies, allowing for timely adjustments and enhanced risk control.

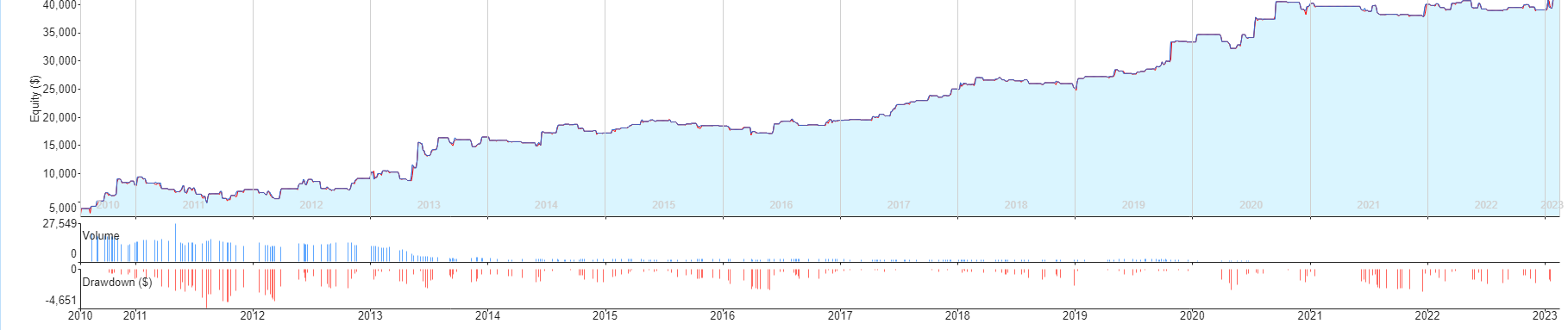

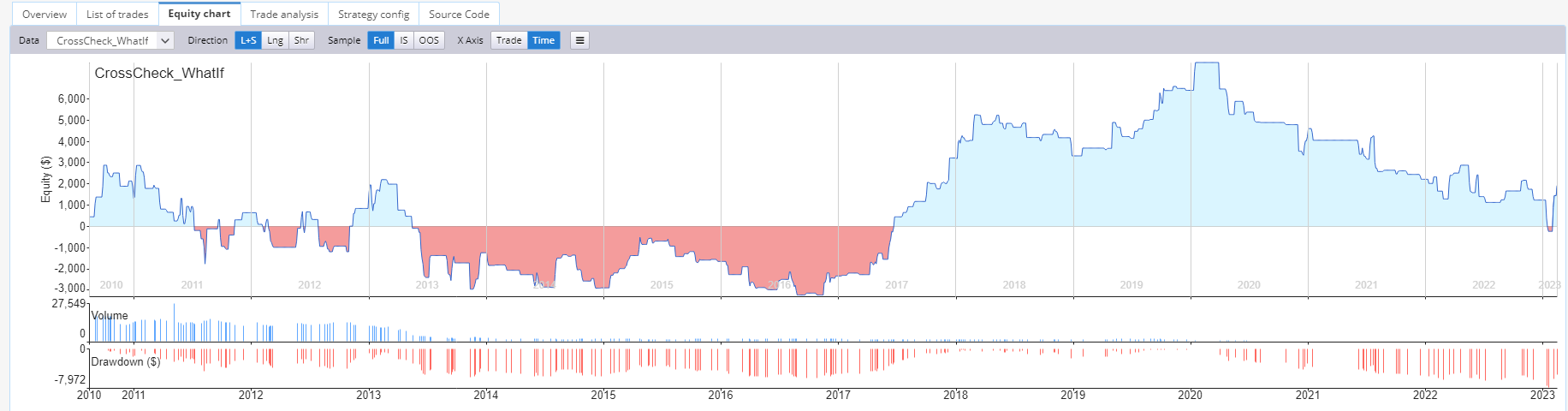

As an experimental approach, I’ve also started leveraging the “what if” functionality within StrategyQuant. I want to see how my strategy will perform if it misses 5% of profitable trades, including the 2 biggest winners. I want to see if my strategies will still have decent performance after removing all these trades.

Here’s an example: This is a strategy before using the “what if” feature:

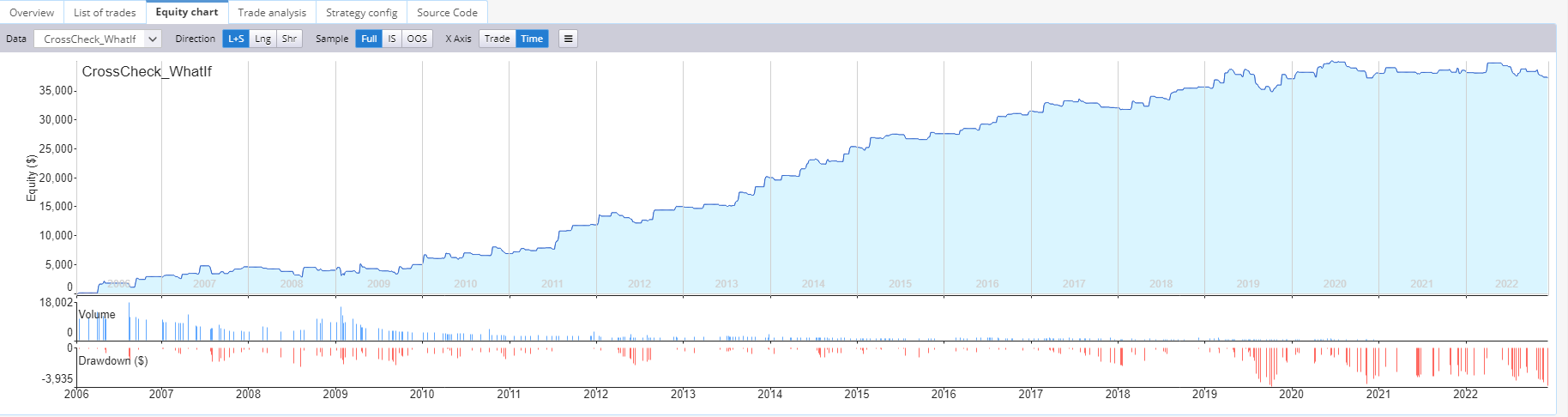

Here’s the same strategy with the “what if” feature activated. We removed 5% of the profitable trades including the two biggest winning trades:

You can see that the strategy is not that attractive after this removal.

Here is another strategy from the databank that still looks interesting, even after removing 5% of the profitable trades and the two biggest winners. More research is needed to confirm if this new robustness test provides value in the forward test.

In summary, my ‘secret recipe’ for sustained success in algorithmic trading consists of:

- Following the methodology explained in the Mining for Gold course in order to create robust strategies

- using the powerful capabilities of StrategyQuant for data mining, strategy creation, workflow automation and robustness testing

- leverage Grove’s principles of vigilance and adaptability

This combination allows for the continuous development of innovative, data-driven strategies, robust risk management, and the agility to adapt swiftly to the ever-changing market landscape.

Thank you, Naoufel, for sharing your trading insights. I am sure that this interview will inspire many traders. Additionally, I have an extra point for you, the reader of this article. If you are interested in Naoufel’s views on any other trading topics, please let us know at [email protected]. Naoufel is open to a follow-up and share his knowledge with the trading community.

Tomas Vanek

Tomas Vanek