Documentation

Applications

Last updated on 27. 1. 2020 by Mark Fric

Portfolio Master – new features in 4.7

Page contents

There were three new features added into QuantAnalyzer 4.7

Possibility to choose Data range

as name suggests you are able to limit the dates on which the portfolio is computed. This is useful if you have multile strategies that don’t start or stop trading at the same time.

![]()

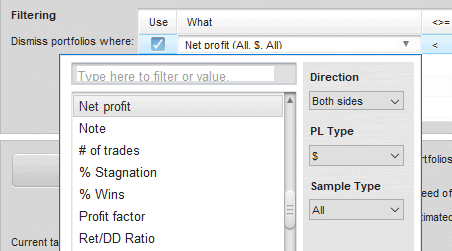

Automatic filtering by conditions

Now you are able to automatically filter out portfolios that don’t fulfill the given conditions:

Note that you can choose direction and PL type for the metric as well as Sample type – another new feature:

Out of sample part

when using Genetic search in Portfolio master you are able to reserve some part of he data as an Out of sample part.

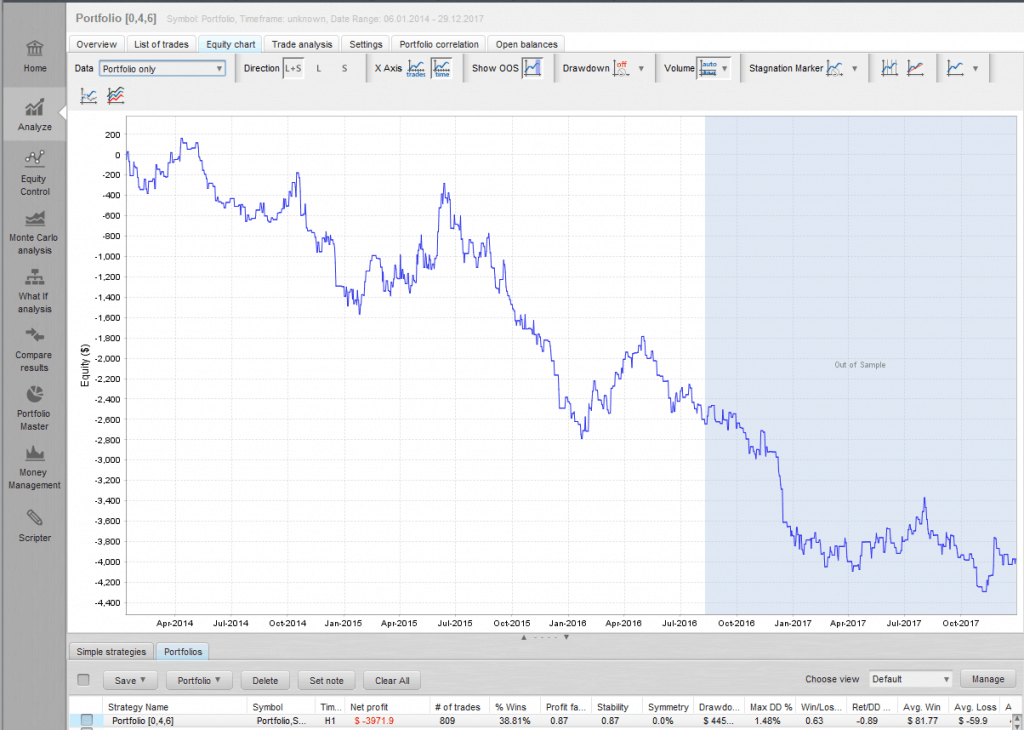

This means that this part will be not used in genetic evolution, the engine will not “see” this part when it evolves the population of portfolios in genetic evolution.

Using Out of sample part is a protection or check against curve fitting, because you can then see if portfolio works the same also on this unseen part of the data.

To visually display Out of sample part you have to switch to Portfolio only data in equity chart, and it is displayed like this:

You can use Out of sample part also in the Filtering conditions.

Was this article helpful? The article was useful The article was not useful