Documentation

Applications

Last updated on 22. 5. 2020 by Mark Fric

Results – Strategy correlation

tab Portfolio correlation is visible only if the strategy backtest contains multiple results:

- you used Merge function (in databank) to merge multipe strategies to a portfolio

- you use Backtest on additional markets cross check to test the strategy on more markets

The correlation matrix has to be computed, you can choose correlation by hour, day, week or month and correlation of Profit/Loss or trade counts.

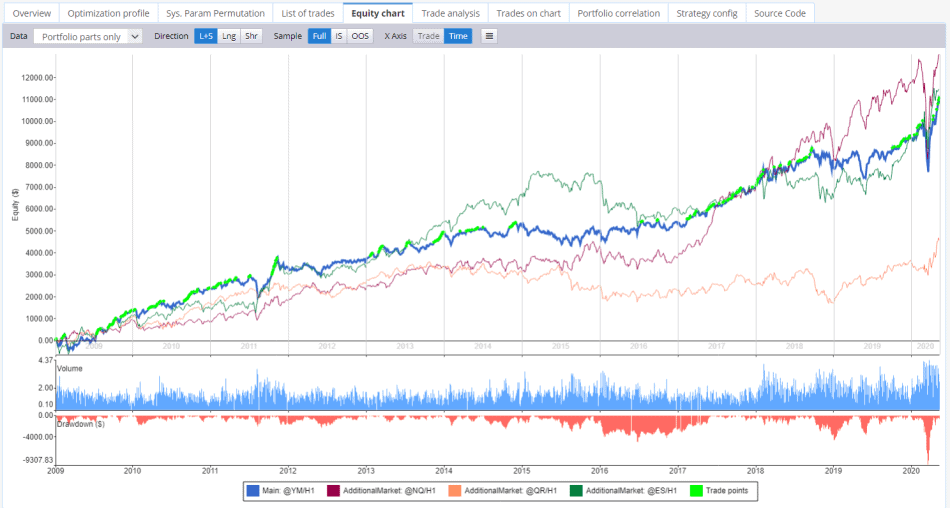

When you have multiple strategy backtest merged in one strategy, you can also see equity curves for all of them in Equity chart:

Was this article helpful? The article was useful The article was not useful

Please login to comment

0 Comments

Oldest