Documentation

Applications

Last updated on 4. 8. 2020 by Mark Fric

What If simulations

Page contents

What If simulations is a new powerful yet quick and simple cross check to verify strategy robustness (added into StrategyQuant Build 129).

What If scenarios allow you to simulate scenarios like:

- what if strategy trades only certain days in a week, or certain hours in a day?

- what if we’ll ommit 5% of the most profitable trades?

- etc.

The idea for What If cross check came from our QuantAnalyzer product, which has this functionality for a long time.

By adding it to StrategyQuant as a cross check you can immediately filter out strategies that will perform significantly worse under your What If scenario.

How does What If simulation work?

It is simple – every selected What If simulation is applied to the list of orders produced by the standard backtest.

For example, if you use Trade only in days simulation and choose to trade only on Tuesday, Wednesday, Thursday, it will go through all the trades an dfilter out the ones that were not opened in these three days.

It is important to realize that What If simulation doesn’t backtest the strategy again – it works with existing list of trades from main backtest. Thanks to this, this crosscheck is very fast.

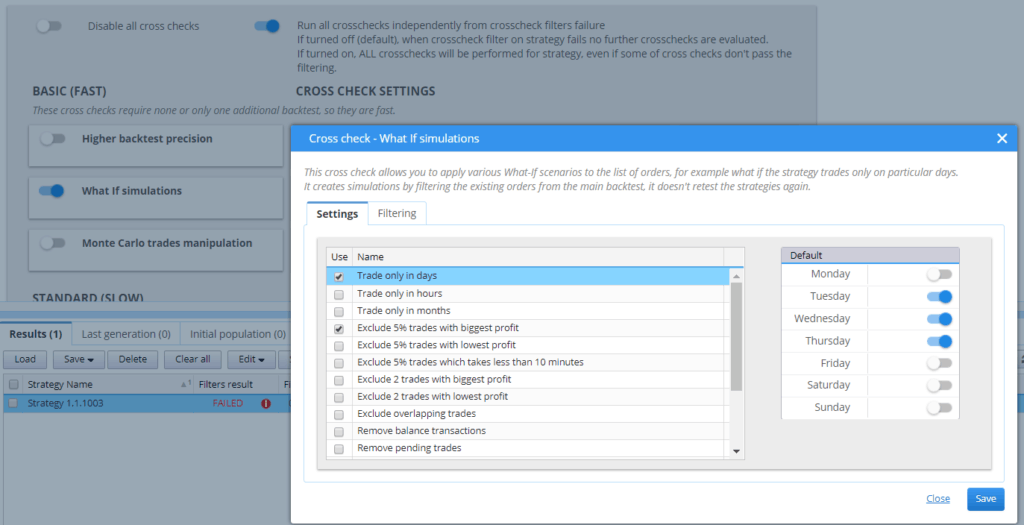

Configuration

What If is similar to Monte Carlo – you choose one or more scenarios that are applied to strategy results:

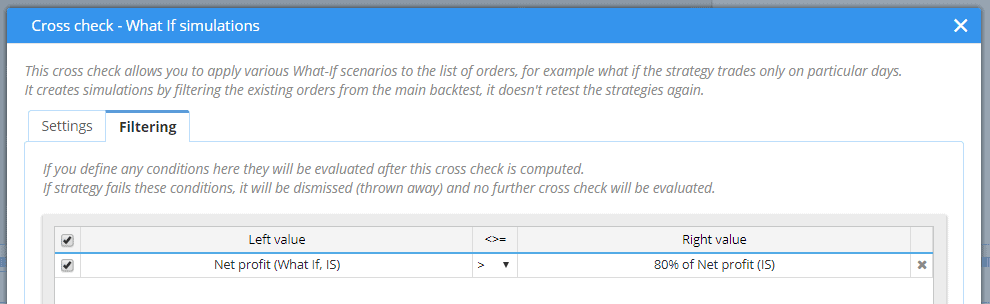

Filtering based on What If simulation performance

optionally you can use automatic filtering to filter out strategies whose performance falls under given limit:

In the picture above we defined that Net profit of What if simulation must be at least 80% of Net profit of normal backtest.

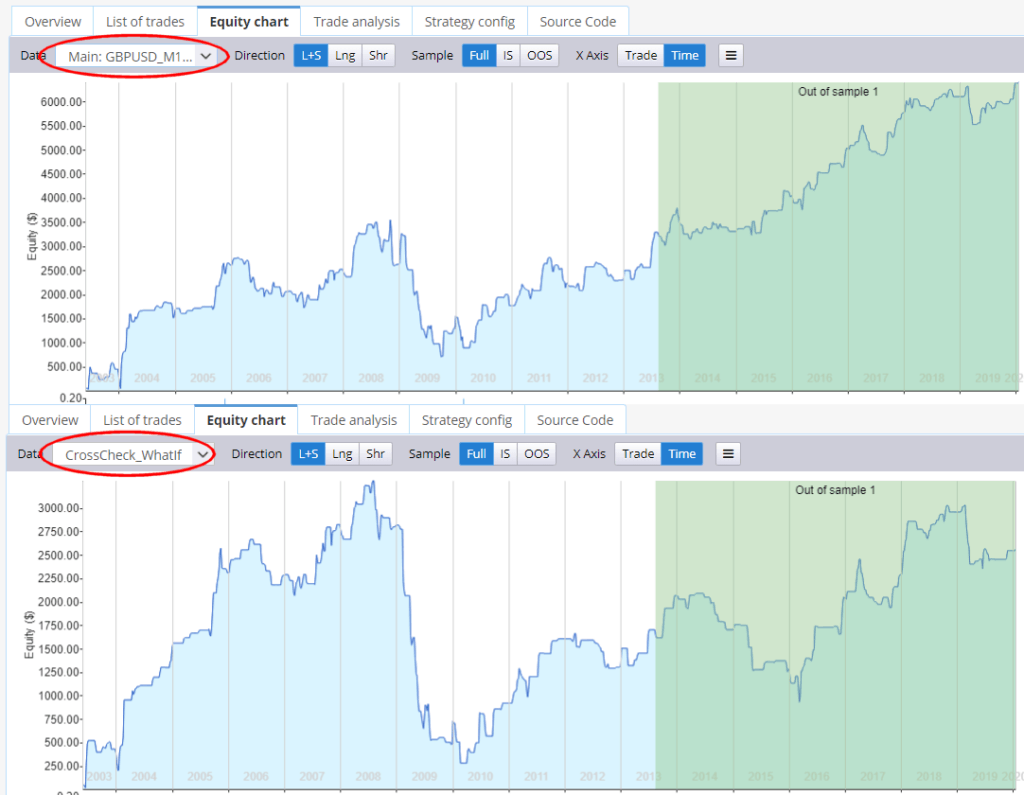

Viewing results

when you run What If simulation it will create a new result that can be displayed in equity chart, overview or in list of trades.

See an example of difference between backtest equity and What If simulation below:

Was this article helpful? The article was useful The article was not useful

can it automatically select best days?

and exclude worst days?

What do you mean by that? Or what is the point of this? You never know in advance what daily PnL will be so there is not point in filtering “bad days” in the backtest

Thank you

All is ok. And how i can apply What if conditions to a strategy?

You would need to edit the MQL code manually to incorporate what-if rules OR edit the strategy in AlgoWizard and setup conditions coresponding to what if rules

You are right. I always forget that in AlgoWizard, I can modify many parameters. Thank you.

And now comes the next question:

In AlgoWizard, can I add conditions so that it does not operate the strategy between 8 and 9 a.m., on a Thursday (for example). how would it look like? What I show is something I have tried but I can’t find the solution.

LongEntrySignal=

RSI (14)[1] > 57.8

and

Current Day Of Week <> 4

and

Current Time >= GetTime(8,0,0)

and

CurrentTime <= GetTime(9,0,0)

(i know it don’t work, how can i do it work?)